Bowling Alley

BUSINESS PLAN THE FAMILY BOWL

P.O. Box 12345

Omaha, Nebraska 68101

The Family Bowl business plan outlines a strategy for a bowling alley that caters to families and celebrates people of all nationalities. It will differentiate itself from other bowling alleys by providing a clean and friendly atmosphere. It also will have the largest number of lanes in the area. This plan was provided by Ameriwest Business Consultants, Inc.

- EXECUTIVE SUMMARY

- OBJECTIVES & GOALS

- BUSINESS DESCRIPTION, STATUS, AND OUTLOOK

- MANAGEMENT AND OWNERSHIP

- MARKET ANALYSIS

- MARKETING STRATEGIES

- FINANCIAL PLANS

Confidentiality Statement

The information, data, and charts embodied in this business plan are strictly confidential and are supplied on the understanding that they will be held confidentially and not disclosed to third parties without the prior written consent of Robert Smyth.

EXECUTIVE SUMMARY

BUSINESS DESCRIPTION

The purpose of the Family Bowl is to provide the area with a bowling alley which caters primarily to families. The atmosphere will be friendly and open. The alley will be maintained to the utmost degree of cleanliness and maintenance, unlike similar operations in the area. The alley's employees will display a new attitude. They will treat customers like first-class citizens and try to make them feel like they are at home. On the premises will be pool tables, video games, and dart boards. We will offer for sale pride items, in a gift shop, from various cultures around the world. The facility will have a first rate sound and lighting system. The services will be offered at a competitive price and pricing will be reviewed periodically. We plan to become the premier bowling alley in the area within two years. We will offer the best entertainment, atmosphere, cultural awareness, and service in metro Omaha, Nebraska.

The facility will normally be closed on Monday. Proposed hours are Tuesday, Wednesday, and Thursday, 2:00 P.M. through 2:00 A.M. On Friday and Saturday the hours will be 12:00 P.M. through 2:00 A.M. On Sunday the hours will be 4:00 P.M. through 2:00 A.M. The premises will be open for a total of 74 hours per week.

CURRENT POSITION AND FUTURE OUTLOOK

The business is in a start-up mode. Plans call for starting operation by the spring of 2000. During the first full year of operation we plan to serve an average of 10,000 customers per month. The second year this will increase to 15,000 per month. Years three through five will show gradual increases to 18,000 per month which we consider to be our capacity. To attain these goals we will use a combination of media advertising, flyers, direct mail, and word-of mouth. Franchising the concept is a possibility for the future.

MANAGEMENT AND OWNERSHIP

The company will be set up as a corporation with Robert Smyth and his wife, Julie, as the major shareholders, incorporators, and directors. Robert Smyth will serve as president and manager. He will also provide the leadership to run this company. He has over 17 years experience as owner and operator of various small business operations, and has dealt with the public as a personnel officer in the military. Initially, up to thirteen other employees will be needed. These employees will be involved in bartending, security, and waiting on tables. They will be a combination of part-time and full-time. When volume picks up, additional part-time or full-time employees will be hired as the workload requires. Small Business Nebraska, Inc. will provide help in additional areas such as setting up the books, logo design, and general business advising when necessary and to supplement the Smyths' overall business knowledge. The services of an accountant, attorney, and a qualified insurance agent have been retained.

UNIQUENESS AND DIFFERENTIATION OF THE SERVICE

The Family Bowl will be the largest bowling alley which caters to families. It will have the largest number of lanes in the area.

The idea of this company is to provide customers with a semi-formal, social setting, and entertainment that does not exist in this part of the state. We will provide customers with high-tech lights and sound, video games, pool tables, and a full line of entertainment. In addition we will cater to private parties and special groups such as schools, senior citizens, and church groups.

The growth potential is virtually unlimited for the greater Omaha area. The population is growing at an accelerated rate. Currently over 12% of the population in Omaha is young. They will be very receptive to a concept such as this that can offer them atmosphere, cleanliness, and security at a competitive price.

It is rare in today's business world to find a true market void. That is exactly what Family Bowl has done. It is combining the latest in technology with an unfilled need and promises to deliver a high quality new product at a competitive price. Our proposed facility will have little true competition in metro Omaha.

FUNDS REQUIRED AND USAGE

The initial start-up expenses will be approximately $300,000. The inventory, equipment, furniture, fixtures, and leasehold improvements will cost approximately $125,000. Investors and/or a bank loan must be secured in the amount of $125,000 at 14.0% amortized over ten years. The initial investors will furnish approximately $50,000, which is 18.5% of the total. After all expenses of start-up, $40,000 will remain in a new business checking account and will provide the balance of the initial working capital.

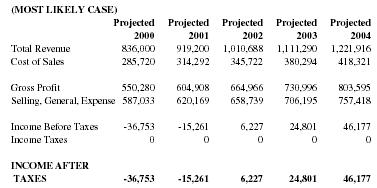

Projected 5-Year Income Statement

| (MOST LIKELY CASE) | |||||

|

Projected

2000 |

Projected

2001 |

Projected

2002 |

Projected

2003 |

Projected

2004 |

|

| Total Revenue | 836,000 | 919,200 | 1,010,688 | 1,111,290 | 1,221,916 |

| Cost of Sales | 285,720 | 314,292 | 345,722 | 380,294 | 418,321 |

| Gross Profit | 550,280 | 604,908 | 664,966 | 730,996 | 803,595 |

| Selling, General, Expense | 587,033 | 620,169 | 658,739 | 706,195 | 757,418 |

| Income Before Taxes | -36,753 | -15,261 | 6,227 | 24,801 | 46,177 |

| Income Taxes | 0 | 0 | 0 | 0 | 0 |

|

INCOME AFTER

TAXES |

-36,753 | -15,261 | 6,227 | 24,801 | 46,177 |

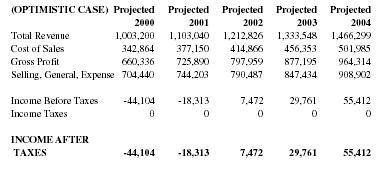

| (OPTIMISTIC CASE) |

Projected

2000 |

Projected

2001 |

Projected

2002 |

Projected

2003 |

Projected

2004 |

| Total Revenue | 1,003,200 | 1,103,040 | 1,212,826 | 1,333,548 | 1,466,299 |

| Cost of Sales | 342,864 | 377,150 | 414,866 | 456,353 | 501,985 |

| Gross Profit | 660,336 | 725,890 | 797,959 | 877,195 | 964,314 |

| Selling, General, Expense | 704,440 | 744,203 | 790,487 | 847,434 | 908,902 |

| Income Before Taxes | -44,104 | -18,313 | 7,472 | 29,761 | 55,412 |

| Income Taxes | 0 | 0 | 0 | 0 | 0 |

|

INCOME AFTER

TAXES |

-44,104 | -18,313 | 7,472 | 29,761 | 55,412 |

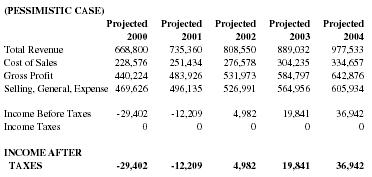

| (PESSIMISTIC CASE) | |||||

|

Projected

2000 |

Projected

2001 |

Projected

2002 |

Projected

2003 |

Projected

2004 |

|

| Total Revenue | 668,800 | 735,360 | 808,550 | 889,032 | 977,533 |

| Cost of Sales | 228,576 | 251,434 | 276,578 | 304,235 | 334,657 |

| Gross Profit | 440,224 | 483,926 | 531,973 | 584,797 | 642,876 |

| Selling, General, Expense | 469,626 | 496,135 | 526,991 | 564,956 | 605,934 |

| Income Before Taxes | -29,402 | -12,209 | 4,982 | 19,841 | 36,942 |

| Income Taxes | 0 | 0 | 0 | 0 | 0 |

|

INCOME AFTER

TAXES |

-29,402 | -12,209 | 4,982 | 19,841 | 36,942 |

Notes:

- The most likely case assumes 10,000 customers per month the first year with each spending an average of $25.00 per visit. The second year the number of customers will rise to 15,000 per month also assumes each will spend $30.00 per visit.

- The optimistic case assumes revenues and expenses will increase 15% over the most likely case. The pessimistic case assumes revenues and expenses will decrease 15% below the most likely case above.

OBJECTIVES & GOALS

- To provide a high quality service so that customers will perceive great value and give them the opportunity to interact with other families in a safe and clean environment.

- Service an average of 10,000 customers per month during the first full year of business and 15,000 customers per month the second year. The ultimate goal is to reach 18,000 customers per month by the third year

- To repay the entire loan amount by the end of the third year and to provide the shareholders with a stable and sufficient income after that.

- Our goal is to become the premier bowling alley in metro Omaha during the next two years.

- Family Bowl plans to closely monitor changing technology to be certain that the company is using the latest and most cost effective equipment and that it keeps up with current trends in the marketplace.

- When economically feasible we plan to open one or more locations and/or consider franchising our service.

When growth has stabilized we plan to add extra services for customer convenience such as large screen television, enhanced game rooms, and food services. In addition to the above goals we will survey our customers and make changes in our programs and add services to meet their changing ideas in the marketplace.

Strategies for Achieving Goals

To obtain the first two sets of goals we will try to maximize sales with an extensive campaign to promote our service. We will utilize the radio stations and newspaper along with brochures, media advertising, pamphlets, direct customer contact, use of coupons, referrals, and a variety of other advertising and marketing tools to reach the customer base of metro Omaha. We expect to flood the market with advertising until consumers become aware of us and more comfortable with our company. As we grow, word-of-mouth referrals will bring in increasing numbers of customers and we will reduce our reliance on advertising.

The dominant driving force behind our company will be profit and income.

To become the premier bowling alley in metro Omaha, we will offer outstanding quality, cleanliness, security, long hours, and reasonable pricing. We will listen to our customers and conduct surveys.

As we grow and build a reputation for our people and culturally oriented atmosphere with excellent security, service, and entertainment, we will offer frequent user discounts. In the future we may consider diversification and enter new market areas.

BUSINESS DESCRIPTION, STATUS, AND OUTLOOK

The Family Bowl will be a full service bowling alley combining entertainment suited to a specific culture at a competitive price. We will try to promote an atmosphere that will remind many people of their homeland. This is a relatively new concept for this part of the country. Robert Smyth will operate the business as a corporation. The principal shareholders will be he and his wife, Julie. Initially, Robert Smyth will manage the operation with daily input from Julie and the other investors. The new equipment and enhanced lighting and sound systems will also give us market advantages. A building will be leased that best meets the goals and market we are trying to reach. Ultimately, we will construct our own building to expand to the full potential of this business.

The biggest problem this venture will face will be creating customer awareness of our services. We will use a combination of advertising techniques to increase this awareness. Once a general awareness is present, the industry has a virtually unlimited growth potential.

The future holds the promise for almost unlimited growth and income as the business matures and considers other markets and products. Complementary products such as additional video games, more pool tables, dance lessons, and higher profile entertainment will all be considered in the future in response to customer surveys indicating their wants and needs. Complete food services will be offered in the future as the needs are demonstrated.

MANAGEMENT AND OWNERSHIP

Robert Smyth has owned several successful small businesses in Texas and Nebraska. He attended Texas State University from 1979 through 1983. His major was civil engineering and his minor was business. He also has experience as a bartender, bouncer, and cashier in pool halls and arcades. He had 14 years experience in personnel management in the military. These skills will help ensure that the Family Bowl will have a solid foundation of management skills available to it.

The Smyths' will supplement their skills by using outside consultants in areas such as legal work, income tax preparation, insurance, and general business advising.

The business will be set up as a corporation. This form of legal entity was chosen primarily for liability reasons and to make it easier to secure investors. To begin operation, as many as thirteen full-and part-time employees will be hired to help in areas such as bartending, waiting on tables, and security. As the business grows additional part-time or full-time employees may be added to handle the increased workload.

The Service — An Unfilled Need

Nebraska growth in families is the ninth greatest in the country. The past decade has seen this segment of the population grow by more than 30%. It is growing 5 1/2 times as fast as the general population.

The few existing bowling alleys that cater to families are dark and dingy. They pay little attention to cleanliness, maintenance of premises, and security for their patrons. Family Bowl and its ownership will embrace the family community and try to become a focal point for them. We will promote families whenever possible.

The idea for a family-oriented bowling alley was formulated when Robert and Julie Smyth noticed a need for a quality bowling alley which caters to families in southern Omaha. They have conducted extensive surveys of the local families. These surveys have shown a great interest in such an alley. These surveys also have indicated that cleanliness, good maintenance, good security, quality live entertainment, and a semi-formal atmosphere are all desirable characteristics for which people are looking.

The timing for such a business is perfect. A significant window of opportunity exists for a company such as the kind we are proposing. This proposed business will be providing the "Right Service at the Right Time."

Uniqueness of the Service

It is rare in today's world that a true market void exists. Our service will meet the "unfilled need" described above by providing customers with competitively priced bowling alley facilities combined with the latest in lighting and sound systems and longer hours. We will be considerably larger than the typical bowling alley.

Customers will be attracted to the Family Bowl because our atmosphere, pricing, and facilities. They will be made to feel welcome and as part of the family.

Some major advantages Family Bowl will have over potential competition and conventional bowling alleys are:

- Larger and newer facility

- Lower operating expenses

- Best sound and lighting system in the area

- New concept—cater primarily to families

- Live diversified entertainment

- Location

- Longer hours

- English lessons for those interested

- Dance lessons for patrons wanting to keep up with the latest dance steps

- The cleanest restrooms in the city

- Security personnel and other employees who can speak both Spanish and English

- The largest dance floor in the area

- Display cabinets with pride items for purchase such as flags, hats, scarves, etc.

- Family Bowl will sponsor ethnic festivals and holidays

MARKET ANALYSIS

MARKET OVERVIEW, SIZE, AND SEGMENTS

Currently, the market distribution is shared by three major participants. They are all located on the north side of Omaha. This market segment has been relatively stable over the past five years.

The market area we will concentrate on is Greater Omaha County. This includes 6 surrounding towns. Additionally, we expect to draw some patrons from a northern town which is only 40 minutes away. These areas have been growing rapidly the past several years and should continue for the foreseeable future. Once the concept catches on locally, we feel the potential is unlimited. As we grow we will have the financial capacity to carry on an advertising campaign on a regional basis.

The economy is in the midst of a particularly strong growth period. Many new jobs are being added to the local community. Ever increasing numbers of Californians are moving to this location. All of these factors are cause for a much greater interest in bowling alleys. All of this activity can only help our attempts to start a bowling alley.

Listed below are just some of the reasons that the Omaha area is growing and why it is a good time to be starting any kind of new business:

- The local economy is booming and virtually busting at the seams.

- Omaha has become a magnet for religious organizations. More than 65 nationally based Christian organizations are headquartered here. The largest has over 1,200 employees (especially women) and an operating budget of over $85 million.

- The new Apple Computer plant is setting records for production and is adding new employees monthly.

- Omaha has a new airport and a nearby Free Trade Enterprise Zone that should grow and attract even more new businesses.

- Gambling in nearby Red Hawk continues to draw many visitors and some new businesses.

- Every week, we see articles in the newspapers of California residents and companies relocating here.

- The world renowned Four Seasons Hotel is building a new convention facility here.

- MCI and Quantum Electronics are undergoing large increases in their operations here that should add many hundreds of employees.

- Prairie Springs is only 50 minutes away and is another good market for businesses in the area.

- Many experts predict metro Omaha to become the fastest growing city in the state between now and the year 2005.

- The local economy is now more diversified than it was when troubles occurred in the local economy in the late 1980s and early 1990s.

The estimated population of Omaha County in 1998 was 900,000 people. The number of households was 480,000. Currently, this market is growing at an annual rate of 3-5%. Projections see this trend continuing for the balance of this next decade.

From the above figures it can readily be seen that the potential market for our services is huge. We feel with our pricing and value we will become a price and industry leader within two years.

Customer Profile

Our surveys have shown the following mix of patrons that use Spanish-oriented alleys:

- 5% White

- 3% Black

- Median age of local Hispanics is 25.9 years, whereas the median age of the rest of Nebraskans is 32.5 years.

- Majority of patrons will be in the middle to upper income brackets.

- There are over 45,000 Hispanics in Omaha, nearly 40,000 in Lincoln and over 20,000 in surrounding areas. They have increased more than 5 1/2 times as fast as the general population.

Typically, our customers will be middle to upper income. Beyond the local market we could eventually tap into a more regional market. The advantage of our service is that it could appeal to all segments of the community.

Throughout this business plan we have taken a very conservative approach to developing our financial projections.

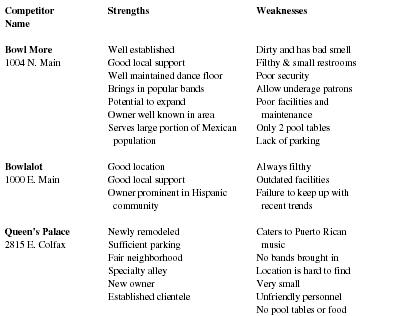

Competition

Our primary competition are the bowling alleys listed below. On a limited basis there are other competitors such as strip alleys, country and western bars, and other bowling alleys.

The following table summarizes the local competition:

| Competitor Name | Strengths | Weaknesses |

|

Bowl More

1004 N. Main |

Well established

Good local support Well maintained dance floor Brings in popular bands Potential to expand Owner well known in area Serves large portion of Mexican population |

Dirty and has bad smell

Filthy & small restrooms Poor security Allow underage patrons Poor facilities and maintenance Only 2 pool tables Lack of parking |

|

Bowlalot

1000 E. Main |

Good location

Good local support Owner prominent in Hispanic community |

Always filthy

Outdated facilities Failure to keep up with recent trends |

|

Queen's Palace

2815 E. Colfax |

Newly remodeled

Sufficient parking Fair neighborhood Specialty alley New owner Established clientele |

Caters to Puerto Rican music

No bands brought in Location is hard to find Very small Unfriendly personnel No pool tables or food |

Our facility will be more convenient than any other facility for over 75% of the population in metro Omaha.

The marketplace is currently shared by the above outlined 3 major participants. This market is increasing about 5-7% per year.

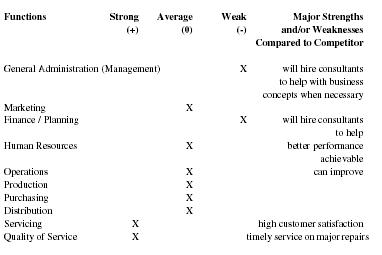

Identification of Strengths and Weaknesses

| Functions | Strong(+) | Average(0) | Weak | Major Strengths and/or Weaknesses Compared to Competitor |

| General Administration (Management) | X | will hire consultants to help with business concepts when necessary | ||

| Marketing | X | |||

| Finance /Planning | X | will hire consultants to help | ||

| Human Resources | X | better performance achievable | ||

| Operations | X | can improve | ||

| Production | X | |||

| Purchasing | X | |||

| Distribution | X | |||

| Servicing | X | high customer satisfaction | ||

| Quality of Service | X | timely service on major repairs |

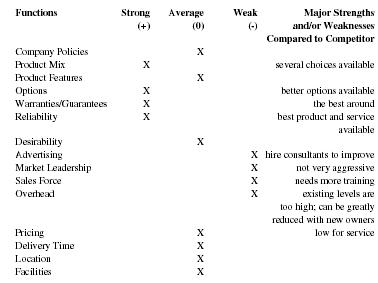

| Functions | Strong(+) | Average(0) | Weak(-) |

Major Strengths and/or Weaknesses

Compared to Competitor |

| Company Policies | X | |||

| Product Mix | X | several choices available | ||

| Product Features | X | |||

| Options | X | better options available | ||

| Warranties/Guarantees | X | the best around | ||

| Reliability | X | best product and service available | ||

| Desirability | X | |||

| Advertising | X | hire consultants to improve | ||

| Market Leadership | X | not very aggressive | ||

| Sales Force | X | needs more training | ||

| Overhead | X | existing levels are too high; can be greatly reduced with new owners | ||

| Pricing | X | low for service | ||

| Delivery Time | X | |||

| Location | X | |||

| Facilities | X |

We feel we will have strengths in product features, management, planning, human resources, quality of service, product mix, options, and reliability because we will have new equipment, pricing, location, and facilities. We will have low risk exposure in the areas of technology, inflation/interest rates, regulatory environment, management ability, location, facilities, and suppliers.

We perceive medium risk exposure in the local economy, strategy, and vulnerability to substitutes, finance and planning, company policies, sales force, and pricing. We have retained the services of specialists to help in various areas such as marketing, setting up the books, providing management reports and general overall business operation advice.

Since we are new to this type of business we will have a high degree of risk in this area. It will take a little time to gain knowledge in developing the business and create a customer awareness of our company and our concept. To help reduce this risk we will hire experienced consultants.

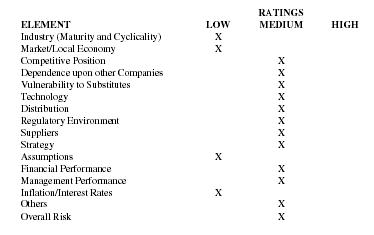

Risk Analysis

| RATINGS | |||

|

ELEMENT

|

LOW | MEDIUM | HIGH |

| Industry (Maturity and Cyclicality) | X | ||

| Market/Local Economy | X | ||

| Competitive Position | X | ||

| Dependence upon other Companies | X | ||

| Vulnerability to Substitutes | X | ||

| Technology | X | ||

| Distribution | X | ||

| Regulatory Environment | X | ||

| Suppliers | X | ||

| Strategy | X | ||

| Assumptions | X | ||

| Financial Performance | X | ||

| Management Performance | X | ||

| Inflation/Interest Rates | X | ||

| Others | X | ||

| Overall Risk | X | ||

MARKETING STRATEGIES

PRICING AND VALUE

We will offer a series of cost savings options to groups that use our facility the most frequently. Our intention is to raise the public's awareness of our company. We plan to review our prices and those of our competitors every three months. We will review direct material costs, direct labor costs, and total overhead expenses. We will continually monitor the cost of providing our service to each customer. We will offer discounts to larger groups. We will offer various free or reduced rate programs to get customers acquainted with us.

At this point there is a certain amount of price restrictions in this service. With the current level of competition we must be careful not to price ourselves out of the market.

Numerous package deals will be available to customers. Various marketing strategies we may try include the following:

- Discounts for larger groups

- Frequent user discounts

- Special party rates

- Spirited cultural competition

SELLING TACTICS

Our company's marketing strategy will incorporate plans to promote our line of services through several different channels and on different levels of use. We will advertise heavily on the popular local Hispanic radio stations and newspapers.

We will try to satisfy the market void in this area for indoor entertainment. We will flood the market with advertising and try to go after our specific targets. We will try to capture their attention, pique their interest, make them feel that they must have our services.

We will offer continuous promotional rates. The results sell themselves. We will offer discounts to frequent users. The more a customer uses our services the cheaper it will become for them.

We will also become a MasterCard and Visa charge card merchant to enable us to more readily charge our customers.

In order to sell our facility we shall consider a variety of promotions including:

- Reserve certain hours for unique groups such as children, senior citizens, adults, etc.

- Conduct special theme nights, use ethnic holidays, family night, charity promotion night, game night, contest night, etc.

- Cultivate local churches, and Hispanic organizations

- Promote birthday parties

- Offer dance lessons at no charge

- Early bird specials

ADVERTISING, PROMOTION, AND DISTRIBUTION OF SERVICES

We recognize that the key to success at this time requires extensive promotion.

Advertising goals include all of the following:

- Position the company as the premier alley in metro Omaha

- Increase public awareness of the Family Bowl and its benefits

- Increase public awareness of our company and establish a professional image

- Maximize efficiency by continually monitoring media effectiveness

- Consider a possible credit coupon in some of the advertisement

- Take out an ad in the yellow pages beginning in 2000

- Develop a brochure or pamphlet to explain our service and company

- Create a distinctive business card and company letterhead

- Consider using a direct mail approach

- Use a mix of media to saturate the marketplace

- Spend a minimum of $25,000 in advertising the first year and $35,000 the second year

Public Relations

We will develop a public relations policy that will help increase awareness of our company and product. To achieve these goals we will consider some or all of the following:

Develop a press release and a company backgrounder as a public relations tool.

Develop a telephone script to handle customer and advertiser contact.

Develop a survey to be completed by customers to help determine the following:

- How did they hear about us?

- What influenced them to use our service?

- How well did our service satisfy their needs?

- How efficient was our service?

- Did they have any problems getting through to us?

- Did they shop competitors before selecting us?

- How did they initially perceive our company and product?

- Where are most of our customers located?

- Do they have suggestions for improving our service or our approach to advertising?

- What additional services would they like us to offer?

- Would they recommend us to others?

Join the Chamber of Commerce to keep abreast of developments in the community and market trends.

FINANCIAL PLANS

ASSUMPTIONS, DEFINITIONS, AND NOTES

Family Bowl has used the following assumptions in preparing this business plan:

Average number of customers will be 10,000 per month the first year, 15,000 per month the second year and leveling off at 18,000 per month by the third year.

Revenue sources are as follows:

- Cover charge income will equal 7.08% of total

- Each patron will have 5 drinks per visit at an average price of $2.50 per drink

- Game and food income will be 2.65% of total

- Drink income will equal 88.2 % of the total

Customer volume will be greater in warm weather months.

Growth in sales will be 29.6% the second year, 25% the third, 15% the fourth, and 10% the fifth year.

We have assumed a high and low case by adding or subtracting 15% to the most likely case.

Inflation Rates to remain stable at 3-5%.

Robust local economy.

Interest Rates to remain flat and basically unchanged.

Wage Rates to remain flat.

Local unemployment rates to remain low at approximately 4-5%.

Assumes average income per customer per visit of $14.18.

Assume a rate of pay of $9.00 per hour for security personnel and $4.50 per hour for bartenders and waitresses.

Payroll taxes and benefits will equal 20% of payroll expenses.

Assumes salaries for officers of 3.5% of sales.

Assumes a loan of $125,000 at 14.00% amortized over ten years and having monthly payments of $1,707.93 per month.

Cost of goods sold will be 40% of drink income.

Maintenance, Repair, and Breakage equals 3% of total income.

Advertising & Marketing (Public Relations) is 3.5 % of income.

Amortization of organization expenses will be over 60 months.

Depreciation will be computed using straight line method over 60 months.

Insurance is at 2% of total income.

Telephone and utility expense will be 1.25% of total income.

Office supplies expenses is set at 1% of total income.

Contingency and miscellaneous expenses are set at 3% of total income.

Income tax for both state and federal is set at 20% for year one and 28% for year two.

Dividend payout is set at 15% of net income.

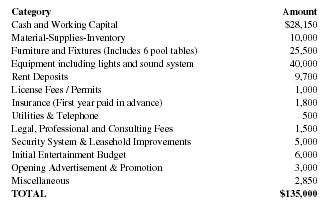

Start-up Expenses

| Category | Amount |

| Cash and Working Capital | $28,150 |

| Material-Supplies-Inventory | 10,000 |

| Furniture and Fixtures (Includes 6 pool tables) | 25,500 |

| Equipment including lights and sound system | 40,000 |

| Rent Deposits | 9,700 |

| License Fees /Permits | 1,000 |

| Insurance (First year paid in advance) | 1,800 |

| Utilities & Telephone | 500 |

| Legal, Professional and Consulting Fees | 1,500 |

| Security System & Leasehold Improvements | 5,000 |

| Initial Entertainment Budget | 6,000 |

| Opening Advertisement & Promotion | 3,000 |

| Miscellaneous | 2,850 |

| TOTAL | $135,000 |

Items to be purchased include 50 tables and 200 chairs, bar equipment, pool tables, sound and lighting systems, initial inventory, leasehold improvements, and various furniture and fixtures. After all expenses $40,000 will remain in a checking account as working capital.

The total investment of $135,000 will be obtained as follows:

| 1. Cash | $25,000 |

| 2. Bank Loan /Investors (Combination) | $110,000 |

Financial Statements Analysis

Many lenders and some investors have adopted the practice of placing constraints and covenants on a borrower in order to ensure that certain levels of liquidity and profitability are maintained. These limits are usually presented to the borrower in the form of loan compliance criteria and are used by lenders/investors for evaluating the loan on an ongoing basis. Some common limits used by lenders/investors are indicated above and demonstrates how this company would do when compared to the industry in each area.

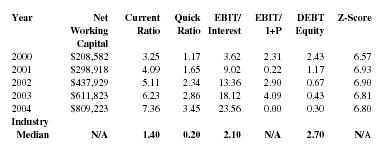

Loan Compliance Covenants

| Year | Net working Captial | Current Ratio | Quick Ratio | EBIT/Interest | EBIT/I+P | DEBT Equity | Z-Score |

| 2000 | $208,582 | 3.25 | 1.17 | 3.62 | 2.31 | 2.43 | 6.57 |

| 2001 | $298,918 | 4.09 | 1.65 | 9.02 | 0.22 | 1.17 | 6.93 |

| 2002 | $437,929 | 5.11 | 2.34 | 13.36 | 2.90 | 0.67 | 6.90 |

| 2003 | $611,823 | 6.23 | 2.86 | 18.12 | 4.09 | 0.43 | 6.81 |

| 2004 | $809,223 | 7.36 | 3.45 | 23.56 | 0.00 | 0.30 | 6.80 |

| Industry Median | N/A | 1.40 | 0.20 | 2.10 | N/A | 2.70 | N/A |

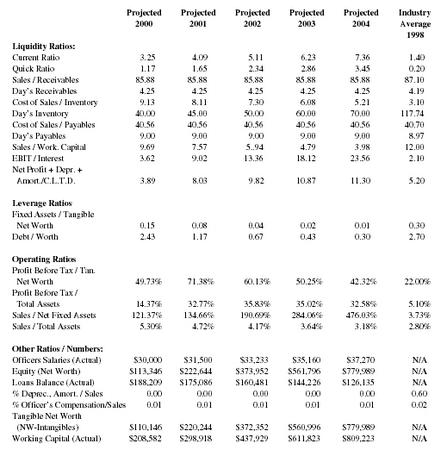

Ratio Comparison

| Projected 2000 | Projected 2001 | Projected 2002 | Projected 2003 | Projected 2004 | Industry Average 1998 | |

| Liquidity Ratios: | ||||||

| Current Ratio | 3.25 | 4.09 | 5.11 | 6.23 | 7.36 | 1.40 |

| Quick Ratio | 1.17 | 1.65 | 2.34 | 2.86 | 3.45 | 0.20 |

| Sales /Receivables | 85.88 | 85.88 | 85.88 | 85.88 | 85.88 | 87.10 |

| Day's Receivables | 4.25 | 4.25 | 4.25 | 4.25 | 4.25 | 4.19 |

| Cost of Sales /Inventory | 9.13 | 8.11 | 7.30 | 6.08 | 5.21 | 3.10 |

| Day's Inventory | 40.00 | 45.00 | 50.00 | 60.00 | 70.00 | 117.74 |

| Cost of Sales /Payables | 40.56 | 40.56 | 40.56 | 40.56 | 40.56 | 40.70 |

| Day's Payables | 9.00 | 9.00 | 9.00 | 9.00 | 9.00 | 8.97 |

| Sales /Work. Capital | 9.69 | 7.57 | 5.94 | 4.79 | 3.98 | 12.00 |

| EBIT /Interest | 3.62 | 9.02 | 13.36 | 18.12 | 23.56 | 2.10 |

| Net Profit + Depr. + Amort./C.L.T.D. | 3.89 | 8.03 | 9.82 | 10.87 | 11.30 | 5.20 |

| Leverage Ratios | ||||||

| Fixed Assets /Tangible Net Worth | 0.15 | 0.08 | 0.04 | 0.02 | 0.01 | 0.30 |

| Debt /Worth | 2.43 | 1.17 | 0.67 | 0.43 | 0.30 | 2.70 |

| Operating Ratios | ||||||

| Profit Before Tax /Tan. Net Worth | 49.73% | 71.38% | 60.13% | 50.25% | 42.32% | 22.00% |

| Profit Before Tax /Total Assets | 14.37% | 32.77% | 35.83% | 35.02% | 32.58% | 5.10% |

| Sales /Net Fixed Assets | 121.37% | 134.66% | 190.69% | 284.06% | 476.03% | 3.73% |

| Sales /Total Assets | 5.30% | 4.72% | 4.17% | 3.64% | 3.18% | 2.80% |

| Other Ratios /Numbers: | ||||||

| Officers Salaries (Actual) | $30,000 | $31,500 | $33,233 | $35,160 | $37,270 | N/A |

| Equity (Net Worth) | $113,346 | $222,644 | $373,952 | $561,796 | $779,989 | N/A |

| Loans Balance (Actual) | $188,209 | $175,086 | $160,481 | $144,226 | $126,135 | N/A |

| % Deprec., Amort. /Sales | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.60 |

| % Officer's Compensation/Sales | 0.01 | 0.01 | 0.01 | 0.01 | 0.01 | 0.02 |

| Tangible Net Worth (NW-Intangibles) | $110,146 | $220,244 | $372,352 | $560,996 | $779,989 | N/A |

| Working Capital (Actual) | $208,582 | $298,918 | $437,929 | $611,823 | $809,223 | N/A |

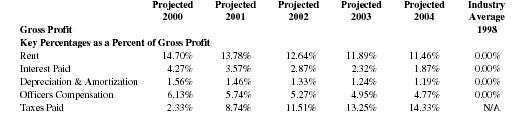

| Projected 2000 | Projected 2001 | Projected 2002 | Projected 2003 | Projected 2004 | Industry Average 1998 | |

| Gross Profit | ||||||

| Key Percentages as a Percent of Gross Profit | ||||||

| Rent | 14.70% | 13.78% | 12.64% | 11.89% | 11.46% | 0.00% |

| Interest Paid | 4.27% | 3.57% | 2.87% | 2.32% | 1.87% | 0.00% |

| Depreciation & Amortization | 1.56% | 1.46% | 1.33% | 1.24% | 1.19% | 0.00% |

| Officers Compensation | 6.13% | 5.74% | 5.27% | 4.95% | 4.77% | 0.00% |

| Taxes Paid | 2.33% | 8.74% | 11.51% | 13.25% | 14.33% | N/A |

Sources for the Industry Averages

Ratio analysis can be one of the most useful financial management tools. It becomes important when you look at the trend of each ratio over time. It also becomes important when compared to averages of a particular industry.

- Robert Morris Annual Statement Studies for 1995

- Industry Norms and Key Business Ratios 1995-1996

- Troy Almanac of Business and Industrial Financial Ratios for 1996

Ratio Analysis

Current Ratio is an approximate measure of a firm's ability to meet its current obligations and is calculated as Current Assets divided by Current Liabilities. This ratio shows an upward trend and indicates that if the company meets its goals it will be relatively more stable than the industry in general.

Revenue to Working Capital Ratio is a measure of the margin of protection for current creditors. This ratio is on a downward trend and indicates a good level of safety for creditors.

EBIT to interest Ratio is a measure of ability to meet annual interest payments. Since this ratio is above industry averages, the company should have no problem servicing its debt and can even service greater amounts of debt.

The Current Maturities Coverage Ratio measures the ability to pay current maturities of long term debt with cash flow from operations. It is calculated as Net Income Depreciation, Amortization divided by current portion of long term debt. This ratio shows an upward trend which indicates the company should be better to service its debt than the average company.

The Fixed Assets to Tangible Net Worth Ratio measures the extent to which owner's equity has been invested in the business. Since this ratio is on a downward trend, it provides an even larger "cushion" to creditors in the event of liquidation.

The Debt to Equity Ratio expresses the relationship between capital contributed by creditors and capital contributed by owners. This ratio shows a downward trend which would seem to indicate that if the company meets its goals that it will provide greater long-term financial safety for creditors.

The Earnings before Taxes to Total Assets Ratio expresses the pre-tax return on total assets and measures the effectiveness of management in employing available resources. Since this ratio is above industry averages, the company would be more efficient than the industry in its effective employment of resources.

The Revenue to Total Assets Ratio is a general measure of ability to generate revenue in relation to total assets. This ratio is above industry averages which can indicate that the company is efficient in using available resources to generate revenue as compared to the industry.

The Depreciation, Amortization to Revenue Ratio is a general measure of cost to generate revenue under the matching principal. Since this ratio is consistently below industry averages it would seem to indicate that the company is more efficient generating revenue as compared to the industry.

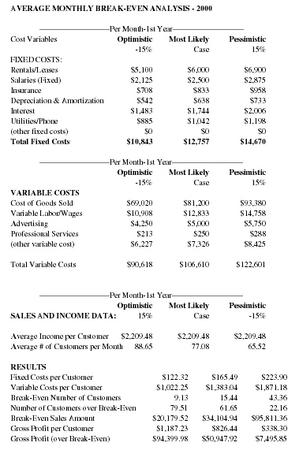

First Year Break-Even Analysis (Average, Optimistic, and Pessimistic Cases)

| AVERAGE MONTHLY BREAK-EVEN ANALYSIS - 2000 | |||||

| —————————Per Month-1stYear————————— | |||||

| Cost Variables |

Optimistic

-15% |

Most Likely

Case |

Pessimistic

15% |

||

| FIXED COSTS: | |||||

| Rentals/Leases | $5,100 | $6,000 | $6,900 | ||

| Salaries (Fixed) | $2,125 | $2,500 | $2,875 | ||

| Insurance | $708 | $833 | $958 | ||

| Depreciation & Amortization | $542 | $638 | $733 | ||

| Interest | $1,483 | $1,744 | $2,006 | ||

| Utilities/Phone | $885 | $1,042 | $1,198 | ||

| (other fixed costs) | $0 | $0 | $0 | ||

| Total Fixed Costs | $10,843 | $12,757 | $14,670 | ||

| —————————Per Month-1st Year————————— | |||||

|

Optimistic

-15% |

Most Likely

Case |

Pessimistic

15% |

|||

| VARIABLE COSTS | |||||

| Cost of Goods Sold | $69,020 | $81,200 | $93,380 | ||

| Variable Labor/Wages | $10,908 | $12,833 | $14,758 | ||

| Advertising | $4,250 | $5,000 | $5,750 | ||

| Professional Services | $213 | $250 | $288 | ||

| (other variable cost) | $6,227 | $7,326 | $8,425 | ||

| Total Variable Costs | $90,618 | $106,610 | $122,601 | ||

| —————————Per Month-1st Year————————— | |||||

|

Optimistic

-15% |

Most Likely

Case |

Pessimistic

15% |

|||

| SALES AND INCOME DATA: | |||||

| Average Income per Customer | $2,209.48 | $2,209.48 | $2,209.48 | ||

| Average # of Customers per Month | 88.65 | 77.08 | 65.52 | ||

| RESULTS | |||||

| Fixed Costs per Customer | $122.32 | $165.49 | $223.90 | ||

| Variable Costs per Customer | $1,022.25 | $1,383.04 | $1,871.18 | ||

| Break-Even Number of Customers | 9.13 | 15.44 | 43.36 | ||

| Number of Customers over Break-Even | 79.51 | 61.65 | 22.16 | ||

| Break-Even Sales Amount | $20,179.52 | $34,104.94 | $95,811.36 | ||

| Gross Profit per Customer | $1,187.23 | $826.44 | $338.30 | ||

| Gross Profit (over Break-Even) | $94,399.98 | $50,947.92 | $7,495.85 | ||

Break-Even Analysis is a mathematical technique for analyzing the relationship between profits and fixed and variable costs. It is also a profit planning tool for calculating the point at which sales will equal costs. The above analysis indicates the first year break-even number of customers at 3,716 per month and break-even income at $52,699.69 per month. Anything over these amounts will be profit.

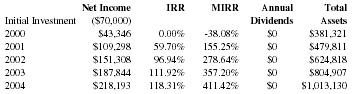

Rates of Return for The Family Bowl

| Net Income | IRR | MIRR |

Annual

Dividends |

Total

Assets |

|

| Initial Investment | ($70,000) | ||||

| 2000 | $43,346 | 0.00% | -38.08% | $0 | $381,321 |

| 2001 | $109,298 | 59.70% | 155.25% | $0 | $479,811 |

| 2002 | $151,308 | 96.94% | 278.64% | $0 | $624,818 |

| 2003 | $187,844 | 111.92% | 357.20% | $0 | $804,907 |

| 2004 | $218,193 | 118.31% | 411.42% | $0 | $1,013,130 |

ASSUMPTIONS:

Income figures are after taxes

Dividend Payout = 50% of After Tax Income

Reinvestment rate = 7%

IRR = INTERNAL RATE OF RETURN

MIRR = MODIFIED RATE OF RETURN

ROI = RATE OF RETURN ON OWNER'S INVESTMENT

ROA = RATE OF RETURN ON TOTAL ASSETS

IRR = the interest rate received for an investment and income that occur at regular periods

MIRR = adds the cost of funds and interest received on reinvestment of cash to the IRR

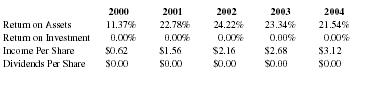

| 2000 | 2001 | 2002 | 2003 | 2004 | |

| Return on Assets | 11.37% | 22.78% | 24.22% | 23.34% | 21.54% |

| Return on Investment | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% |

| Income Per Share | $0.62 | $1.56 | $2.16 | $2.68 | $3.12 |

| Dividends Per Share | $0.00 | $0.00 | $0.00 | $0.00 | $0.00 |

CONCLUSIONS AND SUMMARY

We feel that the type of company and service we are proposing is hitting the market at just the right time. We plan to fully repay the loan by the end of the third year. However, we will schedule repayments over ten years to give us flexibility. By applying our conservative projections, income for the first year is expected to be $21,194 after taxes and debt service. This will rise to $76,822 in the second and $124,363 by the fifth year. The business should be open for business by spring of 2000.

Comment about this article, ask questions, or add new information about this topic: