SIC 2392

HOUSE FURNISHINGS, EXCEPT CURTAINS AND DRAPERIES

This category covers establishments primarily engaged in manufacturing house furnishings from purchased materials, such as blankets, bedspreads, sheets, tablecloths, towels, and shower curtains. Those establishments producing house furnishings primarily of fabric woven at the same establishment are classified, according to fiber, in SIC 2211: Broadwoven Fabric Mills, Cotton; SIC 2221: Broadwoven Fabric Mills, Manmade Fiber and Silk; SIC 2231: Broadwoven Fabric Mills, Wool (Including Dyeing and Finishing); or SIC 2299: Textile Goods, Not Elsewhere Classified.

NAICS Code(s)

314911 (Textile Bag Mills)

339940 (Broom, Brush and Mop Manufacturing)

314129 (Other Household Textile Product Mills)

Industry Snapshot

For many years, house furnishings such as sheets, towels, and blankets functioned as basic household necessities. In the growing economy after World War II, however, these products were manufactured with new technology in an expanding palette of colors, prints, and styles—thus becoming more of an expression of personal taste. By the 1990s, it was easy and affordable for consumers to redecorate their rooms with coordinated bedroom and bath products offered by companies in this industry. Record housing starts and home sales in the early 2000s also helped to increase demand for bedding. However, industry shipments in each industry segment declined due to increased competition from imports and a sagging U.S. economy. Total industry shipments declined from $7.02 billion in 2000 to $6.59 billion in 2001.

Organization and Structure

In 2000, more than 100 companies employed more than 49,000 employees in this industry. The manufacture of sheets and towels was dominated by a few large corporations. Some of the other products covered in this classification included tablecloths, pillows, boat cushions, laundry bags, shower curtains, slipcovers, and mattress pads. These were produced by a variety of small manufacturers, thus creating a very fragmented sector of the market.

Of the entire market for textiles, home furnishings shared 15 percent. The fabricated textile products market (including home furnishings), accounted for 30 percent of the combined apparel and fabricated textile products market. Shipments of home furnishings and other textile products also grew much faster than other sectors.

Background and Development

The house furnishings market grew throughout the 1980s. Several factors contributed to the industry's relative strength. The home textile market was less penetrated by imports than other sectors of the textile industry. Also, home textiles were manufactured in a more automated process, with specialized machinery taking the place of the paid production worker. A large portion of the profits in this category was used to upgrade building and machinery. New capital expenditures—at $27 million in 1977—escalated to $81 million in 1995 as companies implemented new technologies at their manufacturing facilities. Companies continued to invest over the next several years; in 1997, capital expenditures reached $115 million.

Current Conditions

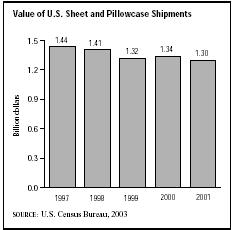

The top three companies with primary products in this category employed more than 1,000 workers each, while about 70 percent of the remaining companies employed fewer than 100 workers. The value of shipments of all products in these establishments, including but not limited to the primary products of the industry, grew from $2.3 billion in 1977 to more than $7 billion in 2000. However, the value of shipments declined to $6.5 billion in 2001. Specifically, the value of shipments in the various market segments in 2001 were as follows: shower curtains, comforters, quilts, pillows, blankets, mattress protectors, table linens, and slip covers at $3.9 billion; sheets and pillowcases at more than $1.3 billion; towels and washcloths at $801.3 million; and bedspreads and bedsets at $263.7 million. Although the value of product shipments in each sector declined between 2000 and 2001, continued growth in new home construction helped to somewhat offset the impact of a weakening U.S. economy throughout the early 2000s.

Of the industry's top 15 manufacturers, the majority saw decreases in 2003 sales compared to 2002. In fact, after sales declined 9.1 percent and losses mounted to $133 million in 2003, Westpoint Stevens filed for Chapter 11 bankruptcy protection and began shifting its focus from towels to bedding. Dan River Inc. filed bankruptcy in 2004; that firm had posted a $13 million loss on sales of $612 million in 2002. The most dramatic example of the industry's decline, however, was Pillowtex, which led the industry in 1997 with sales of more than one billion dollars, yet was unable to stay afloat in the early 2000s. By the end of 2003, the firm had liquidated operations and begun the process of auctioning off brand names such as Fieldcrest Cannon.

Industry Leaders

The top two companies in this industry earned more than $3.7 billion collectively in 2003. Westpoint Stevens had 2003 sales of $1.64 billion and 13,886 employees, while Springs Industries had 2002 sales of $2.1 billion and 17,000 employees.

Westpoint is the leader in sheets and pillowcases, whereas Springs is the leader in comforters, bedspreads, and shower curtains. Pacific Coast Feather Co. is the largest manufacturer of down comforters and the second-largest bedding company.

Workforce

There were 42,369 production workers and 49,303 total employees in the house furnishings industry in 2000. Production workers earned an average of $10.43 per hour and worked an average of 40 hours per week. Companies that manufactured sheets and pillowcases employed a total of 5,922 workers, with more than 90 percent in production. Employment has been decreasing in the home furnishings sector, but hourly earnings grew at the same rate as the industry average.

America and the World

Imports have not had as much impact on the home furnishings market as with the apparel market. However, the value of imports grew from about $1.2 billion to more than $3.6 billion at the turn of the twenty-first century.

The World Trade Organization Agreement on Textiles and Clothing, which phases out quotas by 2005, is expected to cost the United States four billion dollars in lost textile sales, according to the American Textile Manufacturers Institute. The largest threat will come from China, which imported $9.8 billion worth of apparel and fabricated textile products in 2002.

Exports grew at a much slower rate, from $448 million in 1992 to roughly $500 million by 2000. Canada and Mexico were the fastest growing markets in the early 2000s.

Further Reading

Leizens, Laticia. "Inching Forward." HFN: The Weekly Newspaper for the Home Furnishing Market, 23 February 2004.

U.S. Census Bureau. "Statistics for Industry Groups and Industries: 2000." February 2002. Available from http://www.census.gov/prod/2002pubs/m00as-1.pdf .

——. "Value of Shipment for Product Classes: 2001 and Earlier Years." December 2002. Available from http://www.census.gov/prod/2003pubs/m01as-2.pdf .

U.S. Department of Agriculture. "NAFTA: A Clear Success for U.S. and Mexican Textile and Cotton Trade." January 2004. Available from http://www.fas.usda.gov/info/agexporter/2004/January/pgs%2022-23.pdf .

Comment about this article, ask questions, or add new information about this topic: