SIC 1761

ROOFING, SIDING, AND SHEET METAL WORK

Special trade contractors primarily engaged in the installation of roofing, siding, and sheet metal work. Sheet metal work performed by plumbing, heating, and air-conditioning contractors in conjunction with the installation of plumbing, heating, and air-conditioning equipment are classified in SIC 1711: Plumbing, Heating, and Air-Conditioning.

NAICS Code(s)

235610 (Roofing, Siding, and Sheet Metal Contractors)

Industry Snapshot

Construction services offered by the roofing, siding, and sheet metal industry include architectural sheet metal work; erection and repair of metal ceilings; copper smithing in connection with construction work; metal downspout installation; sheet metal duct work; metal gutter installation; roof spraying, painting, or coating; all roofing work, including repairs; siding installation; skylight installation; and tin smithing in connection with construction work.

Organization and Structure

The construction industry can be divided into three major divisions: general building contractors, heavy construction contractors, and special trade contractors, which include those who install roofing. General building contractors build residential, industrial, and commercial buildings, while heavy construction contractors build structures such as roads, highways, and bridges.

Special trade contractors usually focus on one trade and work under the direction of general contractors, architects, or property owners. Beyond completing their work to specification, special trade contractors have no responsibility for building the structure in its entirety.

Besides new installations or re-roofing, the market can be divided by type of roof, either low-slope or steep-slope. The low-slope market includes commercial and industrial buildings and some apartment houses. The steep-slope market is primarily residential.

Sometimes working in conjunction with architects, roofing contractors choose from a selection of materials that include thermoset single plies (e.g., EPDM, CSPE/Hypalon, PVC), built-up roofing (BUR), and fiberglass, and organic asphalt shingles. In the re-roofing industry the contractor decides what type of roofing system to use and which manufacturer's product to install. With new installations the architect usually decides which roof system to use, and, most of the time, the contractor still chooses the manufacturer.

Background and Development

For roofers who work predominantly on newly built homes, the state of the housing industry is crucial. The recession of the early 1990s hit the housing market and roofing contractors particularly hard. Renovation and repair increased slowly but steadily during the mid-1990s, reaching $69.5 billion by 1995. The recovery of the housing market led to significant increases in both re-roofing and new construction in the West (86.4 percent), with moderate increases in the Northeast (36.0 percent) and Midwest (16.8 percent). In the South, however, there was a 17.4 percent decline.

The state of the home remodeling industry also greatly affected roofing contractors, since a large percentage of their business derives from re-roofing projects. The residential repair and remodeling (R&R) market was once thought to be recession-proof. The recession of the early 1990s proved that theory wrong, but the market recovered and increased to about $113.5 billion by 1993.

Roofing contractors who worked in the remodeling sector stood to benefit from two major demographic factors. First, as baby boomers entered their high income-producing years, they would be purchasing new or existing homes. Also, the U.S. housing stock became fairly old. Of the 100 million homes in the United States, nearly 60 percent were at least 22 years old.

Some roofing contractors rebounded from the recession with a booming roofing business. These contractors were re-roofing faulty plywood that was widely used in the eastern and southern United States in the 1980s. The chemically treated, fire-resistant roofing substance known as FRT deteriorated and lost strength when subjected to high heat and humidity, causing roofs to sag and leak. It was estimated that between 250,000 and 1 million roofs would need to be replaced.

Current Conditions

According to the latest figures available from the U.S. Census Bureau, the U.S. roofing, siding, and sheet metal contracting industry comprises more than 30,000 companies and earns more than $24 billion in total revenues, the largest portion of which is generated by architectural sheet metal contractors, followed by carpentry contractors; heating, ventilation, and air-conditioning contractors; roofing contractors; siding contractors; and specialty sheet metal contractors.

Due to the economic downturn of the early 2000s, both the roofing and the siding industries felt the pinch of reduced commercial and industrial construction, despite the frenetic pace of residential construction. Based on estimates released by the Freedonia Group, demand for

siding between 2002 and 2005 will grow less than 1 percent, reaching 109 million squares, worth $9.2 billion, in 2005. Fiber cement siding is expected to lead industry growth with 5 percent gains each year due to its increasingly popularity over wood siding products. However, due to booming residential construction and remodeling, vinyl siding will likely remain the leading industry segment in terms of volume. Due to signs of recovery in the U.S. economy, the roofing industry expects increased sales in 2004, according to the National Roofing Contractors Association.

Industry Leaders

The roofing industry typically consists of numerous small roofing firms and a few larger companies, which often operate additional construction and manufacturing businesses. Among the largest companies involved in the roofing, siding, and sheet metal industry, Bradco Supply Corp. of Avenel, New Jersey, employed 2,000 people in 2003 and had estimated annual sales of $995 million, reflecting 17 percent growths from 2002. Privately owned Pacific Coast Building Products Inc. of Sacramento, California, had roughly 2,500 employees and approximate sales of $400 million. Bryant Universal Roofing Inc. of Phoenix, Arizona, had 1,200 employees and sales of $110 million.

Workforce

Workers in the sheet metal industry typically learn their trade through apprenticeship, including four or five years of hands-on training at job sites and at least 144 hours per year of classroom education. Others start as helpers, learning informally from experienced workers on the job and progressing gradually to more skilled tasks. They often study at vocational schools to supplement their practical experience.

On-the-job training is the most common way of entering the roofing industry, but some people learn the trade through a three-year apprenticeship that typically includes 144 hours of classroom education and at least 2,000 hours of hands-on training at job sites. Labor unions usually offer roofing and sheet metal work apprenticeship programs, often under the auspices of local union-management joint training committees.

According to the Occupational Outlook Handbook, roofers held approximately 166,000 jobs in 2002. Self-employed roofers represented one out of every three jobs and mainly specialized in residential work. Some roofers were members of the United Union of Roofers, Waterproofers & Allied Workers. Average hourly earnings for roofers in 2002 were $14.51.

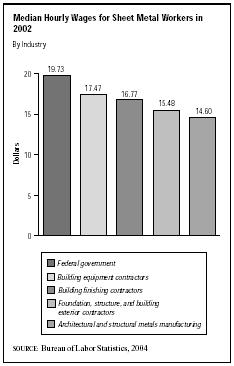

Sheet metal workers held approximately 205,000 jobs in 2002. Roughly 66 percent were employed in the construction industry, half of whom worked for plumbing, heating, and air-conditioning contractors. Most of the others worked for roofing and sheet metal contractors, and a few worked for other general or special trade contractors. Relatively few sheet metal workers were self-employed. Most were members of the Sheet Metal Workers' International Association. Average hourly earnings in 2002 were $16.62.

Between 2002 and 2012, employment in the roofing and sheet metal industries was expected to grow by 18.8 percent and 22.8 percent, respectively, according to the Bureau of Labor Statistics.

Further Reading

"Fiber Cement Opportunities for U.S. Siding Industry." Forest Products Journal, January 2002.

U.S. Census Bureau. Economic Census 1997. Washington, DC: GPO, 2000.

U.S. Department of Labor. Bureau of Labor Statistics. Occupational Outlook Handbook, 2004-05. Washington, DC, 2004. Available from http://www.bls.gov/oco/print/ocos203.htm .

Zissman, Mindi. "Roofing Industry Looks for Recovery." Building Design and Construction, September 2003.

Comment about this article, ask questions, or add new information about this topic: