Healthcare Software Company

BUSINESS PLAN QUIKMEDINFO

689 Wyoming Avenue

Louisville, Kentucky 40202

QuikMedInfo has developed a targeted, well-thought-out marketing plan providing a clear road map of how it will secure clients and allied business partners for its innovative, highly useful healthcare software targeting hospitals. This plan was provided by Trinity Capital.

- EXECUTIVE SUMMARY

- COMPANY SUMMARY

- PRODUCTS

- MARKET ANALYSIS SUMMARY

- STRATEGY

- IMPLEMENTATION SUMMARY

- MANAGEMENT SUMMARY

- FINANCIAL PLAN

EXECUTIVE SUMMARY

The QuikMedInfo product is an application that allows numerous databases to completely interface with each other without changing hardware or software between parties. The product can work over a secured Virtual Private Network (VPN) and be encrypted at 128 bits. The product developers have concentrated on the medical community as end users—specifically, hospitals. The next logical market would be the health insurance industry.

QuikMedInfo is an innovative new solution in the healthcare industry, bringing a common client presentation to users of disparate systems. Multiple hospital information systems can now be accessed, within or outside of the immediate hospital environment, with a Java-based "common client presentation." QuikMedInfo provides a graphical front end for the user with any of the popular Internet Web browsers, such has Netscape and Microsoft Explorer.

The product is currently developed in seven different modules. As an Intranet application solution, the modules are required to run on a robust server. The installed modules are Admissions, Transcriptions, Laboratory, Imaging, and Pharmacy. Future modules are in development as needed in the marketplace. Home Health and Physician management modules are complete but not installed. Currently five modules are successfully operating in six different environments.

All these modules allow credentialed QuikMedInfo users to access all of the applications via the Internet or through the VPN Intranet. The Admissions application allows users to share data between healthcare organizations, displays information about the patient, and handles patient transactions—including pre-admissions, registration, and admissions. The Transcriptions section creates new transcriptions; doctors now can sign transcriptions electronically, list patient and physician transcriptions, view transcription details, and format all the views. The Laboratory application entails ordering lab tests, viewing results and comments, sorts test criteria, and other laboratory functions. The Imaging module digitizes images such as licensees, photos for I.D. purposes, EKGs, CAT scans, MRIs, and pulmonary functions tests. The Pharmacy module lists medications prescribed for any given patient, views medication details, references patient allergies, and can be linked to all area pharmacies in addition to the hospital pharmacy.

The product will be leased, rented, and sold to potential users. Leasing and renting the product will facilitate faster sales in the hospital environment. Because the full price of the product can reach $350,000, many hospitals must postpone decisions until another budget year. Leasing and/or renting will allow the hospital to make decisions sooner. Also, approaching physicians first in order to sell the hospital on the needs of the physicians will allow for easier access to information.

The hospital industry relies on a multitude of different systems to house the databases they access. These systems are provided by different vendors and do not share data. When physicians and hospital staff need to access data they are required to sign in and out of these multiple databases to complete a transaction. This is very inefficient, and a significant issue for hospitals that find themselves in an environment of decreasing reimbursement from government programs and managed care companies.

The developer of the QuikMedInfo application solution is Best Source Solutions, Inc. QuikMedInfo is a new entity being formed to market the QuikMedInfo product.

Best Midwest Solutions, Inc. (BMS), a value-added reseller of computer hardware and software, worked with a community hospital to find a solution to their problem with the inefficiency of dealing with disparate systems. The result of almost three years of effort and $2.2 million of investment is this software program. It provides a web-enabled interface capable of linking all of a hospital's disparate systems to a single, common view which is extremely simple and easy to use. While the development of the product has been focused on the healthcare industry, the technology is applicable to any industry that uses many different systems.

BMS has sold and installed six units at customer sites. (All of them are very happy customers willing to serve as references.) Four of the installations are healthcare related, and one is in the communications industry. Over the past year the BMS sales staff has spent its time educating the hospital industry about the product and waiting for the hospitals to obtain approval for the capital expenditure. As a result of these efforts, BMS currently has a list of 13 qualified clients representing potential revenue in excess of $3 million. Management estimates the probability of closing these sales at between 30% and 90%.

BMS lacks sufficient capital to effectively penetrate the hospital market nationally. In addition, a more complete and robust management team will fully enable the execution of the plan.

QuikMedInfo is seeking $3 to $6 million in investment. $3 million would be utilized under the guidelines of this plan to expand market share via marketing and in working capital to expand personnel and operational needs.

Successful penetration of the hospital market in years one, two, and three will enable the company to become profitable. Projected profitability occurs at 24 months. Cash flow from the initial investment should be sufficient to execute the plan through the first three years. Any shortfalls should be correctable by commercial banking options. Years four and five call for full national roll out and entry into other vertical markets, primarily health insurance. Management forecasts a $40 million company by year five. A bank line of $1.5 million and a mezzanine debt/equity infusion of $5 million (in year four) will finance the growth and potentially lead to an acquisition or an IPO.

As is characteristic of the software industry, margins are high and cash flow and accumulation are excellent.

Fiscal year 2000 begins in September 1999.

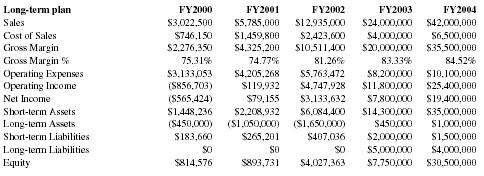

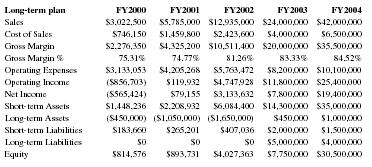

The following illustrates a summary of our financial projections:

| Long-term plan | FY2000 | FY2001 | FY2002 | FY2003 | FY2004 |

| Sales | $3,022,500 | $5,785,000 | $12,935,000 | $24,000,000 | $42,000,000 |

| Cost of Sales | $746,150 | $1,459,800 | $2,423,600 | $4,000,000 | $6,500,000 |

| Gross Margin | $2,276,350 | $4,325,200 | $10,511,400 | $20,000,000 | $35,500,000 |

| Gross Margin % | 75.31% | 74.77% | 81.26% | 83.33% | 84.52% |

| Operating Expenses | $3,133,053 | $4,205,268 | $5,763,472 | $8,200,000 | $10,100,000 |

| Operating Income | ($856,703) | $119,932 | $4,747,928 | $11,800,000 | $25,400,000 |

| Net Income | ($565,424) | $79,155 | $3,133,632 | $7,800,000 | $19,400,000 |

| Short-term Assets | $1,448,236 | $2,208,932 | $6,084,400 | $14,300,000 | $35,000,000 |

| Long-term Assets | ($450,000) | ($1,050,000) | ($1,650,000) | $450,000 | $1,000,000 |

| Short-term Liabilities | $183,660 | $265,201 | $407,036 | $2,000,000 | $1,500,000 |

| Long-term Liabilities | $0 | $0 | $0 | $5,000,000 | $4,000,000 |

| Equity | $814,576 | $893,731 | $4,027,363 | $7,750,000 | $30,500,000 |

Objectives

- The business goal is to obtain a 20% market share of the target hospital market in the United States within five years.

- We will offer our software to healthcare-related industries including hospitals, third party administrators, insurance companies, etc.

- We will sell our software, its services and professional consulting directly to accounts and through qualified resellers. We have OEM contracts available that already present an opportunity.

- We plan to be profitable in 24 months and have the opportunity to sell the business at a 15x or higher multiple to another company or make an initial public offering.

Mission

Our mission is to provide physicians and hospital staff access to critical and multiple sources of data, thereby improving their efficiency in caring for patients. In turn, this will improve patient care, increase patient satisfaction, and save time and operating costs.

Keys to Success

The keys to our success are:

- Bringing multiple information sources to a single, common view that is extremely simple and easy to use.

- Providing a low entry price model by offering the product as a monthly service, as well as a purchase price. The low monthly price eliminates capital budgeting issues and allows quicker decisions by hospital management.

- Interfacing to the various legacy systems through several industry standard protocols. Having legacy vendor access is important but can be overwritten by other tools.

- Obtaining physicians' sponsorship.

- Extending our technology to payors, third-party administrators, etc. who often can make decisions quicker than providers.

- Obtaining required capitalization and key management.

- Managing our channels of distribution and resellers effectively.

COMPANY SUMMARY

QuikMedInfo will acquire the rights to the QuikMedInfo code from Empire System, Inc. (Empire), a value-added reseller of hardware and software products. Empire was started in 1990 and has current revenues of $32 million. Empire is located in Lexington, Kentucky. Empire began the development of this software product because of the need by hospitals and physicians to have easier access to data from disparate systems. Empire has invested $2.2 million and 2 years in the development of the product, QuikMedInfo. QuikMedInfo will provide Intranet/Internet applications to the healthcare industry to enhance access to the industry's disparate legacy systems. This access to critical data is vitally important to patient care and satisfaction as well as to physician and staff productivity.

Company Ownership

QuikMedInfo is located in Louisville, Kentucky. It is owned currently 50% by Rachel Brown and 50% by Ed Roost.

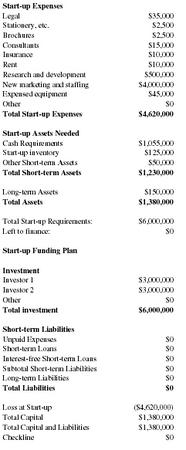

The following summarizes the start-up requirements. Primary requirements are working capital. $3 million is being sought for the purposes of this plan.

Start-up Summary

| Start-up Expenses | ||

| Legal | $35,000 | |

| Stationery, etc. | $2,500 | |

| Brochures | $2,500 | |

| Consultants | $15,000 | |

| Insurance | $10,000 | |

| Rent | $10,000 | |

| Research and development | $500,000 | |

| New marketing and staffing | $4,000,000 | |

| Expensed equipment | $45,000 | |

| Other | $0 | |

| Total Start-up Expenses | $4,620,000 | |

| Start-up Assets Needed | ||

| Cash Requirements | $1,055,000 | |

| Start-up inventory | $125,000 | |

| Other Short-term Assets | $50,000 | |

| Total Short-term Assets | $1,230,000 | |

| Long-term Assets | $150,000 | |

| Total Assets | $1,380,000 | |

| Total Start-up Requirements: | $6,000,000 | |

| Left to finance: | $0 | |

| Start-up Funding Plan | ||

| Investment | ||

| Investor 1 | $3,000,000 | |

| Investor 2 | $3,000,000 | |

| Other | $0 | |

| Total investment | $6,000,000 | |

| Short-term Liabilities | ||

| Unpaid Expenses | $0 | |

| Short-term Loans | $0 | |

| Interest-free Short-term Loans | $0 | |

| Subtotal Short-term Liabilities | $0 | |

| Long-term Liabilities | $0 | |

| Total Liabilities | $0 | |

| Loss at Start-up | ($4,620,000) | |

| Total Capital | $1,380,000 | |

| Total Capital and Liabilities | $1,380,000 | |

| Checkline | $0 | |

Company Locations and Facilities

It is expected that QuikMedInfo will be located in Louisville, Kentucky. However, Lexington also may be a future potential headquarters.

PRODUCTS

QuikMedInfo will sell software and installation services related to that software. The company also will sell professional consulting services that include the design, writing, and implementing of custom screens, file interfaces, and administrative security features related to the software product. The software runs on a variety of computer servers. The software is written in 100% Java, which is supported on many hardware servers and is scaleable from the smallest of servers to the largest of systems.

Product Description

QuikMedInfo sells software for hospitals, physicians, payors, and related entities.

Software is sold with a base server license, seats, and applicable modules.

The software will interface across all disparate hardware and software systems, using the Internet language of Java (licensed by Sun Micro Systems, Inc.). No additional purchase of hardware is required to run the software.

Professional services are provided for customization of the software.

Training and support services are provided as a billable item.

The product is currently developed in seven different modules. As an Intranet application solution, the modules are required to run on a robust server. The installed modules are Admissions, Transcriptions, Laboratory, Imaging, and Pharmacy. Future modules are in development as needed in the market place. Home Health and Physician management modules are complete but not installed. Currently five modules are successfully operating in six different environments.

The QuikMedInfo System

- A single system that will do the data collection, presentation, and transmission without regard to the platform, software, or location of either the original data or end user.

- A system that is sensitive to political, security, and financial aspects.

- A system that recognizes the importance and responsibility of the M.D.

- A system that merges the unique talents of the team.

- A system that recognizes the annual purchase cycles of hospitals and offers a "subscription" or rental option.

- A system that derives from and is validated by the market research we have done with M.D.s and hospitals.

Competitive Comparison

The QuikMedInfo software system has been in the disparate system market for nearly three years. Originally there was very limited competition. We fully expect the competition to increase as Java becomes better known and last year's Y2K issues free up budgets in hospitals, thereby making the sale of the product easier. Presently, our competitors include interface engine companies that are developing web front-end applications, internal application development from a hospital's own staff, and hospital information systems companies who are web enabling their own applications.

However, we have several major advantages that will enhance our chance of success. These are:

- Hospital information vendors are focused on web enabling their applications, not the common access of their applications to other competitive vendors. This is our niche.

- Hospital information vendors generally do not respond to customers' needs for specialization of their applications.

- Hospitals generally follow one another, which is why we have priced aggressively to get a customer base established.

- Our design allows for a very quick deployment.

- Our application is very easy to learn.

- Our application ties many systems together, thereby being more difficult to uninstall later.

Competitors we are aware of include:

- ABC, an investment by Denver Technology Partners. This company has focused on single sign-on applications and has one or two installations.

- Delve, originally an interface engine company, developed a web interface product. This company was purchased by Oneida Systems. Oneida recently went public and had a very successful offering. Another large interface engine company, Mongoose, is developing a web front end.

- Med-Shell, another company that recently went public, provides similar services that we provide to payors. Med-Shell has purchased several companies and is developing its market. It has recently entered into a marketing relationship with IBM.

- JKL provides a repository to view clinical data over the web. We approached this company two years ago as a business partner, but they felt their development was too far along to assist us. JKL has one or two installations and has had those same installations for nearly two years.

- Inter Fuse M.D., a consortium of many content vendors, is entering the market promising to be a catch-all solution to physicians and providers.

Note: Inter Fuse M.D. and a company named DEF have recently merged. This has created a powerful economic entity. However, our management believes that the scope of their focus is much too broad to mount a challenge in our specific niche. We expect to be able to deliver a better product.

Other competitors may be terminal emulations over the web. We do not see these as direct competition. The key to our market success is being able to provide access to the most important 20% of the critical clinical information to 80% of the users in the hospital market. Often times the data exists but it is neither available nor accessible. We offer a solution to bring this data together in a secure auditable manner for these users.

Sales Literature

Most of our marketing literature has been developed. Our collateral materials include:

- A physician-oriented brochure.

- A hospital-oriented brochure.

- An online web site providing information on the product, architecture, white papers, and online demonstrations.

- A brochure aimed at the insurance and third-party administrator market will be developed.

- General tradeshow booths have been purchased in two sizes. These sizes include a 10' × 10' portable booth and a 10' × 20' demonstration booth. The 10' × 20' booth was designed exclusively for trade shows.

Sourcing

QuikMedInfo will own the sole rights to the software product. This software is copyrighted. The copyright will have to be updated from time to time to protect our investments in the code.

Technology

The QuikMedInfo software is a 100% Java-compliant application. Java is the single best software designed to write applications for the World Wide Web. It is an object-oriented programming language which allows for extremely fast application development and customization. One of the advantages of Java is its wide support from a variety of hardware manufacturers. Although, other programming languages may appear, such as Microsoft's XML, we have been consistently satisfied with Java's performance. Another reason for choosing Java was the flexibility it provides by running on many hardware vendors' platforms. This provides our customers with the security of scaleable systems. Microsoft's XML only runs on an NT server and thus is limited to the PC marketplace. Java runs on personal computers, midrange systems, and mainframes.

Future Products

Our future includes taking the existing software to complimentary industries, such as payors. The software can be used by any industry desiring to link disparate systems; e.g., the telecommunication industry desiring to link pager, mobile telephone, e-mail and other systems. Also, as installations continue, we will build a library of interfaces that make installations and connectivity easier. New applications are to be added annually to include more connectivity to disparate applications. We expect to sell these new and additional modules for $25,000 to $50,000 each.

The focus of our plan is to develop the medical and hospital application first, then penetrate the health insurance vertical market. These other applications above have the potential to generate many times the revenue projected in the focus of this plan. That may be a strategic reason for an IPO.

MARKET ANALYSIS SUMMARY

As any new product is brought to the marketplace it will gain the attention first of the early adopters, then the primary market, and then the market laggers. Our primary target market consists of community-based hospitals with 200 or more beds. When we tried marketing to large chain hospitals such as Ft. Benson and Diamond, we discovered these organizations are extremely interested in the product but bogged down by their own bureaucracies. The same is true for large HIS application vendors. Therefore, we will stay focused on the smaller and independent hospitals that can make a quicker decision.

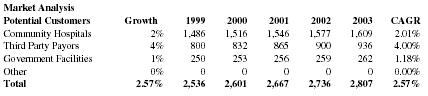

Presently, there are about 5,057 hospitals in the United States. Our target market is the "200 bed and larger" facilities, of which there are 1,486. The total target market potential represents $371,500,000. Of the 1,486 facilities, we plan to sell to 300 facilities over the first five years, which represents 20% of our target market. With an average complete sale of $250,000 this would represent $75,000,000 in revenue over five years.

It is estimated that fewer than 10% of these sales will be for cash. Third-party leasing is expected to comprise the majority of our business.

Revenues in our five-year plan above the $75,000,000 million total are the result of additional vertical markets initially penetrated with modest market share in years four and five.

Our experience has been that it takes about a year for a hospital to make a decision. Our marketing efforts of last year are paying off this year as we close the identified opportunities. Our objective is to keep the pipeline full and have regular closings. Many of the existing customers are already returning for additional customization. We expect our revenues to grow at a minimum of 50% to 100% for the next several years.

Market Segmentation

Our market segmentation includes three primary areas:

- Community and regional hospitals averaging about 200 to 700 beds.

- Third-party administrators and payors.

- Government-run programs, Child Health Insurance Plans (CHIPS), and VA hospitals.

Community and regional hospitals are searching for ways to improve their back office operations and to improve relationships with physicians by providing them better access to patient information.

Third-party administrators can use the software to provide remote access to authorizations, eligibility, claims status, referrals, etc. This information also can be shared with hospitals who have the software and can enable electronic pre-admissions.

Payors can use the software to offload heavily staffed call centers by allowing physicians direct access to eligibility, claim status, etc. Payors can in essence extend their operational hours by allowing direct access to data. They can use this program with employers to provide benefit plan details, account status, explanation of benefits, etc.

State agencies funded by the federal government can purchase our "out of the box" application for certain mandated programs.

Other potential markets include any industry with disparate systems that could benefit from a consolidated view of data. An example of this would be the telecommunications industry which may have systems related to their different products. By using our product, you could view on one display a customer's information coming from providers of email services, voice mail, local telephone service, long distance telephone service, paging services, cellular services, cable television, Internet services, etc.

| Market Analysis | |||||||

| Potential Customers | Growth | 1999 | 2000 | 2001 | 2002 | 2003 | CAGR |

| Community Hospitals | 2% | 1,486 | 1,516 | 1,546 | 1,577 | 1,609 | 2.01% |

| Third Party Payors | 4% | 800 | 832 | 865 | 900 | 936 | 4.00% |

| Government Facilities | 1% | 250 | 253 | 256 | 259 | 262 | 1.18% |

| Other | 0% | 0 | 0 | 0 | 0 | 0 | 0.00% |

| Total | 2.57% | 2,536 | 2,601 | 2,667 | 2,736 | 2,807 | 2.57% |

Target Market Segment Strategy

Our target market is the hospital industry where it is very common to find disparate systems. Hospitals typically take one year to eighteen months to make a decision. Providing flexible pricing and purchasing options, which might avoid the need to go through the capital budgeting process, should help shorten this cycle. Also, hospitals do not like to write their own systems and would rather use applications to achieve their needs.

Secondary markets are the insurance payors and third-party administrators that work in the healthcare field. They are interested in providing physicians with access to patient data, such as eligibility, and with the ability to electronically obtain authorizations, referrals, etc. These companies typically make a decision very quickly, and their services may inter-relate with the hospitals to whom and with whom they market.

Once these industries have been established using our product, we would broaden our base to begin to penetrate other industries where disparate systems exist.

Market Needs

The target market is seeking simplicity of its processes, increased productivity of its staff and increased patient satisfaction. Areas of concern are the physician's time to access information, access to proper data from insurance companies, scheduling lab tests, and many back office and/or administrative procedures. Our niche is to bring the needed information from several disparate systems to a single web browser.

An example of this daily frustration is as follows. A physician wants to retrieve the lab test for a patient. Depending on the lab test results, the physician may change the patient's medication and notify the patient of the change. The physician or someone on the staff would access the lab system; complete a sign-in with a password; conduct a patient search; select a medical record, a specific encounter, or visit; and retrieve the latest lab result. Upon finding the result, the physician would then sign out of the lab system and enter into the pharmacy system. The physician would use a second sign-in and a second password, conduct another patient search, locate the visit that has the medication, review, and submit a change to the pharmacist and sign out of that system. The physician would then sign on a third time, with a third password, conduct another patient search to get the appropriate patient demographics to notify them of the lab results and the change of medication. None of the above systems look, feel, or act similarly.

With our software, the physician can retrieve all the above information with one sign-on, one password, and one patient search.

From our visits in many hospitals the 80/20 rule exists: 80% of the people need about 20% of the data. Today that information is not easily available to them. Our product solves that dilemma.

How an M.D. could use the system was discussed during a physician advisory board meeting:

1. A radiologist:

- Patient info available (even at the beach via notebook computer).

- Radiologist at another hospital sees a patient that he wishes to refer.

2. A surgeon:

- Pre-hospital rounds data review.

- Image and lab review.

- Remote chart review and signing.

- Gain access to hospital pharmacy formulary (or insurance co. drug formulary).

- Order drugs that will be effective, available, and insurance reimbursable.

3. An EE&T:

- Quality assurance.

- Scheduling at surgical center.

4. An IPA (Independent Physicians Association):

- Quality assurance.

- M.D. to M.D. referrals.

How a hospital could use the system:

- Electronic chart signature which allows billing to occur much quicker.

- Windy Mountain (newly acquired hospital) can be integrated with St. Thomas Hospital.

- Any of the 100-plus hospitals in Kentucky to communicate with M.D.s.

- M.D. access to lab, X-ray, etc. without new hardware or software.

- Referral data transferred without new entry.

Market Trends

The trends in this industry include consolidation of facilities, competition for physician allegiance, and the need to improve efficiencies with the decreasing reimbursement rates from government and managed care companies. The World Wide Web is going to be the mechanism by which most information will be implemented and routed. Having a tool that acts as a manager of all those possible connections is important and gives the hospitals a great amount of freedom for their future. We feel this trend will only strengthen over the next several years.

The trend for this "connection" will be a vital role as companies race to get to the market. As we build our connections and libraries of interfaces we will become a dominant player in the marketplace.

Presently, the major hospital information vendors are trying to convince hospitals to consolidate all systems to one vendor. If the vendors were successful in creating this trend, then they could provide a web enablement to their different systems. However, there is significant resistance by the hospitals who do not want to be tied to one vendor. First, the hospital would have to discard millions of dollars already spent for information systems. Secondly, the market is dynamic and no one vendor has successfully captured all areas of a hospital sufficiently so that the hospital has no other needs. The closest vendor to achieving this may be Tech5Health which does offer a proprietary, one-source solution.

It appears that most hospitals want the option to purchase the "best of breed" systems and they will need a system to connect their disparate systems. The hospitals will see a product that allows them to maintain their current system investments, purchase new "best of breed" systems but still maintain autonomy by having a common front end. They have the freedom to change as little or as frequently as their business model requires.

The product works especially well for consolidation of hospitals as well, because the common front end can work with entirely two different hospital information systems. This can provide millions of dollars in savings.

Market Growth

This market will have a 30% or higher growth rate. There is no question that web business or "e-business" (as some companies have phrased it) will be the dominant force over the next 10 years. Recent reports by Roger Alison, industry analyst, illustrate huge paybacks for customers implementing this technology.

Industry Analysis

Common front-end systems are a rather new segment in the industry. As systems have become more complex, users are looking for simple ways to access data. We have found the Pareto rule to be true in the healthcare market: 80% of the people only need about 20% of the data. It is unfortunate that the 20% is across many systems and thus difficult to locate. A review of the industry would put us in a developing category called Universal Desktops or Single Sign-On Solutions.

The Healthcare Community

Healthcare has traditionally been a system of distinct parties who must work together and form a service community. The parties include M.D.s, M.D. office staff, hospitals, surgical centers, diagnostic centers, home health agencies, nursing homes, insurance companies, federal and state government, patients, and ancillary service providers. Patient and their information are the common thread. Each party creates unique information for and about the patient and yet has need of some identical information. The concept of using someone else's information without physical presence in the originating facility is a dim hope only. Within each party's organization there exists a microcosm of the situation existing between parties. As an example, a hospital may have data in a billing system, a dictation system, a laboratory system, an X-ray system and a pharmacy system. The means of gathering, storing, and processing information is different for each party and, despite good intentions, multiple data systems present a very steep learning curve. A busy M.D. will likely select those which they must use (dictation and office billing) and ignore the rest.

M.D.s are the mobile link in that they move between the parties and utilize the bulk of the information. By nature, patients in a hospital are unable to travel to an office. In addition there are many times an M.D. may not be near the data they need to answer an "on call" emergency situation without undue travel and effort.

A Brief Functional Overview of the Medical Community

Very high-tech treatment means:

- The entire process is information-driven combined with judgment of the M.D.

- M.D.s are time efficient and will increase efficiency subject to a learning curve resistance.

-

Gradual acceptance and implementation of information systems in:

Laboratory

Imaging (X-ray, MRI, etc.)

Pharmacy

Billing and patient records

Dictation - M.D. offices adopting information systems for billing.

- Electronic medical records in some M.D. offices.

- Gradual understanding of need to communicate without paper or people intervention.

- Everyone developing their own means to share information.

- M.D. now has to know and use the unique system for each application.

- Hospitals are looking for means to bind M.D.s to them.

- The systems in place use different software and to a lesser extent different hardware.

- All the parties in this community are mildly distrustful of the other's motives.

- HCFA will lobby for secure, automated transfer of data.

Industry Participants

Participants in this industry include the following:

- Single Sign-On Vendors. These vendors offer single sign-on solutions that vary from terminal emulation sessions over the web to more robust sign-ons that also handle password and security. Our product competes well in this environment. We offer a single sign-on to multiple systems, handle security, encrypt data, and retrieve data based upon a user's sign-on identification.

- HIS vendors web enabling their own products. We fully expect each HIS vendor to web enable their own products. These vendors are only interested in web enabling their proprietary software and the large vendors are not known for good customer service. If a customer has multiple different systems he will still have several different systems to access with each system looking and responding differently. The proprietary web enablement will not give the customer with multiple systems anymore ease of use than he presently has with multiple terminal emulations.

- Niche players. There are some direct competitors that we face in the market that offer products similar to ours. These players may address a particular need for a healthcare company such as access to payor information. Healtheon would be an example of this type of company. IBM, also, offers a repository that can be accessed via the web. Our product is more flexible and can better meet the varying needs of the customer.

Distribution Patterns

The product will be sold primarily via a direct sales force. We currently have a few distributors who are excited about the product and have specific opportunities to market the product. These distributors are given a discount that ranges from 30% to 40%, depending upon volume. We also have an OEM agreement that allows the vendor to incorporate the product into their software offerings. This agreement requires an inventory purchase and the company receives payment for each time the product is sold. Both distributors and OEM companies are required to identify the end user to our company for record purposes and quality assurance.

Sales Strategies / Channels

The company's goal is to infiltrate QuikMedInfo into the heart of the healthcare industry. The objective is for QuikMedInfo to be accepted as the standard Intranet application solution that hospitals, doctors, clinics, pharmacies, and laboratories use to obtain necessary patient data. There are three channels defined below to assist us in achieving this goal.

1. Distributors — There are five categories for distributors. These categories are:

- HIS Vendors (provide legacy-based applications to the healthcare industry).

- Interface Engine Vendors such as CAI, STC, HCI, and Hublink (provide communication interfaces between HIS vendor legacy applications to transmit data from one HIS vendor application to another).

- Healthcare industry related consulting firms (providing integration services to hospital organizations).

- Value Added Resellers (selling healthcare-related solutions to hospital organizations).

- Computer and Communication Hardware Vendors (provide computer and communication software, hardware, and services to the healthcare industry).

This group of channels, organized to create higher net revenue, will be resellers of QuikMedInfo. They will assist in marketing and selling QuikMedInfo to local hospitals, clinics, pharmacies, and laboratories that desire to take advantage of the benefits QuikMedInfo has to offer. Distributors will receive commissions based on the level of support provided for every sale they complete. The advantages of utilizing distributors is that they are already providing solutions to the primary target market and can easily penetrate these organizations to provide QuikMedInfo as their Intranet application solution of choice. The cost to support these channels is minimal for the amount of return for immediate market exposure they will provide for QuikMedInfo.

2. Independent Representatives — Independent Representatives are sales people under contract to market QuikMedInfo. They are extensions of the direct sales team, with the added advantage of reaching clients in various service areas that the direct sales team cannot or have not approached. They receive no salary and earn only from commission based on the level of support provided for every sale they complete. Like distributors, the advantages of utilizing independent representatives is that they are already providing solutions to our primary target market and can easily penetrate these organizations to provide QuikMedInfo as their intranet application solution of choice. The cost to support this channel is minimal for the amount of return for immediate market exposure they will provide for QuikMedInfo.

3. Direct Sales — Sales are done directly with hospitals, doctors, clinics, pharmacies, and laboratories utilizing company internal sales representatives. As opposed to distributor and independent representative sales, direct sales do not involve middlemen. Hospitals purchase QuikMedInfo from the direct sales team. The team identifies potential customers, contacts those customers directly, and sells the product to them firsthand. As with arrangements involving distributors and independent representatives, direct sales involve educating the industry about QuikMedInfo—therefore increasing QuikMedInfo's exposure.

Competition and Buying Patterns

The hospital market purchases software it deems as having a strong return on investment. Also, the hospitals tend to purchase applications other hospitals have been successful installing. Most sales to hospitals take time, plus involve patience and working with many different persons within the hospital. Reference selling is important. This type of solution to hospitals is very new and has been ahead of its time. Much of the selling in the past year has been educational, positioning hospitals to use the technology. The market is now developing at a much quicker pace.

Hospitals choose their vendor based upon value of the application, price and ROI, and the quality of the vendor (reputation). Image and visibility are important to gain mindshare and the perception of being a national vendor. However, nothing beats reference selling and recommendations from customers. All of our current customers have agreed to be references.

Main Competitors

Our main competition comes from interface engine companies, hospital information systems vendors, and other web providers.

Of the original four primary interface engine companies only two remain. The original four included CAI, HCI, Hublink, and STC. CAI merged with Neon Systems. Hublink was purchased by HCI and changed their name to HIE. STC remains one of the oldest and established firms in their industry segment.

CAI developed a product about the same time as this product. Their product is called Web Connect and is similar in function to this product. They are at about the same stage of development as our company. CAI was purchased by Whiteash Systems, and Whiteash recently had a very successful IPO.

HIE has maintained its focus on being an interface engine company and has moved from the health market to other industries such as finance, and manufacturing. The purpose of an interface engine is to simply take data for system A and place it on system B, C, etc. This is accomplished by hidden coding and so is transparent to a user of an application. An example of this in the healthcare market is a patient updating his phone number when picking up a prescription. The interface engine would place the changed phone number in the patient demographics system, the lab system, etc.

STC is a well-entrenched interface engine company. STC was previously embedded into the Coopers LPMN product and many sales were achieved with little effort. STC had planned an IPO but backed off when they lost the Douglas contract. Recently, STC has begun a web implementation that is to rival this product. For one year they have promised a few customers sweetheart deals to wait on their product. It is still not marketable but is still being developed. Due to their presence and install base they may be successful in getting their customers to delay decisions.

Hospital information systems companies are racing to get their solutions web enabled. The only focus these vendors have is with their own products. None of these vendors have an interest in developing a cross-vendor web solution. The comment is "Why would I web enable my competitor?" This solidifies the niche that our product addresses.

Some of these web solution providers include Core Change, Healtheon, Envoy, and IBM. CoreChange addresses a single sign-on approach to many systems, Healtheon is extending payor information such as eligibility, authorization, claim status, etc. IBM is offering a repository that can extend results to the web. Our product has the design to do all the above and more. It is robust but also can be sold as a minimized solution.

Other web providers have and will continue to appear. These vendors range from terminal emulations to web content providers. Nathan Bedford Forest, in speaking of his success as a General, stated his key to winning the battle was "the firstest with the mostest!" Yes, it is poor grammar; but his point is the first to the market wins mindshare, establishes a brand, and becomes the incumbent player. This product is well positioned to be the industry leader.

STRATEGY & IMPLEMENTATION SUMMARY

Our strategy for this market is straightforward:

- It is our desire to obtain a quick, referable install base.

- Build relationships with neighboring hospitals.

- Emphasize quick installations with high-quality service and support.

Strategy Pyramids

To achieve a quick referable install base, our main tactic is to call the hospitals where we have information system interfaces already completed. This provides us an extremely quick installation and another reference site. It meets our objective of building an install base. This market can be identified through user groups. Our specific programs include mailing to these hospitals, Internet demonstrations of the product, direct selling, and attending trade shows.

Our next strategy is to build upon our successes by marketing to hospitals in the immediate vicinity of the install base. Successful references are great selling tools and successful installations are great sites for other nearby hospitals to visit. Physicians can be a great asset by pressing other providers to extend to them the same information services they are receiving from a local hospital. Our specific program is to call and escort neighboring facilities to visit the installation site. Also, having these references document their "return on investment" aids the selling and decision cycle.

Quick and successful installations are the key to meeting our business plan. By carefully choosing our installs, we will avoid a developing trap by interfacing to a difficult closed-in system. Our specific plan to avoid this is to partner with other solution providers who have expertise in areas we do not, and allow them to sell and install the product.

Value Proposition

Our value proposition is straightforward. The product solution provides daily users of information a highly improved delivery mechanism. This delivery includes the following:

- Accessibility: information is accessible via any web browser.

- Availability: from any browser, laptop, or PDA.

- Accuracy: via legacy system or depository (real time data).

- Affordability: time savings at all points of access and use.

- Accountability: information is encrypted and audited from within.

As an example of value, physicians pay a monthly fee for a pager that only instructs them to call a number. For an equivalent monthly fee, our product provides the physician with immediate access to information that allows him to care for the patient, make decisions, and perform billable work.

Competitive Edge

Our competitive edge exists because we have chosen the right technologies, have been early to the market, and have a plan to quickly establish an install base. This install base will continue to grow because the product itself can be the front end to a multitude of functions. The product is not canned; thus, the user can continue to develop and enable new applications. The single web session can be used for hospital information, payor information, employee benefit sections, and links to other web site and content areas such as MedScape. Existing customers have already returned to ask for new links, new connections, and new modules.

Our competitive edge will be maintained as interfaces to various legacy systems are built into a library. This significantly improves the deployment time for a user. Also, we have established a vendor certification program allowing vendors to forward to us pre-releases of their software to insure compatibility.

Our competitive advantage also will be maintained due to the daily use of the product by our customers, and the difficulty to undo the connections and replace the access to many systems. Additionally, we are in a strong competitive position because information systems vendors are not focused on building web-enabled interfaces for a cross vendor market.

Others who will enter this market will face vigorous competition from us.

Marketing Strategy

The marketing strategy is the core of the main strategy:

- To obtain a quick and referable install base, we will heavily focus on our target market of 1,486 hospitals with 200 beds or more. Of these 1,486 hospitals we have an immediately installable solution for 291 of these hospitals. These 291 hospitals represent HBOC systems running on IBM's AS/400 for which we have already developed an interface which has been successfully running for two years. These 291 hospitals have a user group to whom we have spoken and will continue to work with in the future. Direct mailings, direct selling, and referencing is the strategy we will use with these accounts.

- Upon the successful installation of a hospital we will immediately contact nearby hospitals. We will build from the install location outward. We also will request the senior management of a successful, newly installed hospital for references to other senior healthcare executives that might have an interest in our product. We know that managers of information systems often refer solutions to their peers in the industry.

- The medical community has a flavor of a fraternal order. Especially among like users of a common software and hardware platform. By having quick installations with quality service and support, we are a very referencable solution. Normal installations of health information systems are very long and complex. Managers of information systems are excited when solutions work and vendors keep their commitments. Unfortunately, this is not the normal experience for most installations. Our service and support sets us apart.

- The new marketing strategy of approaching IPAs in each medical community to influence hospitals will make decisions by hospitals happen quicker and will have a positive impact on growth.

Positioning Statement

For medical and administrative professionals who need immediate access to patient information from a variety of systems, this product delivers that information to them from one single source, anywhere, anytime. Unlike their present environment, that may require many attempts and many different computer skills, this product provides all pertinent information with one click.

Pricing Strategy

The price of the product is $75,000 for the server software and $595.00 per user of the software. User prices are then discounted based upon the volume of users. In addition to the software, we charge for interface programming, customization of screen design, installation, training, and maintenance of the product. These are billed at $180 per hour or $1,500 a day.

We provide the necessary hardware if the customer desires us to fulfill that need.

Customers may ask us to perform a prototype of the application. We do these prototypes at our normal consulting rates mentioned above.

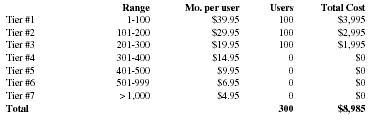

To help hospitals make a quick decision we have a rental model of the software. This rental model is based upon the following model:

| Range | Mo. per user | Users | Total Cost | |

| Tier #1 | 1-100 | $39.95 | 100 | $3,995 |

| Tier #2 | 101-200 | $29.95 | 100 | $2,995 |

| Tier #3 | 201-300 | $19.95 | 100 | $1,995 |

| Tier #4 | 301-400 | $14.95 | 0 | $0 |

| Tier #5 | 401-500 | $9.95 | 0 | $0 |

| Tier #6 | 501-999 | $6.95 | 0 | $0 |

| Tier #7 | > 1,000 | $4.95 | 0 | $0 |

| Total | 300 | $8,985 |

Minimum length of time is 36 months. This model includes maintenance. Hospitals are more flexible with an operating budget than a capital budget. In case the hospital would like to rent and convert later to a purchase model, we accrue a percentage of the rental towards the purchase price.

Promotion Strategy

- Our promotion strategy is via direct sales to the healthcare marketplace. We have a tight target market which we call directly. We work with senior level management and influential physicians. Our sales brochures help to illustrate the ease of use of the software.

- One brochure is targeted for the hospitals and another brochure will target physicians and IPAs.

- We will develop a brochure for the third-party administrator market.

- We will use telemarketing especially prior to trade shows.

- A public relations campaign and press releases will be developed.

- A web site will be created at QuikMedInfo.org

Distribution Strategy

We have signed agreements with distributors who have products complementary to our own. They already have client relationships and can easily add this product in their product offerings. Distributors have an annual quota and percentage discounts related to their self sufficiency in selling the product.

There are distributors that would like to embed the product in their software—the industry terms that to be "OEMing" (other equipment manufacturer) the product. These distributors receive a much higher discount but are required to purchase substantial inventory and offer the first level of customer support.

Marketing Programs

Our direct sales force is currently comprised of two marketing representatives, one for the eastern half of the United States and the other for the western half.

Both sales people have an annual objective of five hospitals to be installed. They are each responsible for calling the customer base, identifying and qualifying prospects, demonstrating the product, and closing the sale. They are both responsible for having $1.5 million of qualified opportunity defined at any one time. They are to make 100 calls a week and update those calls in a customer database. They are responsible for managing their own travel budget and expenses. They are not allowed to travel to a healthcare facility until all appropriate people are available for the meeting. This has worked well in the past and eliminated flights to interested but unqualified prospects.

Direct sales is very important as the sales cycle is long in the healthcare market. The direct selling effort is increased by visiting existing prospects and finding new prospects at trade shows.

Telesales coordinates all mailings to customers. These mailings include marketing material, product newsletters and press releases. Some type of literature is sent every six weeks to the customer and prospect database. All mailings are carefully recorded and response to those mailings is recorded.

Ed Roost of Best Midwest Solutions, Inc. already travels nationally and calls upon prospects with the representatives. Rachel Brown also visits with other CEOs to build strategic relationships.

Sales Strategy

Our sales strategy is to prospect our target market for potential customers. Upon finding customers that have a need, we offer a specific solution to that need. We follow our prospecting efforts with an online, Internet demonstration of the product. After successfully demonstrating the product, we schedule an onsite visit to the healthcare facility when all pertinent people can attend the meeting. We have found that physicians are our greatest advocate and we strive to make sure that they are a part of our onsite meeting. After a successful onsite presentation, we offer to perform a site survey that is billable. The site survey results in a working document defines the environment, the complexities, similarities, interfacing requirements and any customization required. From the site survey, we build a proposal that lists the price of the server, the seat cost based on the number of users, the interfacing costs, the customization programming needed, installation, training, etc. We work with the customer to review the findings and make certain all areas have been addressed.

Upon acceptance of the proposal the customer is provided with license agreements, maintenance agreements, and a Professional Services Agreement with specific work exhibits that detail the customization and interface programming costs. Customers are then entered into our customer support system that tracks the release level of software, technical contacts, all support calls, and repairs.

Sales Analysis

The long-range goal is to develop QuikMedInfo as an enterprise Intranet application solution for the healthcare industry and utilize the Java-based server technology to provide a number of Intranet application solutions to all types of industries. This goal will be achieved by the success of the introductory two-year plan. In addition, version upgrades will be based on seat licenses and maintenance.

The long-range plan is based on a successful introduction of QuikMedInfo to the healthcare industry. There will be a feasible strategy to successfully launch QuikMedInfo and establish brand recognition for a new line of Intranet application solutions and meet the two-year sales goals.

The sales will be derived from hospitals through locally controlled physician advisory boards. QuikMedInfo will be comprised of a server and seven different modules: Admissions, Transcriptions, Laboratory, Imaging, Pharmacy, Home Health, and Physician Management. Revenues also will be generated from computer and network hardware, server, and seat licenses, installation and training of these products to new hospital installations.

In the healthcare industry, there are 5,057 hospitals, representing the market in which the company has targeted. The company's target market is hospitals with over 200 beds, which is currently 1,486. Of these 1,486 hospitals, the company anticipates being the market leader and obtaining 20% of this market share. This will equate to 300 hospital installations in the first two years.

Based on effective marketing and sales in the first two years the company will position QuikMedInfo as a long-term solution for data resource gathering in the healthcare industry.

Sales Forecast

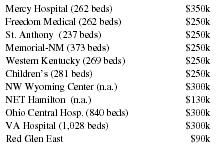

The following is our list of potential sales:

| Mercy Hospital (262 beds) | $350k |

| Freedom Medical (262 beds) | $250k |

| St. Anthony (237 beds) | $250k |

| Memorial-NM (373 beds) | $250k |

| Western Kentucky (269 beds) | $250k |

| Children's (281 beds) | $250k |

| NW Wyoming Center (n.a.) | $300k |

| NET Hamilton (n.a.) | $130k |

| Ohio Central Hosp. (840 beds) | $300k |

| VA Hospital (1,028 beds) | $300k |

| Red Glen East | $90k |

The expected three-year sales forecast is illustrated and more carefully broken down in its appropriate table.

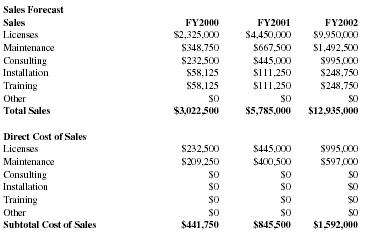

| Sales Forecast | |||

| Sales | FY2000 | FY2001 | FY2002 |

| Licenses | $2,325,000 | $4,450,000 | $9,950,000 |

| Maintenance | $348,750 | $667,500 | $1,492,500 |

| Consulting | $232,500 | $445,000 | $995,000 |

| Installation | $58,125 | $111,250 | $248,750 |

| Training | $58,125 | $111,250 | $248,750 |

| Other | $0 | $0 | $0 |

| Total Sales | $3,022,500 | $5,785,000 | $12,935,000 |

| Direct Cost of Sales | |||

| Licenses | $232,500 | $445,000 | $995,000 |

| Maintenance | $209,250 | $400,500 | $597,000 |

| Consulting | $0 | $0 | $0 |

| Installation | $0 | $0 | $0 |

| Training | $0 | $0 | $0 |

| Other | $0 | $0 | $0 |

| Subtotal Cost of Sales | $441,750 | $845,500 | $1,592,000 |

Sales Programs

Our sales programs are via direct mail and trade shows.

Via our direct mail campaign we send letters and success stories to our target market. These letters may include recent press releases, editorials featuring our product, along with our marketing literature. Mailings include the invitation for a free demo of the product over the Internet. The mailings also may be oriented towards an upcoming trade show that specifically states our booth and the marketing representatives to work with for their particular area. The sales reps are given this information for follow up and to personally invite the prospects and customers.

Educational seminars and end user groups are another avenue we use to educate customers on our technology, services, and expertise. Educational seminars can often be funded by the various professional associations. End user groups provide a wonderful opportunity to market and sell the product and its benefits.

Strategic Alliances

Strategic alliances already in progress include:

Skyenergy, Inc., a wholly owned subsidiary of Northwest Power and Light (a major regional utility company), specializes in application hosting and data transport over its eight-state fiber-optic network. It has shown great interest in the purchase of licensees of the product. Skyenergy currently has a contract with Blue Cross/Blue Shield of Kentucky to provide services to all BC's providers. The QuikMedInfo product can instantly be used in this environment.

Timbute Corp., a potential joint venture partner, is a large player in medical diagnostic imaging. It already has distribution of its platform, and a substantial revenue and client base. We would be an add-in service.

Sun Microsystems has already agreed to do maintenance and support where required. They have complete diligent knowledge of the product.

No agreements have been signed to date. Many other strategic potential partners exist.

Milestones

Our most significant milestone to date? Our "installed customers." They are very happy with the QuikMedInfo product and are excellent references. They include:

Thomas Medical Center (268 beds) - Installed August 1998

Thomas is the original customer that conceived the need for such a product and offered its employees and staff to assist in the initial requirements documentation. Thomas presently uses the product extensively in medical records. Thomas uses the product for one view of patient demographics, document images, and pharmacy. The customer is initiating the laboratory views of the product and will follow shortly with transcriptions.

Trinity 7 Communications - Installed January 1997

Trinity 7 Communications is a provider of telecommunication services. The company offers paging, cellular, voice mail, email, and long distance products. These services may be provided by many vendors. The software product allows them one common view to these different providers and their different systems.

Michelin Wool - Installed February 1998

Michelin Wool is one of the nation's largest third-party administrators and managed care companies. It offers physician management services as well. Michelin Wool uses the product to allow physicians access over the Internet for eligibility, authorizations, claims status, etc. Michelin has purchased a tool kit and is developing some of its own designs.

State of Oregon - Installed March 1999

The state of Oregon has purchased the product to use in a federal and state program called CHIPs (Childrens' Health Insurance Program). This product allows a provider to check a child's eligibility with the primary payors in the state prior to rendering services and before applying the charges to the state fund. This is a highly advanced application as the entire transmissions are secure and encrypted from all aspects.

Greene Medical Center of Titan, Oregon - Installed April 1999

Greene Medical Center uses the product to interface to several HBOC systems. The company retrieves information from lab, patient demographics, pharmacy, and is developing an interface for transcriptions. This customer may purchase a tool kit to develop some of its own applications.

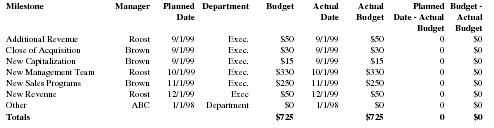

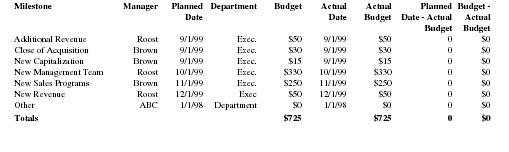

Other forthcoming milestones are summarized in the following table:

| Business Plan Milestones | ||||||||

| Milestone | Manager | Planned | Department | Budget | Actual date | Actual Budget | Planned Date - Actual Budget | Budget - Actual Budget |

| Additional Revenue | Roost | 9/1/99 | Exec. | $50 | 9/1/99 | $50 | 0 | $0 |

| Close of Acquisition | Brown | 9/1/99 | Exec. | $30 | 9/1/99 | $30 | 0 | $0 |

| New Capitalization | Brown | 9/1/99 | Exec. | $15 | 9/1/99 | $15 | 0 | $0 |

| New Management Team | Roost | 10/1/99 | Exec. | $330 | 10/1/99 | $330 | 0 | $0 |

| New Sales Programs | Brown | 11/1/99 | Exec. | $250 | 11/1/99 | $250 | 0 | $0 |

| New Revenue | Roost | 12/1/99 | Exec | $50 | 12/1/99 | $50 | 0 | $0 |

| Other | ABC | 1/1/98 | Department | $0 | 1/1/98 | $0 | 0 | $0 |

| Totals | $725 | $725 | 0 | $0 | ||||

MANAGEMENT SUMMARY

The new management team will be comprised of individuals who are currently with Empire Systems or other respected corporate leaders in the industry. They already understand the market and have been responsible for product development and sales penetration to date. Management bios follow.

Organizational Structure

Our organization structure is divided into three functional areas:

1. Product development and support — The role of this function is to continue to develop the product and new modules, write the appropriate interfaces and customized programs and offer maintenance for the product.

2. Sales and marketing — The role of sales and marketing is to market the product, educate customers, and build a reference base of customers. Sales and marketing conducts telesales, direct sales, etc.

3. General administration — This group manages the sales, invoicing, collection, and accounting of the group. It provides oversight of the entire organization.

Management Team

The management team includes the following individuals. Ed Roost will serve as CEO either on an interim or permanent basis. The potential exists in the personnel forecast to recruit and add a CEO.

Senior Executive Vice President—Rachel Brown is the co-founder of Best Source Solutions, Inc. She is a 1980 graduate of the University of Cincinnati (Accounting degree). She worked for Arthur Anderson in Denver and then worked for IBM from 1980 to 1987, leaving the company as a marketing manager in Point Kenton, Ohio. She was responsible for such accounts as General Electric, Great Lakes Banking, and other major accounts. Rachel became Senior Vice President of Memblast in Cincinnati, Ohio, and was responsible for computer equipment brokerage and leasing. She purchased an interest in a small software company to bring it home to Louisville, Kentucky. In 1990 she started Best Source Solutions and is responsible for the day-to-day sales of that company. Rachel will continue to run Best Source Solutions.

Executive Vice President - Ed Roost is the current President of Empire Systems, Inc. He has 18 years of experience in sales and marketing including six years in sales with IBM. He and his partner Rachel Brown began Empire five years ago and have built a profitable company with $45 million in annual revenues. Ed has the most day-to-day experience and working knowledge of the QuikMedInfo software. He has been responsible for all current sales and prospects.

Vice President of Sales - Nicholas DiMuzzio brings eight years of marketing experience to the healthcare area. Prior to becoming Vice President of Sales, he represented Redheart, a surgical supply vendor for acute care hospitals. DiMuzzio's experience also includes six years with American Health Buys where his duties included project engineering and contract negotiations with sales and marketing for their large buying groups.

Vice President of System Design - Monica Wren is one of the key developers of the product. She brings 13 years of programming, design, development, support, integration, implementation, and project management experience to the company. Prior to her career at Empire she worked in development for IBM, Richards Computer, and Mileage H. Research Corporation.

Vice President of Project Management - Henry Nerth is another key developer of the product. He brings 14 years of programming, design, development, support, integration, implementation, and project management experience to the company. Prior to his career at Empire he worked in development for Richards Computer and Mileage H. Research Corporation.

Application Developer - Ben Hogan has 11 years' experience in programming. His core talents lie in the area of application design and implementation in third-generation languages such as C, C++, and Java. Hogan also has experience in the management of large development projects, most recently the migration of a data warehousing application written in C to the IBM AS/400.

Management Team Gaps

There is a gap for a permanent CFO. It is expected that a temporary CFO will be utilized in year one and year two. A controller needs to be recruited, as well as additional sales people and administrative staff.

Personnel Plan

The company has its personnel needs well defined to handle expected growth.

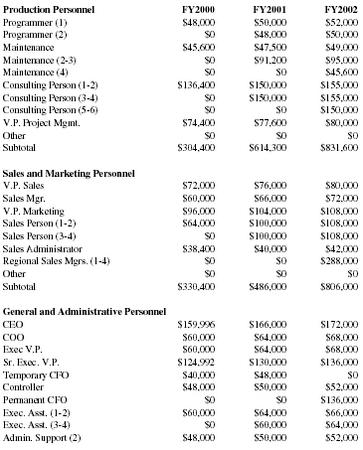

| Production Personnel | FY2000 | FY2001 | FY2002 |

| Programmer (1) | $48,000 | $50,000 | $52,000 |

| Programmer (2) | $0 | $48,000 | $50,000 |

| Maintenance | $45,600 | $47,500 | $49,000 |

| Maintenance (2-3) | $0 | $91,200 | $95,000 |

| Maintenance (4) | $0 | $0 | $45,600 |

| Consulting Person (1-2) | $136,400 | $150,000 | $155,000 |

| Consulting Person (3-4) | $0 | $150,000 | $155,000 |

| Consulting Person (5-6) | $0 | $0 | $150,000 |

| V.P. Project Mgmt. | $74,400 | $77,600 | $80,000 |

| Other | $0 | $0 | $0 |

| Subtotal | $304,400 | $614,300 | $831,600 |

| Sales and Marketing Personnel | |||

| V.P. Sales | $72,000 | $76,000 | $80,000 |

| Sales Mgr. | $60,000 | $66,000 | $72,000 |

| V.P. Marketing | $96,000 | $104,000 | $108,000 |

| Sales Person (1-2) | $64,000 | $100,000 | $108,000 |

| Sales Person (3-4) | $0 | $100,000 | $108,000 |

| Sales Administrator | $38,400 | $40,000 | $42,000 |

| Regional Sales Mgrs. (1-4) | $0 | $0 | $288,000 |

| Other | $0 | $0 | $0 |

| Subtotal | $330,400 | $486,000 | $806,000 |

| General and Administrative Personnel | |||

| CEO | $159,996 | $166,000 | $172,000 |

| COO | $60,000 | $64,000 | $68,000 |

| Exec V.P. | $60,000 | $64,000 | $68,000 |

| Sr. Exec. V.P. | $124,992 | $130,000 | $136,000 |

| Temporary CFO | $40,000 | $48,000 | $0 |

| Controller | $48,000 | $50,000 | $52,000 |

| Permanent CFO | $0 | $0 | $136,000 |

| Exec. Asst. (1-2) | $60,000 | $64,000 | $66,000 |

| Exec. Asst. (3-4) | $0 | $60,000 | $64,000 |

| Admin. Support (2) | $48,000 | $50,000 | $52,000 |

| Other | $0 | $0 | $0 |

| Subtotal | $600,988 | $696,000 | $814,000 |

| Research & Development Personnel | |||

| V.P. R&D | $64,000 | $102,000 | $108,000 |

| V.P. System Design | $74,400 | $77,600 | $80,000 |

| Application Eng. | $45,600 | $47,500 | $49,000 |

| Development Person (1-2) | $129,600 | $136,000 | $140,000 |

| Development Person (3-4) | $0 | $130,000 | $136,000 |

| Development Person (5-6) | $0 | $0 | $133,000 |

| Other | $0 | $0 | $0 |

| Subtotal | $313,600 | $493,100 | $646,000 |

| Total Headcount | 24 | 36 | 45 |

| Total Payroll | $1,549,388 | $2,289,400 | $3,097,600 |

| Payroll Burden | $340,865 | $503,668 | $681,472 |

| Total Payroll Expenditures | $1,890,253 | $2,793,068 | $3,779,072 |

FINANCIAL PLAN

It is expected that the initial $3 million investment will be sufficient for the first three years of this plan. Revenues should be sufficient to allow for a bank line to cover small shortfalls. Major ramp-up occurs in year four with a mezzanine capitalization of debt/equity combined with a $1.5 million bank line. Such a move could occur earlier if the situation permits. The nature of the software business is high margin and cash flow which also could permit growth without substantial equity dilution.

Important Assumptions

It is assumed that a bank line would be around 8% while a coupon on a mezzanine structure would be at 13% and could include warrants and/or an equity component. It is assumed that 90% of sales will be on credit via lease. If these are sold through a third party lessor, cash flow would accelerate. If QuikMedInfo should become its own lessor or offer access via the web, cash flow would spread more evenly.

For the purpose of this plan third-party leasing is the basis for projected revenues.

Other assumptions follow:

| General Assumptions | |||

| FY2000 | FY2001 | FY2002 | |

| Short-term Interest Rate % | 8.00% | 8.00% | 8.00% |

| Long-term Interest Rate % | 13.00% | 13.00% | 13.00% |

| Payment Days Estimator | 30 | 30 | 30 |

| Collection Days Estimator | 45 | 45 | 45 |

| Inventory Turnover | 6 | 6 | 6 |

| Estimator | |||

| Tax Rate % | 34.00% | 34.00% | 34.00% |

| Expenses in Cash % | 1.00% | 1.00% | 1.00% |

| Sales on Credit % | 90.00% | 90.00% | 90.00% |

| Personnel Burden % | 22.00% | 22.00% | 22.00% |

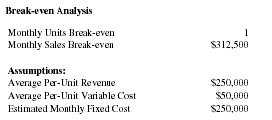

Key Financial Indicators

The most significant indicator is our gross margin. These exceed 80%. Cost of product is primarily packaging, pressing disks, manuals, and potential customer discounts. As long as margins are maintained there will be substantial margin for error in other plan aspects.

| Break-even Analysis | |

| Monthly Units Break-even | 1 |

| Monthly Sales Break-even | $312,500 |

| Assumptions: | |

| Average Per-Unit Revenue | $250,000 |

| Average Per-Unit Variable Cost | $50,000 |

| Estimated Monthly Fixed Cost | $250,000 |

At year one levels of burn rate, included fixed overheads, and full salaries, the company can sustain operation with just more than one installation per month.

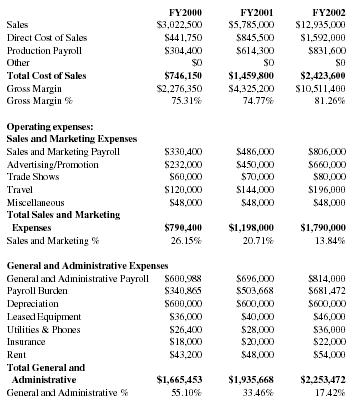

Profit and Loss (Income Statement)

Projected Profit and Loss

The company turns profitable at 24 months.

| FY2000 | FY2001 | FY2002 | |

| Sales | $3,022,500 | $5,785,000 | $12,935,000 |

| Direct Cost of Sales | $441,750 | $845,500 | $1,592,000 |

| Production Payroll | $304,400 | $614,300 | $831,600 |

| Other | $0 | $0 | $0 |

| Total Cost of Sales | $746,150 | $1,459,800 | $2,423,600 |

| Gross Margin | $2,276,350 | $4,325,200 | $10,511,400 |

| Gross Margin % | 75.31% | 74.77% | 81.26% |

|

Operating expenses:

Sales and Marketing Expenses |

|||

| Sales and Marketing Payroll | $330,400 | $486,000 | $806,000 |

| Advertising/Promotion | $232,000 | $450,000 | $660,000 |

| Trade Shows | $60,000 | $70,000 | $80,000 |

| Travel | $120,000 | $144,000 | $196,000 |

| Miscellaneous | $48,000 | $48,000 | $48,000 |

| Total Sales and Marketing Expenses | $790,400 | $1,198,000 | $1,790,000 |

| Sales and Marketing % | 26.15% | 20.71% | 13.84% |

| General and Administrative Expenses | |||

| General and Administrative Payroll | $600,988 | $696,000 | $814,000 |

| Payroll Burden | $340,865 | $503,668 | $681,472 |

| Depreciation | $600,000 | $600,000 | $600,000 |

| Leased Equipment | $36,000 | $40,000 | $46,000 |

| Utilities & Phones | $26,400 | $28,000 | $36,000 |

| Insurance | $18,000 | $20,000 | $22,000 |

| Rent | $43,200 | $48,000 | $54,000 |

| Total General and Administrative | $1,665,453 | $1,935,668 | $2,253,472 |

| General and Administrative % | 55.10% | 33.46% | 17.42% |

| Research & Development Expenses | ||||

| Research & Development Payroll | $313,600 | $493,100 | $646,000 | |

| Product Development | $288,000 | $488,000 | $966,000 | |

| Legal & Accounting | $39,600 | $42,500 | $48,000 | |

| Contract/Consultants | $36,000 | $48,000 | $60,000 | |

| Total Research & Development Expenses | $677,200 | $1,071,600 | $1,720,000 | |

| Research & Development % | 22.41% | 18.52% | 13.30% | |

| Total Operating Expenses | $3,133,053 | $4,205,268 | $5,763,472 | |

| Profit Before Interest and Taxes | ($856,703) | $119,932 | $4,747,928 | |

| Interest Expense Short-term | $0 | $0 | $0 | |

| Interest Expense Long-term | $0 | $0 | $0 | |

| Taxes Incurred | ($291,279) | $40,777 | $1,614,296 | |

| Net Profit | ($565,424) | $79,155 | $3,133,632 | |

| Net Profit/Sales | -18.71% | 1.37% | 24.23% |

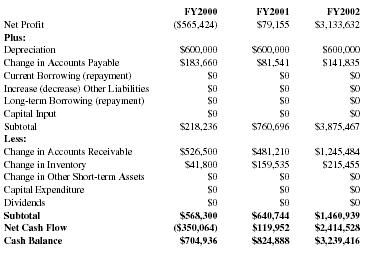

Proforma Cash Flow

Projected Cash Flow

Cash flow remains positive with the only potential exposure in year two. At that point sales shortfalls could deplete working capital. However, cut-backs also would be possible to the break-even levels of year one if required.

| FY2000 | FY2001 | FY2002 | |

| Net Profit | ($565,424) | $79,155 | $3,133,632 |

| Plus: | |||

| Depreciation | $600,000 | $600,000 | $600,000 |

| Change in Accounts Payable | $183,660 | $81,541 | $141,835 |

| Current Borrowing (repayment) | $0 | $0 | $0 |

| Increase (decrease) Other Liabilities | $0 | $0 | $0 |

| Long-term Borrowing (repayment) | $0 | $0 | $0 |

| Capital Input | $0 | $0 | $0 |

| Subtotal | $218,236 | $760,696 | $3,875,467 |

| Less: | |||

| Change in Accounts Receivable | $526,500 | $481,210 | $1,245,484 |

| Change in Inventory | $41,800 | $159,535 | $215,455 |

| Change in Other Short-term Assets | $0 | $0 | $0 |

| Capital Expenditure | $0 | $0 | $0 |

| Dividends | $0 | $0 | $0 |

| Subtotal | $568,300 | $640,744 | $1,460,939 |

| Net Cash Flow | ($350,064) | $119,952 | $2,414,528 |

| Cash Balance | $704,936 | $824,888 | $3,239,416 |

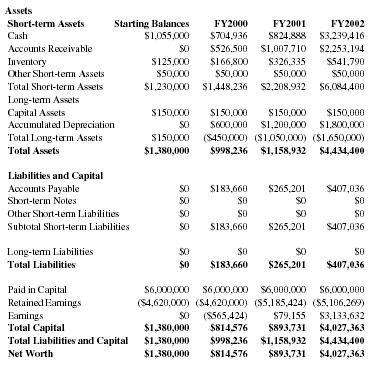

Owner's equity skyrockets in years three, four, and five.

Projected Balance Sheet

Proforma Balance Sheet

| Assets | |||||

| Short-term Assets | Starting Balances | FY2000 | FY2001 | FY2002 | |

| Cash | $1,055,000 | $704,936 | $824,888 | $3,239,416 | |

| Accounts Receivable | $0 | $526,500 | $1,007,710 | $2,253,194 | |

| Inventory | $125,000 | $166,800 | $326,335 | $541,790 | |

| Other Short-term Assets | $50,000 | $50,000 | $50,000 | $50,000 | |

| Total Short-term Assets | $1,230,000 | $1,448,236 | $2,208,932 | $6,084,400 | |

| Long-term Assets | |||||

| Capital Assets | $150,000 | $150,000 | $150,000 | $150,000 | |

| Accumulated Depreciation | $0 | $600,000 | $1,200,000 | $1,800,000 | |

| Total Long-term Assets | $150,000 | ($450,000) | ($1,050,000) | ($1,650,000) | |

| Total Assets | $1,380,000 | $998,236 | $1,158,932 | $4,434,400 | |

| Liabilities and Capital | |||||

| Accounts Payable | $0 | $183,660 | $265,201 | $407,036 | |

| Short-term Notes | $0 | $0 | $0 | $0 | |

| Other Short-term Liabilities | $0 | $0 | $0 | $0 | |

| Subtotal Short-term Liabilities | $0 | $183,660 | $265,201 | $407,036 | |

| Long-term Liabilities | $0 | $0 | $0 | $0 | |

| Total Liabilities | $0 | $183,660 | $265,201 | $407,036 | |

| Paid in Capital | $6,000,000 | $6,000,000 | $6,000,000 | $6,000,000 | |

| Retained Earnings | ($4,620,000) | ($4,620,000) | ($5,185,424) | ($5,106,269) | |

| Earnings | $0 | ($565,424) | $79,155 | $3,133,632 | |

| Total Capital | $1,380,000 | $814,576 | $893,731 | $4,027,363 | |

| Total Liabilities and Capital | $1,380,000 | $998,236 | $1,158,932 | $4,434,400 | |

| Net Worth | $1,380,000 | $814,576 | $893,731 | $4,027,363 | |

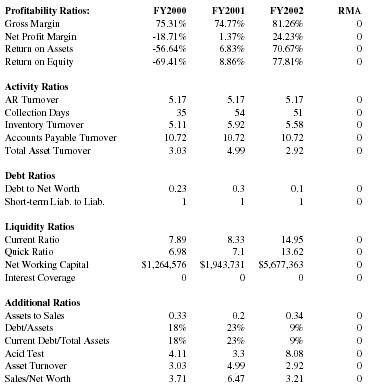

Business Ratios

Return on equity potential certainly warrants early stage investment.

Ratio Analysis

| Profitability Ratios: | FY2000 | FY2001 | FY2002 | RMA |

| Gross Margin | 75.31% | 74.77% | 81.26% | 0 |

| Net Profit Margin | -18.71% | 1.37% | 24.23% | 0 |

| Return on Assets | -56.64% | 6.83% | 70.67% | 0 |