SIC 3699

ELECTRICAL MACHINERY, EQUIPMENT, AND SUPPLIES, NOT ELSEWHERE CLASSIFIED

This classification comprises establishments primarily engaged in manufacturing electrical machinery, equipment, and supplies, not elsewhere classified, including high-energy particle acceleration systems and equipment, electronic simulators, appliance and extension cords, bells and chimes, and insect traps.

NAICS Code(s)

333319 (Other Commercial and Service Industry Machinery Manufacturing)

333618 (Other Engine Equipment Manufacturing)

334119 (Other Computer Peripheral Equipment Manufacturing)

Industry Snapshot

Industries classified in the Standard Industrial Classification Manual as including products "not elsewhere classified" produce miscellaneous products that share a broadly defined similarity but rarely are produced by the same type of manufacturers. These "not elsewhere" classifications (usually abbreviated as NEC) are created to retain the integrity or homogeneity of other industry classifications, which otherwise would become muddled by the inclusion of products that are instead consigned to NEC industries. Consequently, NEC industries frequently include distinctly separate types of manufacturers, competing in entirely different markets, and manufacturing a diverse assortment of products.

SIC 3699: Electrical Machinery, Equipment, and Supplies, Not Elsewhere Classified includes various types of amplifiers, such as magnetic and pulse amplifiers, maser amplifiers, DC amplifiers, and differential and facsimile amplifiers, but excludes audio or video amplifiers. This category also includes various types of particle accelerators (also known as atom smashers), automatic garage door openers, scientific electronic equipment, electronic kits to be assembled by the purchaser, and consumer electronic equipment.

This industry also manufactures electronic teaching machines, teaching aids, trainers, and simulators. There is a category for laser systems and equipment, except communication, which includes laser designator/ranging equipment, laser instrumentation equipment such as laboratory alignment devices and surveying equipment, industrial laser equipment, and medical laser equipment. The electrical products, NEC category includes a host of diverse products such as electric gongs, bells, and chimes; electric Christmas tree lighting sets; electric insect killers; electric fence chargers; and electric outboard motors for boats.

The apparatus wire and cordage product category includes appliance cords manufactured primarily from purchased insulated wire for various household appliances, including electric irons, grills, and waffle irons. And finally, the ultrasonic equipment category, except for medical and dental use, includes ultrasonic equipment manufactured for industrial applications, such as ultrasonic cleaners, drills, welders, and solderers.

Although this classification includes a multitude of diverse products, the industry's core businesses—those products that generate the greatest amount of revenue for manufacturers—are the primary products from the three largest product categories. Accordingly, the miscellaneous electrical machinery, equipment, and supplies industry essentially includes manufacturers of consumer electronic products, particle accelerators, flight simulators, and laser equipment.

The majority of the products that constitute the industry's core businesses were added to its classification in 1987, when SIC 3699: Electrical Machinery, Equipment, and Supplies, Not Elsewhere Classified was reclassified. Added to the industry's classification were particle accelerators, flight simulators, laser equipment, and ultrasonic equipment, as well as other less significant products. The effect of this reclassification on the industry's revenue total was enormous.

Nonetheless, as with most manufacturing segments, this industry was hit hard after the U.S. economy took a nosedive following the terrorist attacks of September 11,2001. The weakening of the U.S. dollar, combined with few product orders and shipments, was only beginning to recover toward the middle of the 2000s, and the recovery was very slow—not more than 2 percent annually in most segments.

Organization and Structure

The miscellaneous electrical equipment and supplies industry became a much more densely populated industry following its reclassification in 1987. Prior to that year, approximately 700 companies in the United States were involved in manufacturing products ascribed to the industry. Once reclassified, the industry's roster nearly doubled to include 1,324 manufacturers and 1,379 individual manufacturing establishments, more than twice as many individual, separate manufacturing establishments as were in operation the previous year. From 1987 into the 1990s, however, the number of manufacturers in the industry declined, falling to 1,185 in 1990 and 912 by 1993.

During the 1980s the industry's sales volume rose steadily before and after the reclassification, but realized a greater rate of growth before being reclassified. From 1982 to 1986 aggregate revenue increased nearly 30 percent, more than twice as much as the percentage increase from 1987 to 1990. In 1990 the industry's sales volume reached $5.8 billion, an increase of $792.0 million from the total recorded in 1987. By 1994, however, the value of industry shipments had fallen to $5.1 billion.

In the mid-1990s individual manufacturing establishments in the industry averaged $6.2 million in annual revenue, about 65 percent of the sales volume generated by the typical manufacturing establishment in industries overall. Although generating less revenue than the industrywide average, electrical equipment and supply manufacturing plants had an investment per establishment in 1994 that was only 48 percent of that found in other industries. This highlighted the labor-intensive nature of the work and the relative ease of entry into the market for potential manufacturers. Despite this, the number of establishments in the industry dropped from more than 1,300 in 1987 to about 800 in 1994, and it continued to drop into the new century, as did employment.

Background and Development

Each product segment composing the miscellaneous electrical machinery and equipment industry possesses a history distinct from the other products grouped into this classification. For the most part, the manufacturers of these disparate product categories have little in common with each other and rarely compete in the same market. Manufacturers of flight simulators, for example, have little in common with manufacturers of automatic garage door openers and compete for market share in entirely different markets. Essentially then, the miscellaneous electrical machinery and equipment industry includes six smaller, subsidiary industries—three of lesser importance and three of greater importance—each of which has experienced different paths of development.

These subsidiary industries, however, do share one common thread; their products depend on electricity and a branch of science and engineering closely related to the science of electricity: electronics. Some of the products within the industry rely solely on electricity to operate, but generally these products are of lesser importance to the growth of the industry as a whole. Rather, many of the more important products that contribute significantly to the industry's growth rely on electronic technology, particularly those products added to the industry after the 1987 reclassification. Accordingly, without electrical power and, perhaps more important, without the emergence of electronics, the miscellaneous electrical equipment and supplies industry would not exist.

Before the electrical machinery industry could emerge as representing an appreciable portion of all manufacturing activity in the United States, sufficient electrical power capacity had to be developed. By the beginning of the twentieth century enough electrical power—2.2 billion kilowatt hours in 1902—was being generated in the United States to engender the electrical machinery industry as a viable sector of U.S. manufacturing. At that time, the electrical machinery industry accounted for roughly 1 percent of the total manufacturing activity in the country, a proportion that would increase to 4.5 percent by 1929 and reach 6.6 percent by the beginning of the 1960s. During those six decades of growth, the electrical machinery industry expanded more than six times as rapidly as did American industry as a whole, and the level of technological sophistication in the country increased sufficiently to encourage the production of electronic products in earnest.

In 1907 American inventor Lee De Forest ushered in the electronic age with his development of a three-electrode vacuum tube, which he called an "audion," making it possible to amplify weak radio signals and transmit them over long distances, a capability earlier vacuum tubes failed to provide. From this discovery, the world was introduced to the radio, creating a small but lucrative market for a new breed of manufacturer: the radio maker. These manufacturers flourished during the 1920s and 1930s, but their numbers began to dwindle as the United States neared involvement in World War II. Infused with orders from the U.S. government for electronic equipment to aid in the war effort, the electronic industry was buoyed for several years during the war, but at its conclusion the small group of electronics manufacturers still represented only slightly more than a fledgling industry, employing relatively few people, contributing a comparatively small amount to the national economy, and amounting to little more than $500 million at the factory level.

The industry's growth during its first 40 years of existence only appeared lackluster in retrospect, however, for in the 10 years following the war the industry expanded at a tremendous pace, becoming the fifth largest industrial segment of the national economy by the late 1950s, employing more than 1 million people, and comprising more than 2,500 large and small manufacturers. By 1957 the industry's annual sales volume at the manufacturer level had increased 14 times in the previous 10 years, reaching $7 billion. At the time, this was considered to be the most prolific growth rate in the shortest time span of any industry in U.S. history. This prodigious growth witnessed the development of many innovative electronic applications, which inspired a host of sophisticated products for commercial, industrial, and consumer use, including the primary products in the miscellaneous electrical machinery and equipment industry. During this decade, flight simulators, an assortment of consumer electronic products, particle accelerators, and lasers each emerged as substantial, revenue-generating products.

Two U.S. physicists, Arthur L. Schawlow and Charles H. Townes, first propounded the theory of the laser (an acronym for "light amplification by stimulated emission of radiation") in 1958, which was based on Townes' development of the maser ("microwave amplification by stimulated emission of radiation") roughly eight years earlier, when the electronics industry was beginning to expand exponentially. Two years after the idea was born, the first laser, a ruby laser, was constructed by Theodore H. Maiman in 1960. Particle accelerators, first developed by John D. Cockcroft and Ernest T. S. Walton in 1932, did not become commercially viable products until the 1950s, their evolution largely attributable to the work of Robert J. Van de Graaff and the company he helped found in 1946, High Voltage Engineering Corp. During the 1950s, a decade of enormous growth in the electronics industry, flight simulators also appeared as a commercially viable product, although they had been in existence for a number of years. Receiving a significant boost from their military applications during World War II, flight simulators gained the attention of the burgeoning commercial airline industry, creating an incentive for electronics manufacturers to convert their facilities to the production of simulators.

From the 1950s forward, the major product categories of the miscellaneous electrical machinery industry were generating appreciable amounts of revenue, albeit from different markets. By the late 1950s, there were eight manufacturers worldwide producing particle accelerators. The largest of these, Van de Graaff's High Voltage Engineering Corp., controlled 40 percent of the $20 million global market. Although it was still a comparatively small market, industry pundits foresaw the market for particle accelerators increasing to nearly $80 million dollars by the mid-1960s. Their optimism stemmed from the various and remarkable industrial applications for particle accelerators, which were then beginning to over-shadow their scientific contributions, or at least command more of the limelight.

Functioning as a machine that synthetically produced radiation energy, particle accelerators were used in various production processes, from sterilizing surgical sutures after they had been packaged to irradiating wire and cable insulation used in missiles and jet aircraft, as well as other electronic gears exposed to high temperatures. Particle accelerators also could perform other feats, such as converting sawdust into digestible feed for livestock, transforming sugar into acid, and waterproofing shoe leather.

The main obstacle facing particle accelerator manufacturers as they entered the 1960s was the expensive nature of their business and the high price of their products. Some units sold for up to $150 million each, limiting the manufacturers' clientele to those businesses for which the high price tag and operating costs of accelerators were offset by their ability to perform a task that otherwise could not be completed. Consequently, there were only 250 particle accelerators in the world by the beginning of the 1960s, but prices were coming down rapidly as manufacturers augmented the world supply by producing 40 to 45 units per year.

As the push toward reducing the manufacturing cost and operating cost of particle accelerators progressed—the cost per kilowatt hour, for example, was cut in third in just two years—scientists also sought to construct bigger units. The bigger the accelerator, the greater the speed at which particles could be slammed against each other, providing scientists with more information about the basic laws of matter with each incremental increase in size and power. Particle accelerator power, measured by the number of electron volts produced by the accelerated particles, increased throughout the 1960s and 1970s, standing at 30 billion electron volts at the beginning of the 1960s, then increasing to 500 billion electron volts by the beginning of the 1970s. These and further advances in power and research broadened the particle accelerator's applicability for industrial and medical use, particularly in the form of powerful X-ray machines used to detect hidden flaws in metal castings, in the production of semiconductors, and to diagnose and treat cancer.

From the first primitive trainers manufactured in the 1940s by Singer-Link to the early 1990s, the market for flight simulators, marine simulators, and other electronic training devices remained a vital component of the miscellaneous electrical machinery and equipment industry, despite being heavily dependent on military spending, which has fluctuated dramatically since the emergence of simulators. Military sales, both to the U.S. government and to other countries, essentially created the industry during World War II and fueled its growth into the 1950s. The growth of the civilian aircraft industry and the airline industry during the 1950s added to this business. Yet another market segment for flight simulator manufacturers emerged during that decade, when the Soviet Union launched the world's first space satellite in 1957 and formally christened the Space Age. Thus, in quick succession three primary markets for the flight simulator industry were created, inducing a growing number of simulator manufacturers to replicate as best they could the rapid technological advancements taking place in the burgeoning aerospace industry.

The bulk of flight simulator manufacturers' space simulation business came soon after the Soviets launched their satellite, when the frenetic race to reach the moon began. In the early 1960s the U.S. government earmarked $65 billion to be spent over a seven-year period to win the race, $300 million of which simulator manufacturers could expect to garner. Initially, more 200 space simulators were ordered, as NASA sought to simulate each stage of a moon voyage.

While space simulators were intended to provide training for hypothetical equipment traveling in a hypothetical environment, flight simulators for military and civilian aircraft replicated existing aircraft and would prove to be the linchpin of simulator manufacturers' financial stability in the years to come. As the costs of operating aircraft increased dramatically, simulating the flight without having to pay for fuel and ground support—or risking the destruction of the plane—became a desirable alternative. Consequently, any significant decline in military spending usually had an insignificant effect on simulator manufacturers, since their products could be construed as cost-saving purchases. For the industry's commercial clientele, the same rationale held true, particularly during the energy crises in the early and mid-1970s. With the rising cost of fuel, many airlines opted for simulators to augment their traditional pilot and crew training. To be sure, simulator manufacturers were negatively affected by the usual economic exigencies, and their market was comparatively small, but their business was not affected as severely when economic conditions soured as were other manufacturers dependent on the aerospace industry.

Simulator manufacturers' role in the civilian aircraft industry received a tremendous boost in 1981, when the Federal Aviation Administration authorized the training of pilots by Braniff Airlines without its pilots recording any actual flight time. Instead, pilots trained in a 747 simulator manufactured by U.K.-based Rediffusion. With this edict, the simulator industry reached "total realism," spurring the industry's growth for the decade.

As the 1990s neared its close, one product category that had been a traditional leader in the industry overall was predicted to fall behind in product shipments. Electronic teaching machines and trainers, which composed 27 percent of the industry as recently as 1992, were expected to fall behind electronic systems and equipment, NEC (including automatic garage door openers), and laser systems and equipment. The U.S. Census Bureau predicted that by the late 1990s, electronic systems and equipment, NEC would be 28 percent of the industry; laser systems, 20 percent; and teaching machines and trainers would account for only about 17 percent.

Particle acceleration scientists and their allied industry got a boost in the late 1990s as the Large Hadron Collider appeared on track to be fully operational by the year 2005, three years ahead of schedule. The collider, which will represent a total cost of $6 billion by its completion, was predicted to be the most powerful accelerator ever built. Constructed at CERN, the European Organization for Nuclear Research, at their particle physics center near Geneva, the collider was to be funded by 19 member nations, including the United States.

The development of the Large Hadron Collider was some consolation to U.S. industry participants disappointed in the abandonment of the 54-mile-long particle accelerator known as the Superconducting Supercollider. Due to ballooning cost estimates, Congress voted to cancel the project in 1993—after more than $2 billion dollars had been spent to finish roughly 20 percent of the accelerator—and allotted $615 million to formally terminate construction.

Prognostications for flight simulator manufacturers generally were encouraging as the industry emerged from the economic recession of the early 1990s. Increases were predicted in the size of the world's aircraft transport fleet through the year 2005, which led industry observers to project a nearly 150 percent increase in the demand for full-flight simulators. In Asia and the Pacific regions, aircraft operators during this period were expected to require 200 percent more simulators than they possessed in 1992, while Western European aircraft operators were predicted to require 155 percent more simulators. Similar percentage increases were predicted by North American and Latin American operators. Driving this increased demand, which promised to expand the size of the simulator industry greatly, was a projected growth in demand for very-long-range aircraft, or those aircraft designed to fly distances greater than 5,500 nautical miles.

That scenario was not embraced wholly by the U.S. Census Bureau, however. It tracked an erosion of the market share of trainers and simulators as the 1990s progressed. That erosion was due at least partly to the growing strength of two other industry segments, electronic systems and equipment, NEC, and laser systems and equipment. Even discounting the gains of those segments, however, the trainer and simulator segment exhibited real declines in the 1990s. Its 1992 value of product shipments was $1.2 billion, about 27 percent of the entire industry's shipments. The segment's shipments dropped to $932.0 million in 1993, and to $840.0 million in 1994, about 18 percent of the total. The segment's $874.0 million value of 1995 shipments represented a resurgence, however, driven by new aircraft technologies requiring new simulators.

Current Conditions

After the terrorist attacks of September 11, 2001, and the subsequent fall of the U.S. economy, manufacturing industries took a huge hit. In the early 2000s, the weakened dollar, lack of consumer confidence, and subsequent lack of company earnings, not to mention the surge of corporate scandals reported in the popular media, contributed to the ongoing poor condition of the U.S. economy and the slow efforts at recovery.

In the electrical machinery, equipment, and supplies industry, the outlook was no better in 2002. Shipments were more than 7 percent lower than pre-9/11 levels, machine tool consumption was down nearly 31 percent, office construction declined more than 27 percent, and industrial construction was down a whopping 43 percent.

The only sector with a positive outlook for those in electrical manufacturing was the prognosis for residential construction, which was rising slowly but surely. By mid-2002, this construction market had risen to $23 billion, a six percent increase over the previous year.

Industry Leaders

In 2001, the industry leader was Synrad Inc. Based in Mukilteo, Washington, Synrad had $9.29 billion in revenue with just 100 employees. Founded in 1984, Synrad specialized in all-metal tube precision lasers for the industrial market. Designed for marking, cutting, and engraving, among other uses, the lasers operate more than 45,000 hours, with output powers ranging from 10 to 240W.

In second place was Boon Edam Inc. of Salt Lake City, Utah. The company, which reported 2001 revenue of $5.34 billion and 100 employees, specialized in the manufacture of security and revolving doors. Rounding out the top three companies in 2001 was Lunaire Ltd. of Williamsport, Pennsylvania. Lunaire had $5.18 billion in revenue and 200 employees. Its product brands included Lunaire Environmental, Gruenberg, Blue M, and Tenney Environmental.

The leader in money recovery systems was ICI Security Systems Inc., with three-fourths of this market segment in 2003. Its number one seller, the Security PAC Electronic Protection System, led the company's products designed for theft deterrence and the recovery of stolen money.

Workforce

In 1986, some 24,700 people were employed by the industry, the majority of whom were employed as production workers. One year later, after the reclassification, the industry's payroll swelled to include 60,300 employees and comprised nearly as many salaried employees as production workers. Before the reclassification, approximately 75 percent of the industry's workforce were employed as production workers, while the remaining 25 percent were employed as salaried workers performing administrative, technical, or managerial duties. After the inclusion of manufacturers involved in producing sophisticated, high-technology products the following year, the composition of the industry's workforce was nearly evenly divided between the two types of employees, with 47 percent working as salaried employees and 53 percent employed in production.

Following the reclassification, which more than doubled the size of the industry's workforce, total employment declined, dropping to almost 40,000 in the mid-1980s. Production workers bore the brunt of the decline, as more than 12,000 lost their jobs by 1994.

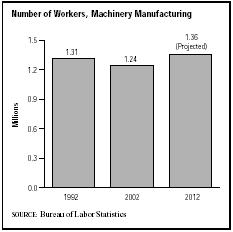

Employment in the machinery manufacturing sector as a whole fell from 1.3 million jobs in 1992 to 1.2 million in 2002, with continued annual decline projected into 2012. Production workers in electrical equipment and supplies manufacturing held only 245,300 jobs in mid-2002, nearly 12 percent fewer than the previous year.

Research and Technology

Some of the most striking research being done in the industry was in the area of particle physics. As the abandonment of the Superconducting Supercollider and the costs of the Large Hadron Collider made clear, advancements in atom smashing in the 1990s were stymied by the astronomical funding and expansive open spaces required to hurl atomic particles quickly enough through a tunnel. Eliminating the need for huge tunnels and their attendant cost occupied a number of researchers, who sought to create what essentially was a tabletop atom smasher. Researchers at the University of Michigan Center for Ultrafast Optical Science were able to generate and manipulate short, powerful laser pulses, which strip electrons from atoms to create a plasma of charged particles. The electric fields created focused the electrons into a tight beam. Using different methods, researchers at the University of California, Los Angeles, the University of Texas, and Argonne National Laboratory worked to achieve similar results.

Such focused beams, which could be manipulated by users, were predicted to make possible compact, relatively inexpensive devices to replace or at least supplement their elephantine counterparts. However, the energy generated by the smaller prototypes in the late 1990s was far short of that generated by large supercolliders. At that time, smaller, less expensive accelerators found their abilities best suited to medical uses, as opposed to studying the nature of matter itself.

Further Reading

"About Lasers." 23 March 2004. Available from http://www.synrad.com/LaserFacts/Aboutlasers.htm .

Baker, Deborah J., ed. Ward's Business Directory of US Private and Public Companies. Detroit, MI: Thomson Gale, 2003.

"Biggest Atom Smasher Rises on Illinois Prairie." Engineering News-Record, 6 August 1970.

Eby, Michael. "Not Much to Smile About." Electrical Construction & Maintenance, 1 July 2002.

"Extra Zip for Atom Smashers." Business Week, 27 March 1981.

"First Industrial Laser Retired to Smithsonian." Iron Age, 24 September 1979.

"First Name in Entrance Technology," 23 March 2004. Available from http://www.boonedam.nl/inc/home.htm .

Gutman, Walter K. "Atomic Alchemy." Barron's, 19 October 1959.

"Hurrah for Second Thoughts." The Economist, 27 June 1970.

Lazich, Robert S., ed. Market Share Reporter. Detroit, MI: Thomson Gale, 2004.

"Lunaire Limited Thermal Products and Test Solutions." 23 March 2004. Available from http://www.lunaire.com .

McKenna, James T. "Very-Long-Range Aircraft Seen Driving 150 Percent Rise in Simulator Demand." Aviation Week & Space Technology, 20 July 1992.

Moorman, Robert W. "From the Beginning." Air Transport World, August 1992.

Nordwall, Bruce D. "Airline Demand for Flight Simulators to Outstrip Growth in Transport Fleets." Aviation Week & Space Technology, 3 August 1992.

"Push for Biggest Atom Smasher." Business Week, 8 April 1961.

"Radiation for Industry." Chemical Week, 5 May 1962.

"Synrad CO2 Laser Technology," 2004. 23 March 2004. Available from http://www.synrad.com .

U.S. Department of Labor, Bureau of Labor Statistics. Economic and Employment Projections. 11 February 2004. Available from http://www.bls.gov/news.release/ecopro.toc.htm .

"Wanted: Bigger Atom Smashers." Business Week, 10 September 1960.

Whitehead, Ross. "Rapid Growth Ahead for Industrial Lasers." Industry Week, 28 April 1980.

Comment about this article, ask questions, or add new information about this topic: