SIC 2673

PLASTICS, FOIL AND COATED PAPER BAGS

This category covers establishments primarily engaged in manufacturing bags of unsupported plastic film, coated paper, metal foil, or laminated combinations of these materials. These bags can be printed or unprinted. Establishments primarily engaged in manufacturing uncoated paper bags and multiwall bags and sacks are classified in SIC 2674: Uncoated Paper and Multiwall Bags; those manufacturing textile bags are classified in SIC 2393: Textile Bags; and those manufacturing garment storage bags, except of plastics film and paper, are classified in SIC 2392: Housefurnishings, Except Curtains and Draperies.

NAICS Code(s)

322223 (Plastics, Foil, and Coated Paper Bag Manufacturing)

326111 (Unsupported Plastics Bag Manufacturing)

Note: The U.S. Economic Census now reports industrial information under the North American Industry Classification System (NAICS) instead of the Standard Industrial Classification (SIC) system. As a result, the value of shipments data reported below is for NAICS 322223 (the replacement for SIC 2673 ), and includes only a small portion of what used to be reported for SIC 2673. For example, the 1994 value of shipments for SIC 2673 was reported at $6.02 billion; in 1997, the value of shipments for NAICS 322223 was reported at just $512 million.

While this category is classified under paper and allied products, the industry actually uses very little paper in its products, and even that small percentage is declining. The vast majority of products in this industry are made exclusively from plastic.

Products found in this classification include merchandise bags, trash bags, waste bags, frozen food bags, garment storage bags, and wardrobe bags. The vast majority of products manufactured in this sector are specialty bags, pouches, and liners, multiweb laminations and foil, except film. This segment accounted for 60 percent of total shipments in 2001, down from 71 percent in 1997. Shipments for this segment had declined steadily throughout the late 1990s and early 2000s, from $399 million in 1997 to $292.5 million in 2001.

Other significant industry products include specialty bags, pouches, and liners, coated single-web paper, which accounted for 36 percent of total shipments in 2001. Shipments for this industry segment increased every year between 1997 and 2001, growing from $143 million to $176.1 million. Another category, plastics, foil, and coated paper bags not separated in kind, appeared to be on the decline. Shipments of these products declined from $19.6 million in 1997 to $14.2 million in 2001.

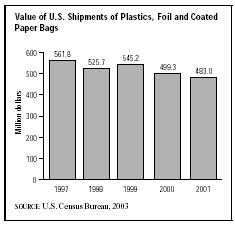

The performance of the plastic, foil, and coated paper bag industry produced a value of shipments of $483 million in 2001, down from $512 million in 1997, according to the U.S. Census Bureau. While the outlook for the industry was generally thought to be quite positive as more retail outlets converted to plastic merchandise bags and as other applications were developed in the late 1990s, the sluggish U.S. economy hindered industry growth in the early 2000s.

The biggest purchaser of plastic, laminated, and coated paper bags continued to be retail trade outlets (not including eating and drinking establishments). These retail outlets purchased about 60 percent of all bags produced in this category. Personal consumption and wholesale trade each accounted for less than 10 percent of the output. The remainder of product shipments was purchased by a wide variety of other sectors of the economy, mostly in manufacturing.

The vast majority of products produced by companies in this industry in 2001 were made from plastic resins or sheets. Plastic resins used in granule, pellet, powder, or liquid form accounted for about 40 percent of the materials consumed by this sector. Plastic products used in the form of sheets, rods, tubes, and other shapes accounted for about 15 percent. By contrast, paper accounted for just 5 percent of industry purchases. Other significant raw materials for this category include printing ink, paperboard containers, boxes and corrugated paperboard used to ship finished products, and glues and adhesives.

A large portion of this industry's output is in branded products, with trash bags being one of the leading products. Leading national brands include Glad, Hefty CinchSak, Hefty, and Glad Stress Flex. However, of the total U.S. trash bag market in 2003, private label products held a 33.9 percent share, compared to 20.5 percent in 1995. Total trash bag sales in 2002 declined 4.2 percent to $1.7 million. According to an April 2003 issue of

Private Label Buyer, "Declines in the overall trash bag segment can be partially attributed to ongoing environmental concerns, including the ongoing growth of recycling programs and push to reduce landfill waste."

The plastic, foil, and coated paper bag industry has made extensive use of new plastic materials to make products that are both lighter and stronger. For example, the use of high-density polyethylene by all manufacturers was expanding at a healthy 6 percent annual rate in the late 1990s. High-molecular weight resins offer major performance improvements over linear-low density polyethylene. While the primary application for this product is retail plastic bags, trash bag manufacturers are using this material as well to take advantage of its strength, toughness, and printability.

Further Reading

"In the Bag." Private Label Buyer. April 2003.

U.S. Census Bureau. "Statistics for Industry Groups and Industries: 2000." February 2002. Available from http://www.census.gov/prod/2002pubs/m00as-1.pdf .

——. "Value of Shipment for Product Classes: 2001 and Earlier Years." December 2002. Available from http://www.census.gov/prod/2003pubs/m01as-2.pdf .

U.S. Trade and Industrial Outlook, 2000. New York: McGraw-Hill, 1999.

Comment about this article, ask questions, or add new information about this topic: