SIC 2519

HOUSEHOLD FURNITURE, NOT ELSEWHERE CLASSIFIED

This industry category includes establishments primarily engaged in manufacturing reed, rattan, and other wicker furniture; plastics and fiberglass household furniture and cabinets; and household furniture not elsewhere classified.

NAICS Code(s)

337125 (Household Furniture (except Wood and Metal) Manufacturing)

Industry Snapshot

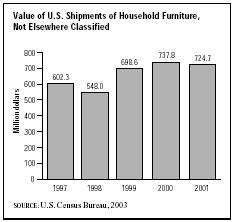

This industry, focusing largely, though not exclusively, on more specialized furniture production, was dominated in the late 1990s and early 2000s by small firms. Moreover, it was distinguished from most manufacturing sectors in that it was characterized by a trend toward more companies with fewer employees, against overall industrial trends. Of the 212 companies producing such furniture, only one-fifth maintained more than 20 employees; more than half had fewer than five. In all, the industry employed 4,923 people in 2000, down from 5,400 in 1995; of that total, 3,797 were production workers, who earned an average of $10.54 per hour. Shipments for all products in this category totaled $724.7 million in 2000, up from $602.3 million in 1997.

Background and Development

Wicker, Rattan, and Reed Furniture. Wicker furnishings have been used in American households since the seventeenth century. The first known craftsmen to advertise wicker furniture were early nineteenth-century basket weavers. During that period, straw and willow were replaced by rattan, which was imported by the East India Company.

In the mid-nineteenth century, wicker furniture, customarily styled with closely woven cane seats and looped reed backs and arms, became increasingly popular. Furniture

frames were constructed from hickory and oak pieces that were steamed and bent into shape, then wrapped with split cane. At that time, construction of wicker furniture changed from craft to industry.

Between 1875 and 1910, wicker furniture reached the height of its popularity, in part because of its association with exotic foreign countries. In 1917, Marshall B. Lloyd invented a wicker-weaving machine that used fiber material—the Lloyd Loom. Concurrently, many wicker manufacturers began to experiment with materials such as prairie grass and fiber. Wire grass, converted into a pliable twine and woven into furniture, was obtained from the prairie marshes of northwest America.

By the end of World War I, the skilled labor needed to weave wicker became scarce in the United States, and imports began replacing domestically manufactured goods. By the close of World War II, almost all wicker furniture sold in America was imported, a situation that continued in the early 2000s.

Plastics and Fiberglass Furniture. Although plastics had been developed in the late nineteenth century, it was not until 1909, when the American chemist Leo Baekeland developed Bakelite, that plastics gradually began to replace metal for body-shells in industrial applications. Baekeland, along with two Westinghouse Corporation engineers, Harold Faber and Daniel O'Connor, developed a laminate originally intended for electrical insulation. The development of this formula in 1913, however, eventually resulted in the establishment of the Formica Corporation. By the mid-1920s Formica's laminate was used to produce furniture.

With the demands for light-weight seat furniture brought on by the aircraft industry during World War II, the development of plastics for furniture construction increased. Two early pioneers of American furniture design, Eero Saarinen and Charles Eames, began experimenting with molded polyester in 1941. Saarinen's "Womb" chair, the first fiberglass design to be mass-produced in America, was manufactured by Knoll Associates in 1946. The chair remained in continuous production for more than four decades. In 1950 New York's Museum of Modern Art held an exhibition entitled "Organic Design in Home Furnishings." The prize-winning fiberglass armchair, designed by Charles Eames, was manufactured by the Herman Miller Furniture Company. Eames' molded plastic chair series, which also included a stacking chair, became one of the most basic and popular lines of American seating furniture.

Current Conditions

Due to the wave of consolidation among retail furniture outlets, furniture makers across all categories were forced to compete on the basis of access to distribution channels, with the larger firms typically gaining greater leverage in the process. While some of the major manufacturers in the miscellaneous household furniture category were able to establish inroads in this domain, the bulk of the industry's players had largely sidestepped the whole process, focused as they were on niche products and smaller-scale production facilities. These companies benefited greatly from the surge in e-commerce, allowing them to market their specialized products directly to customers. Wholesale outlets, home-shopping television, and mail-order distribution were the other primary marketing targets for these firms.

Just as the booming U.S. economy in the late 1990s boosted discretionary consumer spending on merchandise such as furniture, the recessionary conditions of the early 2000s undermined the performance of the furniture industry. After growing from $548 million in 1998 to $698.6 million in 1999 and to $737.8 million in 2000, shipments of household furniture except wood and metal declined to $724.7 million in 2001.

The surging number of home-office workers in the United States foreshadowed healthy sales in the early twenty-first century, as more and more individuals converted rooms in their homes into office space complete with all the features and amenities of their offices at work. Shipments of plastic shelves and cabinets were valued at $270 million in 2003, largely on the strength of this trend. Most of these products were shipped in pieces ready to assemble. Despite a weak U.S. economy, which forced manufacturers to keep shelving prices low, sales of plastic shelves and cabinets grew an estimated 3 to 5 percent per year in the early 2000s. The rapidly growing ready-to-assemble sector also constituted an important market in which miscellaneous household furniture manufacturers competed for position.

Industry Leaders

The major players in this industry generally are diversified furniture manufacturers who generate the bulk of their revenue from furniture not classified under this category. Through the turn of the twenty-first century, Krause's Furniture, Inc. was a leading manufacturer of made-to-order furniture, with sales of $145 million and 1,100 employees. However, after two years of declining sales and mounting losses, due in large part to the sluggish U.S. economy, Krause filed for Chapter 11 bankruptcy protection. Unable to recover, the firm began liquidating operations in 2002.

O'Sullivan Industries, specializing in ready-to-assemble furniture, including plastic and fiberglass shelves, cabinets, and seating, employed 1,750 people in 2003, with $289 million in revenue. Another leader, Sealy Corporation, posted $1.18 billion in revenue and maintained a payroll of 6,562 employees in 2003.

Further Reading

Howell, Debbie. "Storage Shelving Cleans House." DSN Retailing Today, 27 January 2003.

U.S. Census Bureau. "Statistics for Industry Groups and Industries: 2000." February 2002. Available from http://www.census.gov/prod/2002pubs/m00as-1.pdf .

——. "Value of Shipment for Product Classes: 2001 and Earlier Years." December 2002. Available from http://www.census.gov/prod/2003pubs/m01as-2.pdf .

Comment about this article, ask questions, or add new information about this topic: