SIC 1542

GENERAL CONTRACTORS—NONRESIDENTIAL BUILDINGS, OTHER THAN INDUSTRIAL

BUILDINGS AND WAREHOUSES

This category covers general contractors primarily engaged in the construction, alteration, remodeling, repair, and renovation of nonresidential buildings, other than industrial buildings and warehouses. Included are nonresidential buildings of commercial, institutional, religious, or recreational nature, such as office buildings, churches and synagogues, hospitals, museums and schools, restaurants and shopping centers, and stadiums. General contractors primarily engaged in the construction of industrial buildings and warehouses are classified in SIC 1541: General Contractors—Industrial Buildings and Warehouses.

NAICS Code(s)

233320 (Commercial and Institutional Building Construction)

As with the construction industry in general, nonresidential construction had benefited from a surging U.S. economy in the late 1990s. The demand and spending for all types of construction in this sector was commensurate with general economic strength, measured by gross domestic product and interest rates. When the economy began to falter at the turn of the twenty-first century, the nonresidential construction began to feel the pinch. Although residential construction was bolstered by interest rates that dipped to lows not seen since the 1950s, nonresidential construction experienced no such cushion. Businesses of all kinds began to curb spending on new and existing construction projects.

Along with economic strength, the specific construction categories of this sector are further affected by a range of variables, such as demographic trends, legislation regarding public expenditures and business developments, and social trends. Private nonresidential construction in the United States has fluctuated according to the success of key sectors such as office buildings and institutions. Nonresidential construction spending dropped by 6 percent in 2003 as even the strongest sectors, such as healthcare construction, began to see previously rapid growth rates slow.

The states that experienced the greatest levels of construction activity in this sector included California and Texas.

Office Construction. The 1980s saw tremendous growth in new office construction, but the overproduction and subsequent economic recession resulted in such a glut that vacancy rates became a nationwide problem. In 1983, the national metropolitan office vacancy rate stood at approximately 12 percent; by 1990, that rate had risen to 17 percent and peaked at 19 percent two years later. In 1998 the rate was at its lowest mark since the early 1980s, at 8.9 percent. However, by early 2003, the office vacancy rate had jumped back up to 16.5 percent.

Office construction spending experienced a long-awaited resurgence in the late 1990s, from $36.2 billion in 1997 to $47.5 billion in 1999. While this was excellent news for contractors, 1999 revenues were still 35 percent below their record 1985 level. As the economy as a whole cooled off from its late 1990s surge, the rate of office building construction growth slowed considerably to roughly $43 billion in 2002 and to $39 billion in 2003. Meanwhile, lending institutions, which had eased some of their restrictions on commercial real estate loans, began to tighten up lending requirements. Eyeing the slower growth rate for white collar employment, as well as the economic trend toward downsizing, builders wary of a repeat of the late 1980s disaster were expected to try and rein in runaway construction.

Retail Construction. In contrast to office construction, the retail construction market has remained strong since the 1980s. Spending on retail construction rose steadily during the late 1990s, from $42 billion in 1996 to $55.4 billion in 1999. About half the value in this category is related to the construction of shopping centers. Especially in recent years, such construction was geared toward big box stores—large non-mall discount stores specializing in focused product categories.

According to a December 2002 issue of Chain Store Age, the 25 largest U.S. retailers opened a total of 5,935 new stores in 2002, compared to 5,843 in 2001. In addition, square footage in these new stores reflected a 6.4 percent increase over the size of existing stores. Leading U.S. retailers also continued to spend construction dollars on remodeling existing stores. Supermarkets, in particular, were investing more capital into improving existing stores than on opening new units. Supermarket companies engaged in store remodeling grew from 22 percent to 38 percent between 1997 and 2001. In fact, supermarket store openings fell to a ten-year low in 2001. Offsetting the impact of this decline, however, was the fact that store closings had also reached a decade low rate. The new supermarkets that did open in 2001 boasted square footage of 46,750, compared to 44,072 a year earlier.

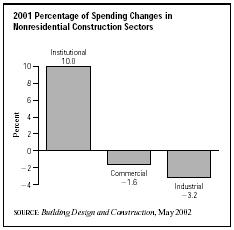

Institutional Construction. This sector includes a wide range of building types, including hospitals, schools, prisons, government buildings, and others. This type of construction has generally been more stable than all other sectors of nonresidential construction. As a result, it commands an increasing share—more than 60 percent as of the early 2000s—of total industry spending. Compared to industrial construction spending, which declined by 3.2 percent in 2001, and to commercial construction spending, which dipped 1.6 percent that year, spending on institutional construction grew 10 percent in 2001.

Educational building construction was very healthy in the late 1990s, with optimistic forecasts into the following decade. Sales in 1998 reached $39.5 billion and were expected to increase to $44.0 billion by 2000. Furthermore, as more schools placed a priority on full Internet service and technological facilities, the construction of new buildings and remodeling of existing ones was expected to follow. However, drastic cuts in educational funding in the early 2000s curtailed construction considerably in this sector. Seventy percent of this construction was of primary and secondary schooling facilities, while colleges, universities, and other educational institutions accounted for the remainder. The vast majority of this construction (80 percent) was for public institutions, though that figure was likely to diminish as state and local budgets continued to be strained while calls for voucher programs and other shifts toward private schooling increased.

The construction of healthcare facilities was largely dependent on legislative activity, which was in an uncertain state of limbo in the late 1990s. As a result, spending was down slightly in this sector, though much less for private hospitals than for public care facilities. Seventy percent of spending in this sector went toward hospitals and clinics, though nursing homes and outpatient centers claimed an increasing proportion of the market. More optimistically, however, analysts expect healthcare facilities to be among the fastest-growing sectors in the entire construction industry in the early 2000s. An aging population is a prime factor for this projected growth, especially as nursing homes and similar facilities flourish. Another indicator for growth is the age of existing facilities. According to an August 2002 issue of Heath Care Strategic Management, "In many cities, hospital plants are decaying beneath the surface, with out-of-date chillers and boilers, asbestos in the walls, and outdated signage … now it's time for hospital to play catch-up."

Industry Leaders

While the majority of companies engaged in nonresidential construction other than industrial buildings and warehouses employed fewer than 8 workers, a handful of firms commanded a substantial market share; however, most of those firms' operations included construction activity that extended beyond what fits into this industry.

HBE Corporation was established in 1960 and employed 9,100 workers in 2002. Its flagship operation is HBE Hospital Building and Equipment Company, which designs, plans, and builds healthcare facilities. HBE also performs construction activity for the financial services industry, building banks and credit unions. Sales totaled $625 million in 2002, compared to $1.3 billion in 1998.

Hellmuth, Obeta, and Kassabaum, otherwise known as HOK Group, Inc., engaged in a wide range of construction activities, including commercial, recreational, and institutional facilities, including U.S. government buildings. The firm maintains a payroll of more than 1,600 workers and posted sales of $309 million in 2002.

Other leading firms in 2002 included: Clark Construction Group of Bethesda, Maryland, with 4,000 employees and sales of $2 billion; Perini Corporation of Framingham, Massachusetts, with 2,400 employees and sales of $1.4 billion; and Turner Corporation of New York, New York, with 4,700 employees and $6.0 billion in sales.

Further Reading

"Construction Spending Continues Its Climb." Real Estate Weekly, 14 January 2004.

Delano, Daryl. "Clouds Over Industrial Sector Won't Break Until '03." Building Design and Construction, May 2002.

"Home Building Strong, But Commercial Construction Falters." Indianapolis Business Journal, 17 February 2003.

"Hospital Construction Boom Looms, Changes to Affect Facilities' Design." Health Care Strategic Management, August 2002.

Comment about this article, ask questions, or add new information about this topic: