SIC 4231

TERMINAL AND JOINT TERMINAL MAINTENANCE FACILITIES FOR MOTOR FREIGHT

TRANSPORTATION

This category includes establishments primarily engaged in the operation of terminal facilities used by highway-type property carrying vehicles. Also included are terminals that provide maintenance and service for motor vehicles. Terminals operated by motor freight transportation companies for their own use are classified in SIC 4212: Local Trucking Without Storage; SIC 4213: Trucking, Except Local; SIC 4214: Local Trucking With Storage; or SIC 4215: Courier Services, Except by Air. Separate maintenance and service facilities operated by motor freight transportation companies are classified as auxiliary.

NAICS Code(s)

488490 (Other Support Activities for Road Transportation)

Although trucking terminals provide a number of services, including showers for truckers and truck maintenance and repair, these establishments are primarily used for their storage and consolidation facilities. Freight is combined and redistributed at these terminals in an effort to reduce the distances and costs of transportation.

Terminals, therefore, are located in areas where the demand for transportation is high, and terminals are continually relocated according to shifting traffic patterns. While there are thousands of trucking terminals in the United States, most of these facilities are operated by trucking companies themselves and therefore are not included in this category.

The truck terminal industry boomed after the deregulation of the industry as a whole in 1980. Deregulation resulted in a 160 percent increase in the number of registered truckers between 1980 and 1991. These new truck companies were often small operations that could not afford to operate their own terminals. As the industry moved into the 1990s, however, shifts in both the economy and in distribution patterns reversed the truck terminal expansion. Although an increase in traffic in the southeastern United States fostered terminal growth in the south, many existing terminals were closed in the early 1990s.

A number of factors precipitated the terminal closings, such as the waning health of the trucking industry. By the late 1980s, many of the smaller operators who emerged after deregulation had been forced out of business. The post-deregulation boom was ended by the recession and an increase in competition from parcel carriers such as United Parcel Services. The remaining companies were large and generally operated their own terminal facilities. Even these large trucking companies were forced to streamline their terminal networks in the 1990s.

The focus on efficiency and quality in the 1990s further encouraged terminal closings. Shippers and truckers were committed to reducing cargo damage and handling costs. These reductions were often achieved by minimizing the number of times freight was handled. As such, truck terminals were eliminated from the transportation equation if their use proved unnecessary according to freight handling standards, which emphasized efficiency over short-term cost savings.

One bright spot in the trucking terminal facility industry was the growth of the intermodal industry in the 1990s. Intermodalism, or piggybacking, is the use of two or more modes of transportation for freight movement. Often, railroads were unable to obtain right-of-way into ports because of the unavailability of land, creating an opportunity for intermodal truck terminals to be built in major ports.

Although the decline of the trucking industry had a negative impact on terminals, the growth in intermodal service presented opportunities for truck terminal facility expansion. Truck terminal owners continue to reevaluate location and access in search of new opportunities in a shrinking market. The transportation industry as a whole was expected to experience modest annual growth into 2012.

The industry leader in 2001 was Brake Systems Inc. of Portland, Oregon. The company posted revenues of 11 million that year. As its name implies, Brake Systems Inc. specialized in manufacturing and installing a variety of brake types, brake systems, and brake system designs.

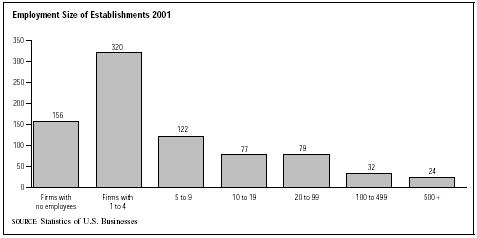

According to the Statistics of U.S. Businesses, there were 810 firms operating 1,031 establishments in this industry in 2001, an increase from the 769 firms just the year before. There were 17,541 total employees earning a payroll in excess of $452.5 million. About 17 percent of the firms employed 20 or fewer workers, and just 3 percent employed 500 or more.

Further Reading

Baker, Deborah J., ed. Ward's Business Directory of US Private and Public Companies. Detroit, MI: Thomson Gale, 2003.

"Brake Systems, Inc.," 2004. Available from http://www.brakesystemsinc.com .

U.S. Census Bureau. Statistics of U.S. Businesses: 2001. 1 March 2004. Available from http://www.census.gov/epcd/susb/2001/us/US332311.htm .

U.S. Department of Labor, Bureau of Labor Statistics. Economic and Employment Projections. 11 February 2004. Available from http://www.bls.gov/news.release/ecopro.toc.htm .

Comment about this article, ask questions, or add new information about this topic: