SIC 3339

PRIMARY SMELTING AND REFINING OF NONFERROUS METALS, EXCEPT COPPER AND

ALUMINUM

This classification covers establishments primarily engaged in smelting and refining nonferrous metals, except copper and aluminum. Establishments primarily engaged in rolling, drawing, and extruding these nonferrous primary metals are classified in SIC 3356: Rolling, Drawing, and Extruding of Nonferrous Metals, Except Copper and Aluminum, and the production of bullion at the site of the mine is classified in various mining classifications.

NAICS Code(s)

331419 (Primary Smelting and Refining of Nonferrous Metals (except Copper and Aluminum))

Industry Snapshot

This industry supplies nonferrous metals for further consumption to secondary smelting and refining establishments. The metals refined include antimony, babbitt, beryllium, bismuth, cadmium, chromium, cobalt, columbium, germanium, gold, iridium, lead, magnesium, nickel, platinum, rhenium, selenium, silicon, silver, tantalum, tellurium, tin, titanium, zinc, and zirconium. These metals are extracted from their ores and poured into basic shapes, such as slabs, pig molds, or ingots.

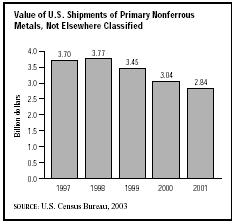

According to the U.S. Census Bureau, roughly 140 establishments operate in this category. Industry-wide employment totaled 9,197 workers receiving a payroll of more than $400 million in 2000. Within this workforce, 6,235 of these employees worked in production, putting in more than 13 million hours to earn wages of almost $225 million. Overall shipments for the industry were

valued at more than $2.8 billion in 2001, down from $3.7 billion in 1997.

Background and Development

In its March 1999 issue, E-MJ—Engineering and Mining Journal reported on the market status of many of the metals in this industry, including cobalt, lead, nickel and zinc. Lead experienced increased consumption due to steady demand for lead acid batteries. The lead market had been depressed in the early 1990s, recovering in the mid-1990s. Lead prices on the London Metal Exchange (LME) averaged 28 cents per pound in 1995 and 1997, peaking in 1996 to 35 cents per pound; the price continued to fall to 24 cents per pound in 1998. Seventy percent of domestic lead production, however, occurred at secondary smelters, which primarily recycled lead acid batteries; this left only 30 percent of production for primary smelters.

Cobalt prices plummeted in 1998 due to weak endmarkets and inventory stockpiling. Producers had been hoping for price reductions to spur consumption, but the price fell further than expected while consumption failed to increase, creating an imbalance. The future of the cobalt market promised continued consolidation to weather its fluctuations. Similarly, nickel prices plunged 33 percent in 1998, averaging $2.13 per pound across the year. Western consumption grew slightly, while Western production grew 2.3 percent to 713,000 metric tons. These conditions combined to create a volatile market for nickel, with recovery at the mercy of global economic growth. Zinc experienced similar market conditions, with prices on the LME falling from 48.7 cents per pound at the opening of 1998 to 41.6 cents per pound at the year's close, averaging 46.5 cents per pound—a significant decrease from 1997's average of 59.8 cents per pound. Western consumption similarly declined.

Current Conditions

Shipments of primary nonferrous metals, not elsewhere classified, had declined steadily throughout the late 1990s and early 2000s. Between 2000 and 2001 total industry shipments declined from $2.77 billion to $2.2 billion. Shipments in 2001 were less than half the value of industry shipments in 1997. Refined primary zinc, which accounted for 17.2 percent of industry shipments in 2001, saw the value of goods shipped decline from $542.9 million in 2000 to $490.3 million in 2001. The value of goods shipped for the primary precious metals and precious metal alloys sector, which made up 18.8 percent of industry shipments in 2001, dropped from $549.2 million to $537.1 million over the same time period.

Industry Leaders

Dominating the industry in overall sales were Phoenix, Arizona-based Asarco Inc., with more than $514 million in 2003 sales; New York City-based Renco Group Inc., with $2.1 billion in 2003 sales; St. Louis, Missouri-based Doe Run Co.; and New York City-based Horsehead Industries Inc.

Research and Technology

Late in October 1993, researchers at the National Institute of Standards and Technology (NIST) in Boulder, Colorado announced they had developed a new alloy. The alloy is a combination of nickel, chromium, manganese, molybdenum, copper, nitrogen, and iron. It can withstand temperatures below −269 degrees Celsius (−516 degrees Fahrenheit), and is expected to find use in fusion energy studies, superconducting magnets, and physics experiments funded by the U.S. government. The importance of the alloy will lie in welding seams in superconducting magnets, which must resist fracture in such low temperatures. In 2000, the NIST developed another new alloy—a combination of tin, silver, and copper—designed to offer a non-lead based alternative for the manufacture of electronic equipment.

Further Reading

Deelo, Michael L. "Lead: Millennium to Bring Happiness?" E-MJ—Engineering and Mining Journal, March 1999.

Kielty, Edward R. "Cobalt: A Market Still Not Satisfied," E-MJ—Engineering and Mining Journal, March 1999.

"National Institute of Standards and Technology." Purchasing, 19 October 2000.

Upton, Doug. "Nickel." E-MJ—Engineering and Mining Journal, March 1999.

U.S. Census Bureau. "Statistics for Industry Groups and Industries: 2000." February 2002. Available from http://www.census.gov/prod/2002pubs/m00as-1.pdf .

——. "Value of Shipments for Product Classes: 2001 and Earlier Years." December 2002. Available from http://www.census.gov/prod/2003pubs/m01as-2.pdf .

Comment about this article, ask questions, or add new information about this topic: