SIC 2038

FROZEN SPECIALTIES, NOT ELSEWHERE CLASSIFIED

This industry comprises establishments primarily engaged in manufacturing frozen food specialties, not elsewhere classified, such as frozen dinners and frozen pizza. The manufacture of some important frozen foods and specialties is classified elsewhere. For example, establishments primarily engaged in manufacturing frozen dairy specialties are classified in SIC 2024: Ice Cream and Frozen Desserts; those manufacturing frozen bakery products are classified in SIC 2051: Bread and Other Bakery Products and SIC 2053: Frozen Bakery Products, Except Bread; those manufacturing frozen fruits and vegetables are classified in SIC 2037: Frozen Fruits, Fruit Juices, and Vegetables; and those manufacturing frozen fish and seafood specialties are classified in SIC 2092: Prepared Fresh or Frozen Fish and Seafood.

NAICS Code(s)

311412 (Frozen Specialty Food Manufacturing)

Industry Snapshot

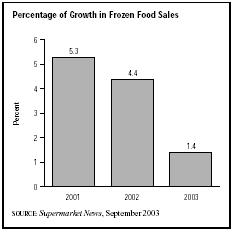

Due to increased competition from other sectors of the food industry, such as refrigerated entrees and ready-to-eat meals prepared by grocery store delis, frozen food sales began to weaken in the early 2000s. Frozen food sales grew 5.3 percent in 2001, 4.4 percent in 2002, and just 1.4 percent in 2003. Sales in 2003 totaled $27.1 billion. The frozen food segments performing well despite increased competition included frozen dinners, which saw a sales increase of 8.6 percent in 2003.

Background and Development

Clarence Birdseye is considered the father of the frozen food industry. He created the freezing process so that preserved foods did not need to be cooked immediately. Birdseye formed Birds Eye Foods Ltd. in London in 1954; it later became a subsidiary of Unilever. According to Quick Frozen Foods International, Birds Eye "virtually held an umbrella over the industry during the squalls of its infancy."

The frozen food industry evolved during the early 1960s as the proliferation of supermarkets and self-service stores made mass marketing of frozen food products profitable. At the same time, refrigerator-freezers and stand-alone freezers gained in popularity. The first frozen food products were vegetables, poultry, fish, and fruit in boilable pouches. Items such as frozen juice concentrate, ice cream novelties, baked goods, variety dinners, seafood, breakfast items, and pizza gradually entered the industry from the mid-1960s through the 1990s.

Beginning in the 1980s, standard TV dinners gave way to a variety of meals and frozen specialty items that offered more choices and met specific dietary requirements. Frozen food manufacturers targeted their products at the needs of busy families who desired quick meal preparation and a large variety. They also developed new frozen entrees for children.

The rapid growth in the industry is also attributable to the introduction of the microwave oven. In fact, Quick

Frozen Foods International called the combination of the microwave oven and frozen food a "marriage of convenience: Frozen food performs better in a microwave oven." The magazine reported that microwave oven owners spent 34 percent more on pizza, 29 percent more on breakfast foods, 19 percent more on entrees, and 16 percent more on dinners than non-microwave owners. Improvements in taste over the past 40 years also made frozen food specialties increasingly attractive to busy families.

Leading frozen food manufacturers engaged in damaging price wars and expensive trade promotions in the early 1990s. As a result, many companies began shifting their focus toward generating profits from existing products instead of launching new brands and line extensions.

In the 1990s, dual-income households and the convenience of microwave ovens contributed to annual growth in the frozen food category. However, consumers also complained about the poor texture and inferior browning effect of microwaveable foods. Cognizant of this concern, technicians in the food additives field increased research into methods to improve the flavor, texture, color, shelf-life, and nutritional benefits of frozen foods.

At the close of the 1990s, industry analysts were urging the frozen food industry to develop new prepared foods in order to avoid losing additional market share to ready-to-eat meals, including microwavable shelf-stable and refrigerated items. Sales of such products could erode the market share held by frozen foods, which was 18 percent of total supermarket sales in 1999, according to Techtronic, Inc.

Current Conditions

The frozen food industry grew from a $250 million retail business in 1947 to more than $20 billion by the 1990s, according to the National Frozen Food Association. Total retail sales in 2003 reached $27.1 billion, compared to $24 billion in 1997. The dinner and entree category was the largest—with sales of more than $5 billion. Frozen dinners, the fastest growing segment of the industry in 2003, saw sales increase by 8.6 percent that year.

Convenience in preparation is the primary appeal of frozen foods. Americans used fewer and fewer ingredients to prepare their meals in the late 1990s and early 2000s and often substituted frozen foods for fresh produce. However, the increasing popularity of ready-to-eat refrigerated and microwavable shelf-stable foods, as well as take-home meals prepared by supermarket delis began to undercut frozen food sales. While units sold grew by 0.8 percent in 2001, prompting sales to jump 5.3 percent, unit sales declined by 0.8 percent in 2002 and by 0.6 percent in 2003, resulting in sales growth of only 4.4 percent and 1.4 percent, respectively. According to a September 2003 issue of Supermarket News, "The vast majority of frozen foods out there aren't as convenient as they once were. The increasing variety available from restaurant concepts, and even the supermarket's own deli and prepared-food departments, has collectively drawn away the demographic that viewed frozen foods as convenient."

Concerns about health and nutrition also led consumers to reduce their intake of foods containing fat and sodium in the late 1990s and to reduce their intake of carbohydrates in the early 2000s. The specialty frozen food industry responded by offering low-cholesterol and low-fat products in the late 1990s and low-carb products in the early 2000s. Weight Watchers, for example, which already offered low-fat entrees, sandwiches, desserts, and pizzas in the late 1990s, introduced a line of low-carb frozen dinners in the early 2000s.

At the same time, despite the growing number of health conscious shoppers, the frozen snacks sector, which included pizza rolls, frozen pretzels, and Mexican and Asian food snacks, experienced particularly strong growth throughout the late 1990s and early 2002. Between 1997 and 2002 frozen snack sales grew 53 percent to $908 million. These sales were expected to grow another 47 percent by 2007 to $1.3 billion.

By the early 2000s, a variety of frozen ethnic foods such as Mexican, Tex-Mex, and Asian entrees had expanded beyond their regional markets to reach the vast majority of American households. In fact, sales of Asian entrees grew 4.4 percent to $512 million in 2003, outpacing overall industry growth considerably.

Further Reading

American Frozen Food Institute Web Site, 2000. Available from http://www.affi.com/facts/decafood.htm .

Murray, Barbara. "Stuck In Time." Supermarket News, 8 September 2003.

Zimoch, Rebecca. "What's Hot in the Freezer Case." Grocery Headquarters, December 2003.

Comment about this article, ask questions, or add new information about this topic: