Financial Services Company

BUSINESS PLAN PRISMA MICROFINANCE, INC.

2 Claremont Street Boston,

Massachusetts 02118

Prisma MicroFinance, Inc., is a private, mission-driven company with operating subsidiaries in Central America that provide "microcredit" to entrepreneurs. Since 1995, Prisma has provided lending and savings services to people in the developing world considered "unbankable" by formal financial institutions. By operating a profitable private-equity funded business in the Nicaraguan microfinance market—where most competitors are nonprofits—the company seeks to revolutionize and to grow the world's microfinance industry.

- EXECUTIVE SUMMARY

- COMPANY OVERVIEW

- TARGET MARKET

- OPERATIONS & MANAGEMENT

- GROWTH STRATEGY & MILESTONES

- MARKETING & SALES STRATEGY

- FINANCIAL ANALYSIS

- IMPACT ANALYSIS & SOCIAL RETURN ON INVESTMENT

- APPENDIX

EXECUTIVE SUMMARY

Who We Are

Prisma MicroFinance, Inc., is a private, mission-driven company with operating subsidiaries in Central America that provide "microcredit" to entrepreneurs. Since 1995, Prisma has provided lending and savings services to people in the developing world considered "unbankable" by formal financial institutions. By operating a profitable private-equity funded business in the Nicaraguan microfinance market—where most competitors are nonprofits— the company seeks to revolutionize and to grow the world's microfinance industry. The company upholds a dual mission of providing affordable capital to "unbankable" individuals while operating an efficient, profitable business.

Why We Do It

At Prisma MicroFinance, access to affordable credit is considered a right, not a privilege. Providing affordable capital is a business model that will allow the company to offer reliable financial returns and significant social returns to its investors, while providing a valuable service to its borrowers. "We believe in doing well by doing good."

The Management

Prisma's management team has a total of over 25 years of experience in the microfinance industry. They have worked together for five years and their track record proves that they have the necessary skills to guide the company as it expands throughout Nicaragua and Central America.

The Market

The worldwide microfinance market is large, underserved, and growing at a rate of 30 percent annually. The worldwide market is estimated to be $270 billion, with current annual cash turnover of $2.5 billion. The Nicaraguan market is $300 million, with $50 million being lent at rates averaging 60 percent APR. There are more than 20 significant entities in Nicaragua providing microfinance services, with no single one holding more than 13 percent of market share.

The Customers

Prisma's customers are individuals who are not in an economic position to secure funding from traditional financial institutions. The majority are small-business owners, operating in the Nicaraguan capitol of Managua. Prisma has a strong lending history with taxicab owneroperators, and it plans to solidify its reputation within this market. By FY2004, its customer base will be an equal split of micro, small, and medium-size business owners.

Competitive Advantage and Profitability

Prisma embodies a profitable business model with four major components: local and inexpensive labor, market penetration in cooperative taxi financing, externalization of costs by partnering with third parties, and the use of effective technology. Unlike its competition, Prisma has operated without subsidies or grants since day one for over five years while also providing healthy returns to its financial backers. Moreover, Prisma lends at rates of 31-34 percent APR, two thirds of the average competitor's rate.

Marketing and Sales

Prisma's marketing and sales strategy has been extremely successful, yet extremely cheap. As word of mouth has been Prisma's biggest source of sales, marketing activities have been focused on keeping clients happy and recognizing their accomplishments. The social structure and business culture that has made this approach a success in Nicaragua exists throughout Central America.

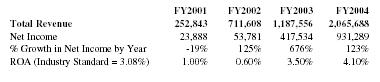

Financials

| FY2001 | FY2002 | FY2003 | FY2004 | |

| Total Revenue | 252,843 | 711,608 | 1,187,556 | 2,065,688 |

| Net Income | 23,888 | 53,781 | 417,534 | 931,289 |

| % Growth in Net Income by Year | -19% | 125% | 676% | 123% |

| ROA (Industry Standard = 3.08%) | 1.00% | 0.60% | 3.50% | 4.10% |

Key Milestones

FY2001

- Raise Series "B" $1.5 million Investment Round

- Grow loan portfolio to $1 million

- Make 2,000th loan

- Diversify portfolio to 60/40 taxi/non-taxi loans

- Expand board to 7 members

- Establish Advisory Board

- Report on new location for central office

FY2002

- Close Series "B" $1.5 million Investment Round

- Grow loan portfolio to $4 million with debt

- Make 4,000th loan

- Diversify portfolio to 50/50 taxi/non-taxi loans

- Expand Central Managua office

- Complete Central American expansion report

FY2003

- Raise Series "C" $4 million Investment Round

- Grow loan portfolio to $5 million

- Make 6,000th loan

- Diversify portfolio to 40/60 taxi/non-taxi

- Open second Nicaraguan office

- Lay groundwork for operations in second country

FY2004

- Close Series "C" $4 million Investment Round

- Grow loan portfolio to $10 million

- Make 10,000th loan

- Achieve balanced "Prisma Portfolio," even split of Micro, Small, Medium loans

- Open third and fourth Nicaraguan Offices

- Begin operations in second Central American country

Funding Goals

Prisma is raising $1.5 million in its Series "B" round to grow and expand business, both the total number of customers it serves and the region in which it offers service. The company has planned an aggressive, but realistic, expansion strategy. By the end of FY2004, Prisma will be lending 4,800 loans profitably in four Nicaraguan cities and a second Central American country with a total lending portfolio of $10.56 million.

Use of Funds

Prisma seeks to expand its current successful model. The funds from the sale of stock will be used to leverage debt in order to expand the loan portfolio.

COMPANY OVERVIEW

Prisma MicroFinance, Inc.'s, Mission Statement:

To provide our customers superior financial services, fostering opportunities for wealth and employment creation, while maximizing social and economic returns for our investors.

The Company

Prisma MicroFinance, Inc. (Prisma) is a United States corporation registered in the state of Massachusetts. The company was founded to be a development bank—making loans in small amounts widely available to people in the developing world. This growing industry is known as "microfinance."

The necessary capital to operate Prisma is raised through private equity and debt from individual and institutional investors in the developed world. With $1.5 million in new equity, the company will be able to support expansion efforts and leverage at least this amount in debt financing. This capital will accelerate growth, exponentially increasing the number of customers and amount lent. Prisma's customers are primarily business owners who do not have access to affordable capital to finance their operations because they are considered unbankable by traditional financial institutions. Although these poor business owners may operate on a very small scale, their operations are profitable. They remain locked in the poverty cycle because of the premium they pay for being perceived as a risky investment. Prisma's experience, and that of the microfinance industry in general, has proven just the opposite. Lending to poor individuals poses risks because of the precarious nature of their cash flows, but providing them access to affordable capital allows them to even out cash flows and break out of the poverty cycle.

Prisma does not conduct its operations for charity. It is at the forefront of the B2-4B revolution—meaning it is finding business solutions for the four million poor people of the world. Companies such as Hewlett-Packard are investing significant capital into this area not only because of the social upshot, but because it is good business. Prisma has operated profitably for five years by targeting a market opportunity that is large, underserved, and in which the competition is fragmented by industry standards. Prisma offers less expensive products to consumers with better service than its competitors.

Company Name

"Prisma" means "prism" in Spanish. Prisma MicroFinance, Inc. "refracts" private capital investment from the developed world, funneling it to small business owners in Central America who traditionally have lacked access to capital but who are entrepreneurial and commercially savvy operators.

Prisma's spectrum covers providing access to credit and financial services for people living in the developing world. The diversity in loan size creates a balanced portfolio serving a range of people. A single loan officer can easily and profitably manage a cost-effective portfolio that includes loans of different sizes. In this way, Prisma embraces its dual business focus of:

- Providing capital to "unbankable" clients

- Ensuring market rate returns for investors

Company History

Prisma was begun in 1995 as a savings and loan cooperative called SINAI, R. L. (Support and Incentives for Autonomous Initiatives) founded by a Nicaraguan, Roger Aburto, and an American, David J. Satterthwaite. They shared a common interest in assisting poor business owners overcome barriers to success. The two founders started operations completely through grassroots efforts with $1,000 in personal start-up capital and a $4,000 loan from American businessman George Kraus, who is now a Board Member. For its first two years, the company conducted its activities out of a single room in Roger's house with a home computer.

Prisma has grown steadily from the beginning, averaging 387 percent annual growth rate as measured by total loan portfolio under management.

Prisma Growth: 1996-2000

| Year | 1996 | 1997 | 1998 | 1999 | 2000 |

| Number of Loans, Year End | 99 | 310 | 530 | 395 | 236 |

| Portfolio Balance | $39,400 | $396,557 | $698,381 | $649,066 | $855,177 |

| Total Number of Loans Made | 257 | 607 | 1,099 | 1,419 | 1,519 |

The organization's growth has been funded completely with private investment. In December of 2000, the Nicaraguan loan portfolio was at just over $850,000 distributed to 236 loans. The average loan is $3,000 and is repaid within 22 months. Phenomenally, in 1,500 loans, Prisma's default rate is less than 1 percent. The single most limiting factor throughout Prisma's history has been lack of capital. At present, the organization has nearly 200 approved loans waiting for sufficient funds to grant them.

Prisma's first client in 1995, Arroya Rios Vallejos, borrowed $500 for inventory for her corner store. She has since received and repaid four loans, and now owns her own home.

Unlike the overwhelming majority of microfinance institutions that depend on donations, Prisma's entire loan portfolio has instead been financed by debt from individuals and commercial institutions. Prisma has consistently offered interest rates at 31-36 percent APR, significantly lower than the competition's rates of 60-80 percent APR. The company has continually sought to maintain efficient and modern operations, thus creating a vibrant business culture prepared to confront a demanding marketplace.

Products Offered

Prisma is a financial institution. Its principal operations are as a lender to customers typically viewed by the industry as "unbankable." Prisma makes loans, at risk-adjusted market rates, from $50 to $15,000 dollars. This range is often referred to in the lending profession as "microfinance" because of the size of the loans.

All customers require a co-signer and character references for loan approval, creating a circle of trust for lenders. All loans over $500 require guarantees and/or collateral. Interest rates start at 24 percent a year, plus fees. Loan interest rates vary depending on loan size, customers' credit, and other risk factors. Loan terms have ranged from 3 months to 3 years. For the Nicaraguan operations, the median loan term to date from the last 300 loans was 2.4 years.

Prisma has ongoing relationships with customers over the life of the loan. By maintaining contact with customers, early interventions save troubled loans. For example, the company offers customers in good standing (taxi owners in particular) additional working capital lines of credit. This ensures that their business is not disrupted due to cash flow crunches or unexpected occurrences including a car accident, a sick family member, or "inclement weather." Prisma also encourages evening out cash flows by requiring that customers put 5 percent of every loan into a savings account. For first-time borrowers, this amount is folded into the loan amount.

Borrowers in good standing, called class "A" customers, gain more latitude in available credit, which they use to restructure existing loans or get new ones. Customers increase their standard of living as a direct result of these loans.

Loan Products

- Micro Loans ($50-250)—primarily made to low-income individuals for consumer purchases and micro-entrepreneurs for business-related expenses. Micro loans are most often made to women. Business owners buy inventory and consumers purchase domestic appliances, such as refrigerators or stoves.

- Small Loans ($251-1,000)—primarily made to business owners. They purchase inventory and/or capital investments like machinery—freezers, sewing machines, or power tools.

- Medium Loans ($1,001-15,000)—primarily made to taxi owners to purchase new vehicles. These loans assist business owners graduating from small loans and growing owner-operated businesses seeking to expand. Extensive due diligence and more rigorous guarantees are required.

Sources of Revenue

LOAN REVENUE: The revenue stream from a loan is derived from three sources.

- Interest: A 24 percent annual rate is carried over the term of the loan. This rate is considerably lower than competitors' rates, which average at least 60 percent in the Nicaraguan microfinance industry. This revenue source accounts for 51 percent of Prisma's historical income.

- Legal Fee: A flat legal fee is charged for the origination of every loan, usually $30, which is carried over the life of the loan.

- Origination Fee: A 6 percent origination fee is charged that is carried over the life of the loan. This fee accounts for 7 percent of Prisma's historical income.

Additional revenue is derived from:

- Loan Late Payment Charges: Delinquent clients pay an extra 0.5 percent on the late balance. Almost 20 percent of the outstanding loans are assessed a late fee at some point during the life of the loan. But, at any one time, only 5 percent are in arrears. This revenue source accounts for 8 percent of Prisma's historical income.

- Savings Accounts: All clients are required to maintain a savings deposit with a balance of at least 5 percent of the amount borrowed. Prisma provides customers the initial 5 percent required in the loan itself. Savings accounts earn 8 percent annual interest. As this rate is on the high end of the market, the majority of customers carry at least a portion of their savings with Prisma. Savings account volume in Nicaraguan has been 5-10 percent of the total loan portfolio.

- Currency Exchange: Prisma conducts all operations in U.S. dollars because the local economies in which Prisma operates currently, and plans to operate in the future, are less stable. Operations in dollars minimize the currency risk and economic influences on the value of the portfolio. Loans are made and collected in dollars; however, the accounts for subsidiary operations must, by law, be carried on the books of the subsidiary companies in the local currency. On average, currency exchanges accounts for 15 percent of Prisma's historical net income.

- Automobile Insurance: This is a new product offering for Prisma; 50 policies have been sold since March 2000. Although it is a lucrative new offering, income is not realized for a policy sale until the end of the fiscal year. In fact, it is carried on the books as a liability. Offering insurance is a value added for several reasons. One, the company ensures that all cars it finances are insured. Two, competitive advantage lending to taxi drivers provides a captive market for the product. Last, profitably expanding services beyond just lending is a positive entry to offering additional products and services to customers that trust the company.

TARGET MARKET

Smart people are not confined to the developed world…. Any company that doesn't figureout a way to get connected with the poor [of the Third World] will not tap huge potential.

—Carly Fiorina, CEO, Hewlett-Packard

The Global Microfinance Market

Prisma MicroFinance, Inc., operates in the large, growing, yet underserved market of microfinance lending. The MicroCredit Virtual Library estimates that there are currently 7,000 microfinance institutions worldwide, serving approximately 16 million poor people. The total cash turnover for these institutions is $2.5 billion.

Of the estimated 500 million people who operate micro or small businesses around the world, only 10 million have access to financial support for their businesses (Source: Micro-credit Summit).

Worldwide demand for credit by this population is almost limitless. Based on an average loan size worldwide of $550, demand for microloans is approximately $270 billion. The annual growth rate of the world microloan portfolio is 30 percent, with some estimates as high as 70 percent (Source: Micro-credit Summit).

The spectacular growth rate of the microfinance industry is in large part due to the difficulty that the vast majority of people in the developing world face in gaining access to credit. The strict demands and cronyism of commercial banks makes it nearly impossible for an average citizen to get a loan.

Demand in Nicaragua

Prisma focuses its activities in the markets with which it is most familiar—Central America. With five years of profitable operations in Nicaragua, the company knows how to conduct successful business in these markets. Currently, the company operates in Managua, the capitol city of Nicaragua, and has made approximately 1,500 loans to date. Lending is limited only by the amount of capital available to lend.

Nicaragua is an attractive market for microfinance. Despite the American image of the country as economically volatile and politically unstable, Nicaragua has had open markets since 1990. In 1990, Nicaraguans elected as president Violetta Barrios de Chamorro who enacted market economy reforms in 1991, privatizing 351 state industries. The 1996 election of Arnoldo Alleman marked the continuation of government policies favoring a market economy. These policies remain in place today.

The economy largely consists of coffee, cereal grains, sesame, cotton, and bananas. Agriculture provides 34 percent of Nicaragua's GDP, the highest in Central America; however, over the past decade, there has been a shift in the workforce away from the agricultural sector toward urban, service sector jobs. Approximately 46 percent of the labor force is now employed in the service industry, compared to 28 percent in agriculture and 26 percent in manufacturing, construction, and mining. Nicaragua's major trading partner is the United States and its major exports are cotton, sugar, seafood, meat, and gold. Economic highlights about the country include:

- GDP of $2. 01 billion in 1998

- GDP per capita of $420

- Population of just over 4, 800,000

- Inflation rate consistently under 10 percent since 1994

The Nicaraguan Small Business Bureau estimates that the number of micro and small, nonagricultural businesses in Nicaragua is 152,607, excluding informal businesses, such as street hawkers and market vendors. Micro and small businesses are defined as having less than 5 employees. They employ 267,000 individuals, and are largely family-run enterprises. Informal businesses, typically a one-person operation, are estimated to be up to double those numbers. The government estimates that 60 percent of urban economic activity is conducted at the small, micro, or informal sector—a major driver of the local economy. With the average micro or small loan in Nicaragua estimated to be $585, based on industry data, this indicates an almost $300 million market in Nicaragua alone. The microfinance market, as a segment, is currently underserved. The total outstanding loan portfolio for Nicaraguan microfinance institutions is $47.9 million. Based on Prisma's experience, approximately 50 percent of all businesses in the country have access to some form of credit, either from formal institutions, family/friends, nonprofit microfinance lenders, or moneylenders. This number skews disproportionately to the larger companies, namely those with at least 20 employees or who are involved in export. Lending available to this population is at rates or terms less attractive than Prisma offers. Nonprofit lenders typically charge 60-80 percent APR, moneylenders are as high as 40 percent a month, and capital from family/friends is highly limited.

Within the large number of businesses operating in Nicaragua, there are numerous segments that are especially attractive for microfinance lending. Some unifying characteristics include:

Specific businesses that have been excellent customers to date include:

- taxi drivers: make daily or weekly payments and provide excellent collateral

- employee associations: act as an intermediary, thus improving the security of consumer loans

- community banks: increase the efficiency of servicing microloans

The Prisma target customer is a self-employed businessperson, either female or male, who lives in an urban area with his or her family. One of the most lucrative market segments Prisma loans to is taxi owners.

The Nicaraguan Microfinance Market

Although the countries in Central America are diverse, all have one thing in common: taxi cooperatives. There are more than 8,000 taxis operating in Nicaragua and the market is expanding. The Transportation Department estimates the number of new licenses granted will increase the total at least 10 percent a year for the next three years.

In Nicaragua, taxis are owner-operated and are considered medium-sized businesses. The owners are called "taxistas." They are organized nationally into 240 cooperatives. The cooperative structure gives the members bargaining power, purchasing power, and a strong social network.

In 2000, Prisma held about 2 percent of the taxi finance market within a fragmented market where no single competitor dominates. Taxi financing is a patchwork of banks, finance companies, car dealers, and other sources of informal financing. No financial institution has captured this market.

Expansion Strategy: Prisma will specialize in financing "taxistas" as a spearhead to establishing operations nationwide in Nicaragua and in other countries in Central America.

Prisma has made 250 loans to date to this population. Because the market is regulated through licenses, business is lucrative for the "taxistas" and loan repayment has been impeccable. Furthermore, in a recent Prisma survey of 80 drivers, 80 percent said they had or needed financing, whereas only half have existing access to financing.

Of the 3,200 "taxistas" who currently want financing, Prisma is positioned to capture the best of these clients, assuming the following:

- Prisma's 4-year track record of successfully working with taxi owner-operators will continue

- The average "taxista" loan to date of $5,993 for a term of 2.4 years is indicative of this market

- Any potential "taxistas" who are bad credit risks can be replaced because Prisma offers better credit terms

- A taxi is replaced every five years

This market segment is worth $11.52 million. For Prisma, further penetration into this market is currently limited only by capital. The Nicaraguan operations currently have 200 pending loans that have been approved, but there is not sufficient capital to lend.

Prisma will specialize in financing "taxistas" as a spearhead to establishing operations nationwide in Nicaragua and in other countries in Central America. Small, low overhead offices will be established in other urban centers. Strategic partnerships with a national bank and car dealers will enable Prisma to centralize lending and collections processes while still maintaining national coverage. This strategy coincides with market trends: new licenses are currently overwhelmingly granted outside the capitol.

Taxi owners are low-risk customers with excellent sources for collateral. They have the insured vehicle itself and an operating license that has value within the cooperative with which Prisma has outstanding relations. Moreover, the cooperatives must co-sign on a Prisma loan. This provides an important set of organizational incentives to re-pay loans. Finally, all taxi loans must be guaranteed by a lien on real-estate.

Serving this market segment is an excellent example of Prisma's double bottom line. Loans made by Prisma to "taxistas" serve independent business people while also placing large amounts of capital quickly and securely. A loan to this population enables a customer to have an annual income of approximately $1,000, almost twice the national average. Given that the average "taxista" has 6 dependents, Prisma's lending helps a huge number of people achieve a decent, although still precarious, standard of living. In this way, the Prisma social return, like the Prisma loan portfolio, is balanced: the emerging middle-class is encouraged while also supporting those on the economic margins.

Nicaraguan Competition

The total outstanding loan portfolio for Nicaraguan microfinance institutions is $47.9 million and Prisma currently has 1.2 percent of the market. Prisma's major competitors, in order of threat to the company, are:

- Other microfinance institutions

- Other formal lending institutions

- Money lenders

- Family/friends

- Potential customers not borrowing

Prisma is confident that its customer network is established enough to overcome the first three threats through word of mouth. In reverse order, here is an overview of each.

Potential Customers Not Borrowing: The most common action by potential customers at this time is not to access capital or credit, due to fear, lack of understanding, or no market opportunity. This dynamic clearly drags the economy in a number of ways, creating a significant dis-incentive for individuals to participate in the market economy.

Borrowing from Family and Friends: When individuals cannot turn to institutions, they turn to family and friends. On the practical level, this typically results in under-capitalization of potential successful businesses because family and friends are confronting the same dearth of capital.

Money Lenders: These are usually local individuals that lend money to people at interest rates that reflect their ability to provide capital quickly for their customers with limited focus on due diligence. Interest rates for this immediate access to capital are frequently as high as 480 percent APR. Prisma's significantly lower interest rates make it an attractive alternative to money lenders even if the turn-around on loan issuance is not immediate.

Other Formal Lending Institutions: There are a wide variety of formal lending institutions in Nicaragua who serve business owners. For the most part, these institutions would only be interested in Prisma's clients who take out the largest loans, namely the taxi cooperatives, because the others would be viewed as too risky. Prisma has a competitive advantage over formal lending institutions because it has been directly serving this target market for five years, knows the customers, and wants to serve them where the formal banks do not.

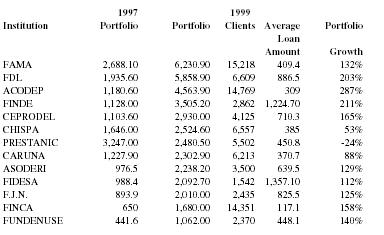

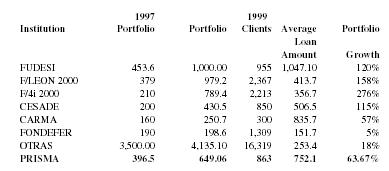

Other Microfinance Institutions: These institutions are Prisma's biggest threat. Many have as much experience as Prisma; however, their interest rates are much higher, hovering anywhere between 60-100 percent APR. Prisma's competitive advantage over these institutions is that its interest rates are considerably lower. Prisma is also a nimble company, with the ability to adapt its loans to the needs of the customer. Prisma is among the top twenty players in the Nicaraguan microfinance landscape, which controls at least 80 percent of the total market, the remainder of the market being served by money lenders. Even with this relatively small number of players in the market, it is still fragmented, with the largest organization controlling approximately 13 percent and the smallest less than 1 percent. The following table gives a breakdown of competitors' loan portfolios and growth.

Nicaraguan Microfinance Institutions: Portfolio and Client Data in Thousands of Dollars (Source: ASOMIF)

| 1997 | 1999 | ||||

| Institution | Portfolio | Portfolio | Clients | Average Loan Amount | Portfolio Growth |

| FAMA | 2,688.10 | 6,230.90 | 15,218 | 409.4 | 132% |

| FDL | 1,935.60 | 5,858.90 | 6,609 | 886.5 | 203% |

| ACODEP | 1,180.60 | 4,563.90 | 14,769 | 309 | 287% |

| FINDE | 1,128.00 | 3,505.20 | 2,862 | 1,224.70 | 211% |

| CEPRODEL | 1,103.60 | 2,930.00 | 4,125 | 710.3 | 165% |

| CHISPA | 1,646.00 | 2,524.60 | 6,557 | 385 | 53% |

| PRESTANIC | 3,247.00 | 2,480.50 | 5,502 | 450.8 | -24% |

| CARUNA | 1,227.90 | 2,302.90 | 6,213 | 370.7 | 88% |

| ASODERI | 976.5 | 2,238.20 | 3,500 | 639.5 | 129% |

| FIDESA | 988.4 | 2,092.70 | 1,542 | 1,357.10 | 112% |

| F.J.N. | 893.9 | 2,010.00 | 2,435 | 825.5 | 125% |

| FINCA | 650 | 1,680.00 | 14,351 | 117.1 | 158% |

| FUNDENUSE | 441.6 | 1,062.00 | 2,370 | 448.1 | 140% |

| 1997 | 1999 | ||||

| Institution | Portfolio | Portfolio | Clients | Average Loan Amount | Portfolio Growth |

| FUDESI | 453.6 | 1,000.00 | 955 | 1,047.10 | 120% |

| F/LEON 2000 | 379 | 979.2 | 2,367 | 413.7 | 158% |

| F/4i 2000 | 210 | 789.4 | 2,213 | 356.7 | 276% |

| CESADE | 200 | 430.5 | 850 | 506.5 | 115% |

| CARMA | 160 | 250.7 | 300 | 835.7 | 57% |

| FONDEFER | 190 | 198.6 | 1,309 | 151.7 | 5% |

| OTRAS | 3,500.00 | 4,135.10 | 16,319 | 253.4 | 18% |

| PRISMA | 396.5 | 649.06 | 863 | 752.1 | 63.67% |

Potential future competition: In this growing market, there are potential future competitors. Banks may move "down the line" to capture a portion of this market share, and direct competitors within Nicaragua may expand their operations. Prisma will draw on the relationships it has established throughout the Nicaraguan microfinance industry, its knowledge of government regulations, and its understanding of industry dynamics to preempt this competition.

Barriers to Entry

In-House Knowledge: Running a microfinance company requires extensive knowledge of banking, financial management, sales, and community outreach. A successful MFI needs a staff with a unique blend of skills. Prisma MicroFinance has attracted employees that bring these skills and has also spent time and energy on professional development. Organizations interested in starting a microfinance company will have to be dedicated to developing the requisite internal capacity as Prisma has done, and this can be costly and time consuming.

Staffing: Microfinance has been driven by nongovernmental agencies. As such, management and individuals working in the field usually come from a social service delivery background rather than a business background. However, microfinance is based on business fundamentals. Attracting individuals from the business sector has historically proven challenging because of the pay differential and lack of compensation incentives such as employment stock option plans. Prisma has already been able to attract staff from the business sector by offering competitive salaries; by converting to a for-profit stock company Prisma is now in a position to offer ESOPs, thus narrowing the differential between for-profit and nonprofit compensation packages. New ventures not in a position to do this will be hard pressed to attract employees with the skills necessary to run a successfully microfinance company.

OPERATIONS & MANAGEMENT

Management

The managers and directors have worked together since the beginning of operations in Nicaragua in 1995, boasting over 25 years of combined experience in the microfinance industry.

President, CEO, & Co-Founder: David J. Satterthwaite has six years of microfinance experience in Nicaragua and Latin America. David has also worked as a business consultant, researcher, and teaching assistant. He graduated with honors from Haverford College in Pennsylvania and is currently completing graduate work in Social Economy at Boston College.

General Manager (COO): Carlos Alberto Aburto Villalta has been responsible for Nicaraguan operations since 1998 and held previous management positions within the company prior to becoming COO. He holds a five-year undergraduate business degree from the Universidad Centro Americano (UCA) in Managua, Nicaragua, and is currently a candidate for a master's degree in business from the UCA.

Portfolio Manager: Honey Maria Aburto Villalta has been the loan portfolio manager since 1998. She holds a five-year undergraduate law degree from the Universidad Centro Americano (UCA) in Managua, Nicaragua, and is currently a candidate for her master's degree in labor law from the UCA.

Board of Directors

Roger Aburto: Co-founder of Prisma. Roger currently runs Xilonem, a cooperative spin-off from Prisma, which manages the insurance fund and past-due collections. Roger's experience includes: manager for a regional micro-credit fund for 8 years, a small-business owner, and a veteran. His education includes graduate work on the Nicaraguan informal economy.

Richard Burnes: Co-founder and Principle of Charles River Ventures (CRV is not associated with Prisma). Rick has been an investor in Prisma since its beginning in 1995.

George Kraus: As a retired entrepreneur, George supports a variety of humanitarian and business projects in Nicaragua. He has been an investor in Prisma since its beginning in 1995.

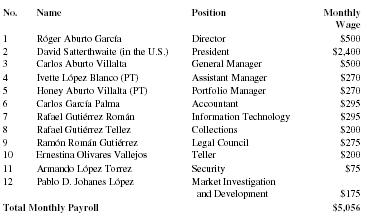

Staff

| No. | Name | Position | Monthly Wage |

| 1 | Róger Aburto García | Director | $500 |

| 2 | David Satterthwaite (in the U.S.) | President | $2,400 |

| 3 | Carlos Aburto Villalta | General Manager | $500 |

| 4 | Ivette López Blanco (PT) | Assistant Manager | $270 |

| 5 | Honey Aburto Villalta (PT) | Portfolio Manager | $270 |

| 6 | Carlos García Palma | Accountant | $295 |

| 7 | Rafael Gutiérrez Román | Information Technology | $295 |

| 8 | Rafael Gutiérrez Tellez | Collections | $200 |

| 9 | Ramón Román Gutiérrez | Legal Council | $275 |

| 10 | Ernestina Olivares Vallejos | Teller | $200 |

| 11 | Armando López Torrez | Security | $75 |

| 12 | Pablo D. Johanes López | Market Investigation and Development | $175 |

| Total Monthly Payroll | $5,056 | ||

Board of Advisors

Erica Mills, Master of Public Administration, marketing and communications consultant

Drew Tulchin, Master of Business Administration, business consultant

Brady Miller, former Director of Finance for Ex-Officio, finance consultant

Professional Staff

Nicaraguan Professionals:

Marco Morales, CPA

Oscar Silva, Legal Counsel, Delaney y Asociados

United States Professionals:

Tom Herman, Legal Counsel, Smith & Duggan, LLP

Howard Brady, CPA, MFI Consulting, Inc.

Daniel MacLeod, Graphic Designer, Visual Braille, Inc.

The Prisma Sales Experience

- Clients visit a Prisma office to request an application.

- Clients with strong references receive an application; careful track is kept of who receives them.

- If, upon review of the application by the Credit Committee, the customer is deemed to be an acceptable credit risk, preliminary approval is granted.

- A site visit is made to interview the customer, verify application details, and review collateral.

- Clients provide all necessary paperwork—including signatures and guarantees. The complexity of this process depends on loan size.

- Larger loans, including taxi loans, can take months because of the due diligence involved. It includes a police record review.

- The process is uniform and straightforward to ensure all customers receive the same treatment.

Operations

Prisma's operations and management has five years of successful, profitable lending experience in the Nicaraguan market. The company has developed successful activities for ensuring it is providing excellent service and developing strong relationships with solid customers, ensuring that the loans will be repaid.

Key Management Philosophy: Prisma conducts business in a highly professional and open manner. The company's philosophy is centered on knowing customers, working with them to be successful, making sure they understand how their loans work, and rewarding good behavior.

Streamlined Processing: Customers are classified from A-D based factors including: payment timeliness, credit history, savings, referring new business, and peer performance (those they referred or referred them). The taxi co-ops are classified according to the same criteria by each co-op as a group. There are rewards and tangible benefits for "A" customers, knowledge of which is spread among customers through word of mouth.

Balanced and Cost-effective Loan Portfolio: The existing relationship with Taxi Cooperatives provides an inroad for nationwide market penetration. A single loan officer covers the costs of his/her position with only 20 taxi loans (approximately $5,000 each). Microfinance industry data indicates loan officers can manage 150-300 loans at one time. Therefore, because the breakeven point for an additional lender is low, Prisma can financially afford to have a balanced portfolio with an equal number of micro and small loans. Although smaller loans are less lucrative, they are financially viable for the business and promote the social mission of ensuring there is access to credit for all. In addition, they provide the benefits of being repaid faster, requiring less due diligence, and producing a high number of referrals.

Hand-held Technology and Centralized Due Diligence: In order to minimize infrastructure costs, back-office support for loan officers will be centralized. Loan officers will utilize advanced technology to conduct their business. Hand-held devices will be used in the field to mechanize the application and monitoring process. The loan portfolio data is stored electronically to minimize onerous paperwork. This equipment investment pays for itself in the reduced paperwork, time savings (especially in approving applications and transferring data). Electronic loan processing and bi-weekly visits to the main office will allow the due-diligence of loan guarantees to be performed with adequate legal review, in a timely manner.

In addition to this technology, Prisma will also take advantage of technology being designed by groups like Hewlett Packard's World e-Inclusion team that is developing networked tools with the express purpose of making microlending more efficient. With a commitment of selling, leasing, or donating $1 billion in products and services to this initiative, it could prove a valuable source of technology enhancement.

Strategic Banking Partnership: To minimize expansion costs and accelerate the amount of lending possible, Prisma plans to partner with a bank with national presence. By utilizing their existing infrastructure and brokering the deals, remote offices avoid the complications of handling cash. This provides benefits in efficiency and also safety/security. Prisma has a developed a relationship with Banco de Finanza, a national leader in web-based delivery of banking services.

Vested Managers: A generous Employee Stock Option Plan creates a vested management team. Vested managers are important to providing motivation for the growth strategy. With these economic incentives for employees, Prisma has a competitive advantage compared to other microfinance lenders, including:

- nonprofits—unable to offer their managers a portion of the potential upside

- newly established stock companies controlled by directors from the nonprofit sector— unlikely to implement market-based incentives due to employee culture bias

GROWTH STRATEGY & MILESTONES

Growth Strategy

Prisma's market niche in taxi financing allows management to plan significant portfolio growth while minimizing overhead. Prisma will specialize in taxi financing as a spearhead to establishing operations nationwide in Nicaragua and in other countries in Central America. Using Prisma's specialization in taxi finance in this way drives penetration of the micro-credit market while still maintaining healthy profit margins.

In fiscal year 2002, Prisma will relocate its Managua office to prepare for national and international expansion. The new office space will accommodate the additional staff needed for expansion, while remaining in a geographically strategic location that will be convenient for Prisma's borrowers. In FY2003, the first satellite office in Nicaragua will be established, with two more additional national offices in FY2004. Also, in FY2004 Prisma will begin operating in a second country in Central America, to be determined depending on market opportunity.

Loan Officers: Prisma can realistically project rapid portfolio growth because of the proven demand for taxi financing and Prisma's track record financing taxis. Assuming that a single loan officer will manage 200 loans (a conservative estimate by industry standards), management estimates needing 25 loan officers by FY2004 when the total loan portfolio will be worth almost $11 million, distributed among 4,800 clients.

Scalability: Management forecasts steady profits for FY2001, although net income is projected to be slightly lower than FY2000 due to the integration of the U.S. operations. FY2002 will see a 100 percent growth in net income over FY2001, although management will advise reinvesting the profit into the company to support the growth strategy. Investment toward scalability during these two years will begin to pay off in FY2003, when management forecasts a 10.9 percent return on shareholder equity. Between FY2002 and FY2004, the portfolio balance per loan officer in order to break-even drops from an aggressive (but tenable) $470,000 down to $225,000 (total portfolio/total expenses). Securing the taxi financing niche and introducing operational improvements such as the use of hand-held technology makes the Prisma business model scalable.

Taxi Financing Market Share: Assuming that three-fourths of all medium-sized loans will be taxi loans and a 10 percent annual growth in the taxi sector, Prisma will claim a 22 percent market share by FY2004.

Central American Expansion: Nicaragua serves as a launch pad for entering the Central American market. In FY2004, Prisma plans to open operations in a second Central American country. This is a large and important market. (A Central American target market analysis can be found in the appendices.) The central challenge in expansion will be hiring effective management; for this reason, we are adopting a conservative expansion schedule. The taxi finance market will serve as a spearhead regardless of which country is deemed most appropriate.

Scalability Goal: Equity in Prisma is a long-term, non-liquid investment. The objective of achieving scale in the microfinance industry requires patient capital. "Scale" signifies at least the $50 million portfolio necessary to credibly solicit commercial capital investment. This will take 5-10 years. Scale is Prisma's mandate in order to be a leader in establishing new private equity capital markets for the microfinance industry.

Financial Return & Exit Strategy

The founders' choice in 1995 not to accept donations or subsidies to run this business was unheard of in the microfinance field at the time. However, since day one, Prisma has been dedicated to utilizing the essential potential of microfinance to eradicate poverty: making it economically attractive for capitalists to invest in "unbankable" business people. This choice has resulted in two truisms: private capital seeks scale to maximize profits and in order to achieve scale, equity is required. Therefore, consideration of the liquid event on this investment is imperative.

Because there are currently no secondary markets for Prisma stock and no one has yet to systematically "securitize" microloans, the most viable exit strategy for investors is acquisition.

Prisma has had discussions with major U.S. banks and has a clear understanding of what characteristics would be needed in order for an acquisition to occur. A national or international loan portfolio in taxi finance and a total loan portfolio of at least $50 million will make Prisma an attractive acquisition to larger banking institutions. These are the principal reasons that Prisma seeks to capture a niche market and grow its loan portfolio—to bring value to investors supporting micro-loans, which at present are unproven in secondary markets.

Financial Returns to Investors

First and foremost, Prisma is committed to providing its investors with dividends, even in the early stages of growth. Prisma has been profitable for five years, since its first day of operation. This proven viability legitimizes the plan of paying dividends. Management thinks it imprudent to forecast the value of dividends at this time. The financial projections indicate healthy profits in FY2003 and FY2004 of 10.9 percent and 11.5 percent respectively, once scale is achieved.

Moreover, Prisma seeks capital appreciation for its investors. Prisma anticipates that capital appreciation will be augmented in the future by the creation of business spin-offs and offering of additional products. Business spin-offs could include auto repair, auto parts, car insurance and collections. Additional products might be credit cards, mortgage financing, or home-improvement loans.

Social Returns to Investors

Like a bank, Prisma is a profitable lending business. But Prisma stands apart from its commercial counterparts for two reasons:

- it targets people without access to traditional, financial resources

- it is a business that realizes social as well as economic returns

Social returns constitute positive impact beyond the immediate benefits offered by a product —in this case small loans. Micro-lending is a business and development strategy widely acknowledged to bring extensive and diverse social returns to local communities. Well-managed, sustainable programs have been proven to successfully empower borrowers, strengthen families, catalyze communities, and expand local markets.

When an individual generates income from a small loan, the benefits extend a great distance and in many directions. Borrowers become more responsive to the needs of their families, and more active in their communities. Breadwinners are able to provide improved healthcare and education to their families, so children grow up healthier and with greater opportunities to realize their own potential. Families become stronger through access to working capital and the resulting opportunities. The fabric of communities becomes more tightly woven when it has a greater stake in its own development and can realize the benefits of its own efforts.

Prisma's clients and investors are able to realize tremendous social returns precisely because the company is profitable. Based on our estimates, every dollar lent generates $21 of social benefit for the borrower. For Prisma, profitability and sustainability are indicators that customers are using and repaying their loans successfully. This, in turn, means resources are more readily available for loans, and the social returns mentioned above go hand in hand with the unfettered availability and successful use of working capital.

Finally, as a market-driven social initiative, Prisma provides social returns at a larger scale with accelerated impact because it attracts investment.

MARKETING & SALES STRATEGY

Marketing Strategy

Because Prisma is mindful of the fiscal operations and expenses necessary to run a profitable enterprise, the marketing budget is, by design, small and highly focused on very basic, interpersonal efforts. Only those activities that provide proven return and bring in new loans to achieve the intended growth and projection figures are undertaken.

Grassroots marketing and establishing trust with customers has been the hallmark of the Nicaraguan operations to date. These efforts led to a 207 percent growth in Prisma's loan portfolio between 1996-2000. Ensuring positive customer experience has led to word of mouth as the leading source for new client acquisition. In a country like Nicaragua, where relationships and community are the mainstays of business activity, the "word on the street" is the best marketing channel and a strong indicator of a company's reputation. It is also inexpensive.

Other channels for publicity, especially formal channels including print media, television, and radio, will not yield sufficient response for their cost. The target customers are typically distrustful and skeptical of formal institutions, if not outright intimidated. Therefore, relationship marketing like face-to-face communication and rewarding referrals has a much larger impact, not to mention lower acquisition cost.

Marketing activities follow the same standards as operations, described earlier. This includes knowing customers, working with them to be successful, making sure they understand how their loans work, and rewarding good behavior. Customers are classified from A-D based factors including: payment timeliness, credit history, savings, referring new business, and peer performance (those they referred or referred them). The taxi co-ops are classified according to the same criteria by each co-op as a group. There are known rewards and tangible benefits for "A" customers—including better interest rates.

New loans are most easily made through the "chain of trust," whereby existing or old clients vouch (co-sign) for new customers. The practice of allowing "A" clients to co-sign, helping friends and family secure loans, provides Prisma with essentially a free sales force, minimizes default rates, and provides a support network to support struggling customers. Customers are highly loyal; they support the lending institution because they are supporting each other and helping themselves.

Promotional activities include simple and basic activities for existing customers and important members of the community including receptions, small gifts, and a newsletter. An annual reception is held to thank customers and share what the organization is doing. Customers feel valued and that they are contributing to economic development in their country. "A" clients receive little gifts on holidays. These gifts are inexpensive but customers appreciate them.

Marketing in New Markets

When entering a new market—first in other cities in Nicaragua and later in other Central American countries—the same tactics will be used. A major key to success is in effective new hires with strong professional and social networks that can share what Prisma does. Word of mouth is effective among family, friends, and the taxi co-operatives—all of which have connections in locations targeted for expansion and are just waiting for Prisma to establish operations there.

Indicators for measuring the success of marketing efforts is in how little money is spent to achieve Prisma's growth milestones. Customer satisfaction will remain the lynchpin of Prisma's marketing strategy.

Sales Strategy

As noted in previous sections, this enterprise is not starting from scratch. Prisma has five years of profitable operations upon which to base its sales activities. Most of the efforts will be on maintaining the current methods and practices that have made the company successful to date—lending to individuals in groups that know each other, providing excellent service, building trust with customers, and working with customers to ensure a successful loan.

The Nicaraguan operation has worked well with the taxi cooperatives. Since 80 percent of taxi drivers report requiring external funding to ensure they can operate successfully, this is a target market with very likely customers. Furthermore, most cannot or choose not to be served by more formal banks. Even better, the taxi cooperatives are close-knit business and social circles. Therefore, taxi drivers easily see what a loan from Prisma does for their business because a co-worker and friend has directly benefited from it. Drivers ensure their colleagues do not default on their loans because they are co-signers and do not want to lose this resource for affordable capital (and an "A" rating). In the event of a default, the entire cooperative could lose the lending service and the co-signers will be stuck with the bill.

FINANCIAL ANALYSIS

Capital Structure

Prisma's business model makes two assumptions:

- Equity capital is the only source of capital that will enable the company to achieve its expansion goals while maintaining a solid balance sheet.

- U.S. investors are looking to invest in companies that value social responsibility.

Prisma's five years of profitable operations confirms the first assumption. From its inception, Prisma has been financed through debt. Prisma has serviced these debts and remained profitable, but relying solely on debt capital has limited the company's growth as evidenced by the fact that Prisma has 200 approved loans waiting to be financed.

The New York Times' front-page article "On Wall Street, More Investors Push Social Goals," from February 11, 2001, bolsters the second assumption. Increasingly, investors are realizing that there "is a correlation between good practices and good investment results" and are placing their money accordingly. An analysis of "Socially Responsible Investing" proves that investors are increasingly adopting an investment approach that integrates social and environmental concerns into investment decisions. Prisma provides a viable option for investors interested in making money and making a difference.

Financial Projections

Prisma's fiscal year runs July 1 through June 30. The $1.5 million currently being raised in Series "B" round is scheduled to close in July 2001. Therefore, the equity appears in FY2002, beginning July 2001. During fiscal year 2001, the management established a U.S. office to raise funds and promote the company's activities. A central strategy is leveraging equity with additional debt to grow operations. In FY2002, a conservative leverage ratio of less than 1 to 1 is assumed; a similar ratio is also assumed in FY2003.

The $1.5 million of sought equity will fully impact revenue in FY2002. By FY2003, management projects a 10.9 percent return on $2.7 million in equity. By comparison, ROE for other financially self-sufficient microfinance institutions is 6.05 percent according to the MicroBanking Bulletin . Return on assets for these institutions hovers at 3.08 percent; by FY2004 management projects ROA of 4.1 percent. Throughout FY2002 and FY2003, investment in scaling operations is assumed. The goal is to achieve appropriate scale to secure another round of equity investment of $4 million in July of 2003 (beginning of FY2004).

Additional assumptions in the financials include:

- Interest Earned: As of FY2002, 17 percent net interest margin is assumed matching historical performance.

- Cost of Capital: 13 percent annual rate, based on current relationships with creditors and management's knowledge of the capital market for socially responsible investment instruments.

- Loan Officer Capacity: Each loan officer will manage 200 clients, which is low by industry standards.

- Taxes: Both U.S. and Nicaragua tax liabilities and expenses are included in the projections, assuming a combined rate of 35 percent.

IMPACT ANALYSIS & SOCIAL RETURN ON INVESTMENT

To claim that tangible assets should be measured and valued, while intangibles should not—or could not—is like stating that "things" are valuable, while "ideas" are not.

—Barach Lev, Professor Stern School of Business, New York University

Social Impact

Receiving a Prisma loan generates significant social impact in the following areas:

- Human Capital Development: Relates to improved economic standing, heightened self-esteem and sense of empowerment, and creation of a stable financial situation for borrowers

- Community Development: Resulting from borrowers' improved economic standing and ability to give back to the community

- Corporate Governance: Refers to the equity incentives that Prisma will offer to its employees and its ethic of empowering its staff through inclusive decision-making roles

- Socially Responsible Market Creation: Speaks to the industry-wide desired outcome of Prisma's activities, which is to be at the forefront of developing viable products to improve the situation of the world's four billion poor people, or the B2-4B revolution

Human Capital Development

Prisma's impact on human capital development results from the positive externalities generated by each dollar lent. The positive externalities start a ripple effect, which leads to improved diet as a result of having a stable cash flow and increased education level for borrowers' children who can stay in school rather than be forced to drop out to increase family income. Improvements to borrowers' lives can be seen in all areas of basic need as a result of having a higher standing of living.

Community Development

In addition to improving individual borrower's economic situation, Prisma's loans also fuel community development, which in essence is the aggregated effect of the individual loans. The loans improve the standing of individual borrowers, thus stabilizing economies at the community level.

The sense of empowerment that comes from economic stability also leads to greater community involvement. This involvement can take many forms, including being involved with public health projects such as latrine building, providing for community members who are sick or in a time of crisis, and skills transfer to other local business owners. These activities and interactions build healthy, sustainable communities.

Corporate Governance

Prisma is offering a balanced, inclusive equity structure that extends to every employee. Senior management is indigenous, except for David Satterthwaite, the CEO and President, who worked in Nicaragua for five years. There is local representation on the board, currently one third of the membership. Equity incentives in Latin America, including ESOPs, are far from the norm, especially for a small company. However, by doing so Prisma is promoting a new business culture of equitable private property ownership in an American company—this is globalization at its most positive.

Creating a commercial market that benefits poor people

According to Jeffrey Ashe, founder of Boston's Working Capital and former Vice-President of Accion International, there are approximately four billion people throughout the developing world without access to affordable credit. Entrepreneurs with excellent skills and incredible ideas are restricted in their opportunity due to lack of financial resources. Even the small amount of money needed as investment capital to start micro-enterprises like weaving baskets and selling them at the local market is beyond the grasp of the majority of the world's poor.

The world's "unbankable" populations have three options:

- gather limited resources from family and friends

- borrow from a moneylender at exorbitant rates

- turn to a microfinance institution like Prisma

Frequently, family and friends cannot generate the necessary capital and the moneylender's rates are too high to be able to pay them back. This being the case, only a loan from an institution like Prisma can result in the successful growth of a new business that may break the cycle of poverty.

According to industry sources, less than $10 billion currently is invested in the worldwide microfinance industry. This does not even scratch the surface towards serving this market. Microcredit is not a panacea solution for social problems. But, it is a useful tool for many to bridge the gap out of poverty and improve their lives. In addition to this activity providing a social return, there are equally compelling market driven motivations to undertake these operations using private capital—providing this service produces financial return.

As with any industry sector, once an example of a successful model is provided, others will enter the field. Following Prisma's lead, microfinance will become a viable commercial market, serving billions of the world's poor.

SROI Methodology and Analysis

While some of Prisma's Social Impact Areas are easily quantifiable, others are best evaluated in terms of qualitative impact analysis. Human Capital Development and Community Economic Development are included in the quantitative analysis using number of dollars lent as the unit of measurement. The qualitative methods analyze aspects of all four impact areas. The following sections outline Prisma's quantitative and qualitative methodology for measuring SROI.

Quantitative Analysis

Current SROI Analysis: In developing its quantitative methodology, Prisma has drawn from models developed by Roberts Endowed Development Fund (REDF), one of the leaders in social enterprise. The use of a social benefit/cost ratio, adjusted for present value, gives a clear sign as to whether the social benefits outweigh the social costs and by what degree. Based on traditional cost/benefit analysis benchmarks, if the ratio is greater than or equal to one, the project should be pursued.

SROI Ratio = Present Value of Social Benefits/Present Value of Social Costs

Social Benefits

Social benefits accounted for in the quantitative analysis of SROI include ripple effects from improving one's financial situations through receiving a loan. These include:

- Improved health for all family members, leading to higher productivity on a long-term basis

- Increased education for borrowers' children as they are not required to drop out of school in order to supplement the family's income

- Increased civic participation as a result of a heightened level of confidence and overall sense of self-worth

These benefits are cited extensively in microfinance literature, including by industry leaders such as FINCA and Accion International. The dollar amounts in the table below are taken from the financial projections for Prisma's loan portfolio. They represent the total number of dollars Prisma expects to lend in each year. (Social benefit and social cost are calculated on a per year basis and then aggregated.) As social benefits are directly correlated to loans, the social benefits are captured in terms of dollars lent to borrowers.

Social Costs

Prisma has always borrowed capital at market rates therefore eliminating the social cost of subsidies or grants often included as social costs in SROI analysis. We have included a small social cost that reflects loan loss due to Prisma's choice to make loans to extremely high-risk individuals. As the company's loan loss has historically been under 1 percent, the estimated social cost per dollar lent of $. 05 used in the model reflects our acknowledgment that in undertaking an expansion strategy into new geographic markets, we run the risk of an increase in the loan loss rate.

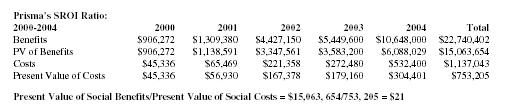

| Prisma's SROI ratio | ||||||

| 2000-2004 | 2000 | 2001 | 2002 | 2003 | 2004 | Total |

| Benefits | $906,272 | $1,309,380 | $4,427,150 | $5,449,600 | $10,648,000 | $22,740,402 |

| PV of Benefits | $906,272 | $1,138,591 | $3,347,561 | $3,583,200 | $6,088,029 | $15,063,654 |

| Costs | $45,336 | $65,469 | $221,358 | $272,480 | $532,400 | $1,137,043 |

| Present Value of Costs | $45,336 | $56,930 | $167,378 | $179,160 | $304,401 | $753,205 |

| Present Value of Social Benefits/Present Value of Social Costs = $15,063, 654/753, 205 = $21 | ||||||

A benefit/cost ratio of 21 means that for every unit of cost, 21 units of social benefit are derived. As the unit of measurement in this model is dollars, the social return is interpreted as $21 of social benefit for every $1 of social cost incurred. The fact that Prisma's SROI ratio is as high as 21 indicates that in terms of benefit/cost analysis, it is an attractive project, with an extremely high social return on investment.

Future SROI Analysis: Ideally, Prisma would quantify its SROI in terms of the increase in income derived directly from the loan. Measuring income generated specifically from a Prisma loan is complicated in that it would involve measuring a portion of each borrower's increase in income, rather than their total income. This approach would require an in-depth understanding of loan usage and the borrower's expenditures. Prisma proposes to develop this understanding through the qualitative methods described below.

A SROI analysis based on incremental increases in income would enable Prisma to project the increase per month in income over time. The company would then calculate the social net present value of that increase and calculate the appropriate social internal rate of return.

Qualitative Analysis

Prisma has historically collected some of the information described below, such as customer finances, professional activities, age, and gender. Based on its experience, Prisma believes the most effective way to gather information on a going forward basis is to administer questionnaires at the loan's beginning, closing, and annually thereafter (on a voluntary basis), in conjunction with qualitative interviews. These new methods will standardize the process of information gathering and enable Prisma to do more rigorous quantitative analysis, in addition to maintaining a clear sense of its customer base—even as it rapidly expands. Information gathered from customers will include both economic and social indicators.

Economic Indicators

As a bank, Prisma must make loans that are fiscally responsible and will be paid back. Therefore, it needs to determine a borrower's financial status before, during, and at the end of the loan. During the loan application process, loan officers will collect information about customers and their finances, including their professional activities, income, historical income, family financial resources, and projected future income. This builds on the information Prisma currently collects and believes is reasonable to collect in the future.

Social Indicators

Because of the level of trust Prisma staff establishes with customers, they have been consistently helpful in providing information enabling us to track their status. At the time of the loan, social indicators including age, gender, economic condition of borrower, number of family members, and current income are provided. Throughout the term of the loan, it is easy to track the number of employees, business income, and changes in standard of living. This is done implicitly by following the timeliness of loan payments and seeing if loan payments are made on time or late. Receipt of late payments usually indicates a change for the worse in the borrower's status. Prisma will also begin using a standardized method for tracking the ongoing conversations Prisma staff has with customers, through which much information about social indicators is gathered. At the end of the loan, the same information will be formally gathered with an exit questionnaire. Plus, because of its active involvement in the communities it serves and the fact that many customers renew loans for additional working capital, Prisma will be able to track social indicators longitudinally.

Information gathered through loan review, questionnaires, and interviews will be included in Prisma's Annual Report. This will enable our investors to track the SROI and ensure that Prisma stays true to its mandate of doing well by doing good.

If we are looking for one single action which will enable the poor to overcome their poverty, I would focus on credit.

—Dr. Muhammad Yunus

Founder, The Grameen Bank

APPENDIX

Target Market— Microfinance in Central America

Market Description

Prisma MicroFinance, Inc., is a U.S. microfinance company with Nicaraguan operations where loans are made to residents in the urban area of capitol, Managua. The loans range in size from U.S. $50-$15,000, and are used for both personal and business purposes. Loans to taxi cab cooperatives account for the larger loans and act as a subsidy for the smaller loans to individuals, primarily women.

Market Size and Trends

Managua is Nicaragua's economic center and has a population of more than 1,000,000. Although Nicaragua's economy is still driven by agriculture, service jobs in the urban areas represent an increasing number of jobs.

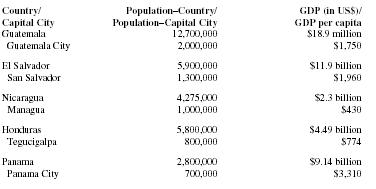

This trend holds true throughout Central America. The table below demonstrates the size of the market for international microfinance in Central America's urban areas—the geographic areas that Prisma will target as it expands—expressed in terms of population and GDP. The countries are ranked by size of capital city, beginning with the largest, Guatemala City.

| Country/Capital City | Population–Country/Population–Capital City | GDP (in US$)/GDP per capita |

| Guatemala | 12,700,000 | $18.9 million |

| Guatemala City | 2,000,000 | $1,750 |

| El Salvador | 5,900,000 | $11.9 billion |

| San Salvador | 1,300,000 | $1,960 |

| Nicaragua | 4,275,000 | $2.3 billion |

| Managua | 1,000,000 | $430 |

| Honduras | 5,800,000 | $4.49 billion |

| Tegucigalpa | 800,000 | $774 |

| Panama | 2,800,000 | $9.14 billion |

| Panama City | 700,000 | $3,310 |

| Costa Rica | 3,700,000 | $5 billion |

| San Jose | 330,000 | $1,351 |

| Belize | 250,000 | $700 million |

| Belize City | 55,000 | $3,000 |

Many Central American countries are rebuilding after years of political, social, and economic unrest. Microentrepreneurs play an integral role as economic drivers in this rebuilding and will need access to affordable capital.

Target Customers

Prisma's target customers include:

- Taxi cab drivers

- Microentrepreneurs

- Women

These target customers look for microfinance institutions (MFIs) that are professional, while still understanding the specific needs of poorer borrowers. They would not have access to banks or traditional financial institutions, so if they decide to take out a loan their options are limited to friends/family, moneylenders, or MFIs. The resources of friends and family are extremely limited, and the exorbitant rates charged by moneylenders (ranging from 360-480 percent APR) make them unattractive in terms of repayment possibilities. (Moneylenders are attractive because there are no conditions to qualify for a loan.) Prisma is in competition with other MFIs.

Market Readiness

Prisma has been in operation for six years. In each of these six years, it has expanded its outreach and refined its operations. With a strong management team in place, Prisma is now ready to significantly expand its operations. It is already the market leader for lending to taxi cab cooperatives and plans to make this its market niche over the next year. This will position Prisma to expand its outreach to other microentrepreneurs and individuals, particularly women.

Strategic Opportunities

Through its experience in the Managua area, Prisma has learned that there is a significant demand for microloans. With its economy continuing to grow, this demand will only increase.

Other capitol cities throughout Central America are experiencing a similar shift toward an expansion of economic activity in the urban centers. The need for microentrepreneurs to access affordable capital will expand along with the urban-based economies. Clearly, there is a demand for reputable MFIs to meet this need and Prisma has established a way to reach this market.

Comment about this article, ask questions, or add new information about this topic: