SIC 0133

SUGARCANE AND SUGAR BEETS

This industry classification includes establishments primarily engaged in the production of sugarcane and sugar beets.

NAICS Code(s)

111991 (Sugar Beet Farming)

111930 (Sugarcane Farming)

Background and Development

The story of the sugar industry in the United States is in fact the story of two industries: one devoted to producing sugarcane and the other to producing sugar beets. Before the twentieth century, sugarcane accounted for 95 percent of world consumption of sugar. However, modern

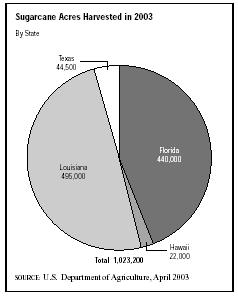

planting and refining techniques helped make sugar beet production profitable. By the 1980s, sugar beets and sugarcane shared equally in the U.S. sugar market. Sugar-cane was introduced to the United States from the Caribbean region by Jesuit priests traveling to Louisiana in 1751, and the first U.S. sugar refinery was built in the same state in 1795. Sugarcane is produced only in Florida, Hawaii, Louisiana, and Texas. Western pioneers desiring their own source of sugar began sugar beet production in the United States around 1870, but their efforts proved unprofitable until the development of irrigation systems in the 1890s. Beet production provided 25 percent of the nation's sugar needs by 1920. The Red River Valley area of Minnesota and eastern North Dakota are the largest U.S. beet producing regions.

Sugarcane and sugar beets are grown mainly to produce table sugar and sucrose. Sugarcane is also produced to manufacture alcohol as fuel for vehicles. Although refining processes for sugar sources are similar, cultivation and harvesting techniques are quite different. Sugarcane is planted using stalk cuttings, and matures between eight and sixteen months, depending on the region. A crop of sugarcane may produce acceptable yields for two to three years before being replanted and, in the case of Hawaii, where there is no danger of frost, can be harvested year round. Sugarcane is most often harvested mechanically, with specially designed harvesters that cut the stalk at the bottom, strip the unneeded leaves and top, and transfer the cane to a wagon. Prior to mechanical harvesting, sugarcane production required vast numbers of laborers who, in many cases, worked under conditions of slavery or near-slavery.

Grown primarily in twelve states, sugar beets, on the other hand, are harvested annually, and have benefited greatly from the attention of agricultural specialists who devised seed types and planting methods that encourage maximum yields. Still, great care must be taken to ensure adequate distance between plants, weed control, planting depth, and proper fertilization. One study showed that 50 percent of sugar beet production costs were expended in cultivation. However, mechanical cultivation and harvesting equipment makes labor costs in sugar beet production negligible. Both sugar industries have attained yields that are among the highest in the world: the average yield for sugarcane was roughly 35 tons per acre in the early 2000s; yield hovered at 20 tons per acre for sugar beets.

Sugar farmers, especially in Florida, faced environmental concerns throughout the 1990s. In 1991, the state was sued by the federal government to clean up the discharge from sugar farms as parts of Florida's Everglades were choked with cattails, a weed that grows from run-off from sugar fields. In 1999, the federal government revealed the Restudy, a major plan to clean up the Everglades.

Current Conditions

The U.S. sugar industry has long been bolstered by government programs designed to elevate the prices that sugar producers receive for their product. Prices for sugar have traditionally gone through dramatic swings, and this trend has continued into the early 2000s as the price per bushel of sugarcane jumped from $26.10 in 2000 to $29 in 2001.

In 1996, the U.S. government sought to alleviate farm subsidies and loans altogether. The 1996 Farm Bill called for the freezing and gradual reduction of agricultural loans and subsidies over a six-year period, resulting in termination of the program in 2002. Government assistance had been especially important to sugar producers because of the market's volatility. Though the bill met stiff resistance from sugar producers and lobbyists, it eventually passed, leading to some closures. In 2002, however, President Bush signed into law the 2002 Farm Bill, which extended farm subsidies for an additional six years.

The sugar industry has undergone a number of changes since the 1970s. Per capita consumption of sugar (both beet and cane) plummeted from 1970, when it stood at roughly 102 pounds, to 1980, when it stood at about 60 pounds. By 2002 it had fallen to 45 pounds. The corn sweetener market has claimed much of sugar's old market share. This steady drop in consumption led to a reduction in cane sugar refineries, from 22 in 1981 to just 12 at the turn of the twenty-first century.

Falling domestic consumption cost the U.S. sugar industry approximately $250 billion in 2001 alone. Between 1999 and 2003, domestic sugar sales fell from 10.11 million short tons in 1999 to 9.67 million short tons. As a result, production began to wane as well. Sugar beet acres planted fell from 1.42 million in 2001 to 1.36 million in 2002; acres harvested declined from 1.36 million to 1.33 million over the same time period. Similarly, sugarcane acres harvested fell from 1.02 million in 2001 to 995,000 to 2002. Minnesota, Idaho, North Dakota, California, and Michigan led in sugar beet production in 2003, while Florida and Louisiana led in sugarcane production.

Industry Leaders

In the early 2000s, the leading sugar farmers included A and B Hawaii Inc. at over $200 million in sales and 1,500 employees, as well as its subsidiary Hawaiian Commercial and Sugar Co. Also at the top of the industry heap was Sterling Sugars Inc. with $40 million in sales and 200 employees in 2003. U.S. Sugar and Flo-Sun are leaders in Florida; each controls 40 percent of the state's sugar industry. While the 1996 Farm Bill forced these companies to diversify to survive, the passage of the 2002 Farm Bill has eased the pressure to do so.

America and the World

Low world sugar prices threatened U.S. import protections at the turn of the twenty-first century and was predicted to increase Mexico's access to the U.S. sugar market. According to the USDA, imports from Mexico reached 260,000 tons in 2000, compared to 155,000 tons the previous year. Thanks to NAFTA, Mexico may import roughly 280,000 tons of sugar, duty-free, to the United States as of 2001.

Further Reading

ASCS Commodity Fact Sheet: Sugar. Washington, DC: U.S. Agricultural Stabilization and Conservation Service.

Ayer, Harry. "The U.S. Farm Bill: Help or Harm for CAP and WTO Reform." Agra Europe, 24 May 2002.

Food and Agriculture Policy Research Institute. "Implications of the 2002 U.S. Farm Act for World Agriculture." 24 April 2003. Available from http://www.fapri.missouri.edu .

U.S. Department of Agriculture. "Sugar and Sweeteners." Washington, DC: 12 January 2004. Available from http://usda.mannlib.cornell.edu/reports/nassr/field/pcp-bba/acrg0603.txt .

U.S. Department of Agriculture. Track Records of U.S. Crop Production. Washington, DC: 2003. Available from http://usda.mannlib.cornell.edu/data-sets/crops/96120/track03d.htm .

"U.S. Sugar Looks to Sweeten Deal with Mexico." Internet Securities. 7 August 2002.

Ward's Business Directory of U.S. Public and Private Companies 2000. Farmington Hills, MI: Gale Group, 2000.

Comment about this article, ask questions, or add new information about this topic: