SIC 1389

OIL AND GAS FIELD SERVICES, NOT ELSEWHERE CLASSIFIED

This industry includes establishments primarily engaged in performing oil and gas field services, not elsewhere classified, for others on a contract or fee basis. Services included are excavating slush pits and cellars; grading and building of foundations at well locations; well surveying; running, cutting, and pulling casings, tubes, and rods; cementing wells; shooting wells, perforating well casings; chemically treating wells; and cleaning out, bailing and swabbing wells.

Establishments that have complete responsibility for operating oil and gas wells for others on a contract or fee basis are classified according to the product extracted rather than as oil and gas field services. Establishments primarily engaged in hauling oil and gas field supplies and equipment are classified in a range of Transportation and Public Utilities Standard Industrial Classifications. Establishments primarily engaged in oil and gas machine shop work are classified in SIC 3599: Industrial and Commercial Machinery and Equipment, Not Elsewhere Classified.

NAICS Code(s)

213112 (Support Activities for Oil and Gas Field Exploration)

Industry Snapshot

Companies categorized in this industry provide specialized services to assist in the excavation of oil and gas. These companies are used by drilling contractors to provide services in producing new wells and maintaining existing wells. The economic condition of oil field service companies is predicated on that of the oil and gas industry in general. Service-related work has been contingent on the number of rigs in operation, the price of oil and gas, and the demand for energy.

At the end of 2003, the number of rotary rigs drilling for oil and natural gas totaled 1,111, of which 109 were offshore and 1,002 were onshore. While this reflected an increase from the average annual active rig count of 830 in 2002, it remained below the 1,156 average active rig count in 2001.

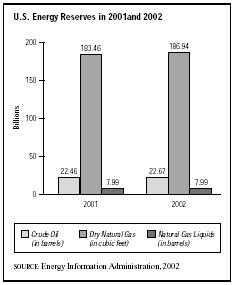

Crude oil prices in 2002 averaged $22.51 per barrel, an increase from $21.84 in 2001. Natural gas prices declined between 2001 and 2002, falling from $4.07 per thousand cubic feet to $2.95 per thousand cubic feet.

Domestic demand for energy continued to grow in the early 2000s as the United States used 97.35 quadrillion Btu of energy, compared to 96.32 quadrillion Btu in 2001. Petroleum and natural gas accounted for 63 percent of U.S. consumption, with crude oil and natural gas liquids accounting for 39 percent and natural gas accounting for 24 percent. To meet demand, the United States relied on imports for 61 percent of its crude oil supply and 19 percent of its gas supply.

Organization and Structure

Companies classified in this industry provide services intended to increase or improve well production. Services are provided throughout the life of the well, including the initial drilling, the completion phase that sets production, and the maintenance or stimulation of existing wells.

Casing and Cementing. Casing and cementing services are provided when the well is drilled. Casing is a large steel pipe, inserted into the wellhole and cemented into place. Oil well cementing is a mixture of water and cement that is pumped into the space between the casing and the wellbore, known as the annular space. The cement bonds the casing to the formation, providing structural support and directing fluid movement. Cementing also limits pipe corrosion, prevents natural gas blowouts, and aids in maximizing production circulation.

Testing Services. After the well has been drilled to its determined depth, evaluations are made to determine if the hole will produce a sufficient amount of oil and gas. Downhole formations can be analyzed by five different methods: well logging, drill stem testing, potential testing, bottomhole pressure testing, and productivity testing.

Completion Services. If it is determined that the well should be completed, the service company will lay production casing and complete the well, bringing the flow of liquid to the surface. Specific types of completion services depend upon the formation of the hole. The open-hole and liner methods are available, although the perforated casing technique has become the most commonly used completion method.

Using perforated casing, the casing wall is pierced to provide holes through which formation fluids may enter the wellbore. These holes are created either by bullet or jet perforating. Bullet perforators are lowered into the hole and fired electronically from the surface. However, jet perforating, using shape-charge explosives, has become more widely used because it produces maximum penetration, especially in hard rock.

Well Stimulation Services. Additional treatment to increase fluid flow rates may be needed to make existing and producing wells commercially viable. These treatments include hydraulic fracturing, acidizing the reservoir, and explosives. The rock type and the existing formation structure determine the selected approach.

Hydraulic fracturing is the use of specialized fracturing fluids blended with water to form a gel that is pumped downhole. This gel forces the petroleum reservoir to split open along the bedding surfaces and fracture zones extending beyond the wellbore. A greater reservoir drainage area is exposed to the wellbore, enhancing the flow of liquid. Reservoir rocks with poor permeability can be treated with acids in order to increase the wellbore's drainage area. Depending upon the structure of the reservoir, acidizing and hydraulic fracturing can be used together.

Originally used in the 1880s, explosives have reappeared as a modern well service method. Explosives are used with certain kinds of tight formations that do not respond to the other treatments. Explosive fracturing enlarges the wellbore by detonation either in the borehole or away from the wellbore.

Establishments engaged in this industry also often provide routine maintenance work on wells already in production. One of the most common well servicing operations is the artificial lift installation. When a well is first drilled, the fluid is expected to flow to the surface. In order to maintain maximum recovery from the well, however, most need some form of artificial lift to help raise the fluid to the surface. Types of artificial lifts include gas lifts, sucker rod pumps, hydraulic pumps, and submersible pumps. Maintenance service also includes replacing parts, repairing tubing leaks, working on malfunctioning downhole equipment, and providing well clean-out services.

Background and Development

When the price of natural gas fell in the United States during the early 1990s, operators reduced most of their drilling plans, which adversely affected the oil field service companies already suffering due to the decline in the over-all U.S. market. Many service companies began to diversify into other oil field services not directly related to production or well completion. Halliburton Company, a leader in the oil field services industry, purchased both 60 percent of Texas Instruments' Geophysical Services (GSI) and Geosource, another geophysical service company. The company also bought Gearhart Industries, a wireline service company, and merged it with Welex to form Halliburton Logging Services. In the second quarter of 1996, Halli-burton announced plans to acquire Landmark Graphics Corporations, the leading supplier of integrated exploration and production information systems and professional consulting services for the petroleum industry. Schlumberger Ltd., another industry leader, had also been investing in artificial intelligence technology. The company bought GECO to provide marine seismic analysis and acquired Prakla Seismos for onshore seismic operations. Schlumberger also entered a joint venture in a smart card and pay phone plant in China. At the end of January 1997, barely two months after beginning production, its factory in Hunan shipped its one millionth smart card. Pay phone production also reached volume status with an output of 1,000 units per month. Schlumberger Electronic Transactions, a unit of Schlumberger Ltd., supplied cards, terminals, and management systems across the entire range of magnetic and chip card applications and was considered the industry's leading single source supplier.

With nearly all of the world's major energy fields already found, according to The Value Line Investment Survey in 1993, the future of oil and gas excavation would be dependent on the search for smaller pools. This effort, in addition to the extension of production from existing wells, increased the demand for oil field service companies. Therefore, those companies providing high tech services, such as three-dimensional seismography, extensive data gathering methods, seismic exploration services, and enhanced oil recovery skills found a competitive but productive market in the 1990s.

Current Conditions

Rig Count. In the early 1980s, the number of operating rigs in the United States rose to more than 4,500. By 2001, this had decreased to 1,156, and the number fell further in 2002 to 830. While this number rebounded in 2003, it remained well below that of the early 1980s. In 2003, 15 percent of rigs were drilling oil, while 85 percent were drilling for gas. Per exploratory well, the average volume of oil discoveries in 2002 declined 47 percent, and the average volume of gas discoveries increased 16 percent. According to the Energy Information Administration, crude oil production in 2002 declined 2 percent to 1.87 billion barrels. This trend is expected to continue declining, as levels in the early 2000s were 12 percent lower than average levels in the 1990s. Although the natural gas industry had been growing in the late 1990s, by the early 2000s production began to decline. Dry natural gas production declined 2 percent between 2001 and 2002, while production of natural gas liquids declined 1 percent during that time period.

Price for Oil and Gas. Natural gas prices fell to $2.95 per thousand cubic feet in 2002, compared to $4.07 per thousand cubic feet in 2001. After starting at $2.36 per thousand cubic feet in January of 2002, gas prices fluctuated for most of the year until October, when they began climbing consistently. By December of 2002, gas prices had reached $3.81 per thousand cubic feet.

The well head price for crude oil has fluctuated dramatically in the early 2000s due to unstable economic and political conditions in both the United States and the Middle East. Compared to a high of $23.02 in the fourth quarter of 1996, crude oil prices were down to $15.54 per barrel in December of 2001. The average price per barrel of $21.84 in 2001 rose slightly in 2002 to $22.51. Gasoline prices, as well, continued to fluctuate in the 2000s.

Demand for Oil and Gas. Faster economic growth in the United States boosted the demand for energy, including oil and natural gas. Energy consumption in 2002 grew by 1.03 quadrillion Btu to 97.35 quadrillion Btu. The United States remains the leading consumer of energy in the world. Daily oil consumption reached 19.8 million barrels, and daily dry gas consumption reached 62.7 billion cubic feet in the early 2000s.

Consumption of natural gas had increased throughout the 1990s, gaining 3.8 percent over 1992's rate to capture approximately 25 percent of the U.S. energy market in 1993. However, by 2002, natural gas accounted for only 24 percent of the U.S. energy market. Crude oil and natural gas liquids made up 39 percent of the market.

In addition to the domestic market, service companies based in the United States will likely encounter a variety of overseas market opportunities, particularly as the United States continues to rely heavily on energy imports. High-potential countries include those in the Commonwealth of Independent States (CIS) and the Asia-Pacific region.

Industry Leaders

Halliburton Co. Dallas-based Halliburton Company provides oil field services, construction services, and insurance as an underwriter of property and casualty insurance. Its oil field service and products group provides start-to-finish service in the drilling and production of oil and gas wells. One of the many companies within this group is Halliburton Services, the world's largest supplier of cementing, stimulation, water and sand-control services and related downhole tools.

Erle Halliburton founded his company in 1919, then called the Better Method Oil Well Cementing Company. He provided a service using cement to hold a steel pipe in a well, which assisted in the drilling and production process. Although this technique was not initially accepted, it has become a common practice throughout the industry. In 1921 Erle Halliburton moved to Duncan, Oklahoma, and in 1924 he incorporated the company as Halliburton Oil Well Cementing Company.

With the purchase of other companies experienced in the oil and gas markets, Halliburton built up its oilfield service business from the 1950s to 1970s. Two particularly important acquisitions were the addition of Welex, a well-logging company, in 1957, and Brown & Root, experts in the construction of offshore and drilling platforms, in 1966.

Halliburton has operations in 100 countries providing construction, drilling, and well maintenance services. It reported 2003 sales of $16.2 billion and 83,000 employees.

Schlumberger Ltd. New York-based Schlumberger Ltd. provides oilfield services, exploration services, well site and contract drilling, and computer-aided engineering services in more than 100 countries. In January 1993, Schlumberger purchased Dow Chemical's 50-percent interest in the Dowell Schlumberger group of companies. This group provides various oil and gas field services and is divided into the following entities: coil tubing, drilling fluids services, cementing, design and evaluation, and industrial cleaning.

Schlumberger was created by two brothers, Conrad and Marcel Schlumberger, who believed that the earth's surface could be measured by electrical resistance. The company began in 1927, when the Schlumberger brothers lowered an instrument down a well to assess the surrounding rock formation.

The company's oilfield services unit provides 75 percent of total revenues. Schlumberger reported 2002 sales of $13.4 billion and 78,500 employees.

America and the World

Companies from the United States have played roles in the discovery and production of oil in major fields in Mexico, Venezuela, Saudi Arabia, Kuwait, and Libya. While exploration and oil drilling have decreased in the continental United States and Alaska, all of the major American oil companies have increased their presence overseas. The American oil and gas industry is inextricably linked to the world industry. Overseas operations have been particularly interested in service companies because of their ability to provide well workover and stimulation services to existing wells. Many countries have numerous wells in existence, but due to a lack of technology, have not been able to maximize production. The DOE has stated that the worldwide market for oil and gas exploration services was $38.2 billion in 1990 and will grow to $1.3 trillion per year to 2010. Moreover, the DOE has calculated that American vendors can capture $995 billion, or 74 percent of that market. This will likely translate into substantial opportunities for companies providing support services to oil and gas exploration services.

The CIS holds an estimated 6 percent of the world's proven oil reserves and 37 percent of the natural gas reserves. According to Oil & Gas Journal, the older fields should offer tremendous opportunities for Western service firms to achieve considerable production improvements through the use of relatively straightforward procedures such as well workovers, equipment repairs, and regular preventive maintenance programs. Estimates of the number of wells in need of workover have been as high as 20,000. Area instability since the early 1990s has slowed progress somewhat, both in renovating old wells and in new drilling and pipelines. But it is predicted that the region will experience enormous growth in the long term, and that by 2010 the CIS will be the largest supplier of natural gas. The Yamal pipeline project, if successful, will run 4,000 km connecting Siberia with Western Europe. It's scheduled completion is 2010.

The Department of Energy (DOE) also regards China as an enormous growth market for oilfield service companies. Other areas of Asia show great potential as well for the service companies. Spending by American oil companies was highest in Southeast Asia during the 1990s, indicating a vested interest in the region. Vietnam and the Philippines also show great promise for oil exploration offshore, which in turn will be a profitable opportunity for service companies.

Latin America and Africa also are growing markets. The natural gas resources in South America are largely underdeveloped but the industry is expected to undergo increased development, incurring a need for skilled personnel to build and maintain rigs and pipelines. The oil wells of Columbia and Peru are expected to double their production by the end of the century. Several natural gas pipeline projects are also planned in South America, the two most ambitious being the Bolivia-Brazil pipeline and the Argentina-Chile pipeline. In the early 2000s, the African nations of Chad, the Ivory Coast, and Somalia, among others, were expected to join the market as oil producers.

Further Reading

"Industry Statistics." Washington, DC: Independent Petroleum Association of America, 2004. Available from http://www.ipaa.org/industrystats.asp .

U.S. Department of Energy. Energy Information Administration. U.S. Crude Oil, Natural Gas, and Natural Gas Liquid Reserves 2002 Annual Report. Washington, DC: 2002. Available from http://www.eia.doe.gov .

Comment about this article, ask questions, or add new information about this topic: