CALL AND PUT OPTIONS

An option is a financial instrument that gives its holder the choice of purchasing (call option) or selling (put option) an underlying security at a predetermined price. Most options are for limited periods, so the choice must be exercised before the option expires.

The security on which the option is written is known as the underlying security. The price that the option purchaser must pay to exercise the option is known as the exercise price or strike price. Strike prices are adjusted for stock splits and dividends, but not cash dividends. The expiration date is the last date on which the option may be exercised. An American option may be exercised at any time up to and including the expiration date. A European option can be exercised only at the expiration date.

An option is said to be "in-the-money" if by exercising the option it would produce a gain. Call options are in-the-money when the market price of the underlying security is greater than the exercise price. Put options are in-the-money when the market price of the underlying security is less than the exercise price. Call options are said to be "out-of-the-money" when the exercise price is more than the market price of underlying security. Puts are out-of-the-money when the market price of the underlying security is more than the exercise price.

The following discussion of options will use a call option as the example. Everything stated, however, also holds for puts—the reader should keep in mind that the transaction is reversed.

A typical call option may be written to give its buyer the option to purchase 100 shares of the PDQ Corporation at a price of $60 per share before a stated expiration date. The writer (i.e., seller) of the option will receive a premium for writing the option. The per share premium is the option price divided by the number of shares in the option. (While most premiums are quoted on a per share basis, options are generally written for 100 shares.) The purchaser of a call option hopes that either (1) the price of the underlying security will increase beyond the exercise price plus the cost of the option, thereby making exercise profitable; or (2) the premium on the option increases, thereby making sale of the option profitable.

Both buying and selling options offer profit opportunities. Buyers of call options have the following advantages:

- They know in advance the price they are going to pay (i.e., the exercise price).

- They know in advance the maximum loss they can sustain on the option if they choose not to exercise (i.e., the cost of the option).

- They have the opportunity to benefit from the extreme amount of leverage implicit in most options.

Advantages to the seller include an opportunity to increase income from the underlying security in the option. For example, assume a portfolio contains some stock , the price of which is drifting around a certain market price. The investor could write an option against that stock and generate a profit, to the extent of the premium in the option, thereby gaining even though the stock's price has not moved.

Sellers who write options against securities held in their portfolios are said to be selling covered options. Options written without the underlying security in the writer's portfolio are known as naked options. Writers of naked options must have adequate funds on deposit with their broker to cover the options, should they be exercised.

The premium related to the option is pivotal to options trading. The lower the premium, the more favorable the option is to the purchaser for two reasons: (1) the purchaser can hope to subsequently sell the option at a higher premium, or (2) if the market price of the underlying security rises above the exercise price of the option, the purchaser can always exercise the option, thereby acquiring the security from the option writer at below the security's current market value.

For example, assume an option for 100 shares is purchased for $200 (premium of $2 per share) while a stock is selling at $30 per share and the exercise price is $35. If the price of the stock rises to $38, the option price should rise to at least $3 ($38 - $35), and more likely will rise close to $5 [($38 - $35) + $2]. If the price of this option rises to $3, the holder can either sell the option and realize a profit of $100 (a 50 percent profit margin), or the holder can exercise the option, purchasing the shares for $3,500 instead of $3,800.

FACTORS AFFECTING OPTION PRICE

There are several factors that affect the amount of an option's premium. The premium will be a reflection of demand and supply. During periods of rising stock market prices, there is an increased interest in purchasing options. Conversely, individuals owning securities would be less interested in writing options, opting to hold their stock for further price appreciation. The combination of these two typically raises the level of option premiums. When stock prices are declining, there is greater interest in writing call options but less in buying them; premiums thus tend to decline.

In addition, there are at least four other factors that interact to influence the level, and movement, of call option premiums:

THE CURRENT MARKET PRICE OF THE STOCK.

Whenever the option is in-the-money, the option price will rise if the price of the stock continues to rise, since the option has value in addition to the time-lock inherent in every option.

TIME.

Everything else remaining equal, the more time remaining until the option's expiration date, the higher its premium will be. This only makes sense, since the longer an option has to run, the less risk there is to the option holder that the exercise price will not rise to a level to make the option profitable. As the option approaches its expiration date, its time value declines, and near expiration, its only value will be the excess, if any, of the underlying security's market price over the exercise price.

It is because of the time value that it is likely an option will still have market value even though its exercise price plus premium is below the market value of the underlying security.

VOLATILITY.

If the price of the underlying security fluctuates substantially, the option is likely to command a heftier premium than an option for a security that normally trades in a narrow price range. As a general rule, call option premiums neither increase nor decrease point for point with the price of the underlying security. That is, a one point increase in the underlying security price commonly results in less than a one point increase in the call option premium. Reasons for this include:

- Rising premiums reduce the leverage inherent in the option. For example, if the price of a stock is $100 and the option is $10, the buyer's leverage is 10:1. But if a $1 increase in the stock price were to raise the option premium by the same amount, the leverage would be reduced.

- A rise in the stock price increases the buyer's capital outlay and risk. For example, an increase in stock price from $50 to $51 is only 2 percent, but a rise in option premium from $5 to $6 is a 20 percent increase.

- Assuming the underlying security has been in an upward trend, the option will have less time value, decreasing its attractiveness.

THE RISK-FREE RATE OF RETURN.

This action of the variable is not as clear. Since increasing interest rates tend to depress stock prices, this should also cause call option prices to decrease and put option prices to increase. On the other hand, if you choose to acquire the underlying stock, instead of an option, the cost to finance the purchase would increase if the risk-free interest rate increases. Therefore, the call option would be preferred over a purchase, since the only cash outflow would be the cost of the premium.

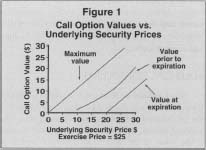

As a result of the interaction of these variables, an in-the-money call option's price will be at least equal to the difference between the market price and the exercise price of the underlying security. If the underlying security's market price is near zero, it is conceivable that the option will be worthless. Therefore, the minimum price of an option is zero. Its maximum price will equal this difference plus the algebraic sum of the value of the above factors, limited by the market price of the security. An out-of-the-money call option's price will be a function of just the above factors. Note that as the expiration date of the option nears, the effects of these other factors are significantly diminished. The figure illustrates these relationships.

In recent years, most analysts have been using the Black-Scholes model for the valuation of options. This model is designed for European options and is mathematically complex. Several software packages, however, have been developed, which makes its application considerably easier. As a result, it has gained widespread acceptance.

BUYERS' STRATEGIES

One of the main advantages of purchasing a call option is to have a security with mega-leverage. For example, going back to the earlier case, assume an option is written for a stock selling at $30. The option's exercise price is $35 and the option is selling for $2. Consider two investors with $3,000 to invest:

- Investor A purchases 100 shares of stock and investor B purchases 1500 options. If the price of the stock rises to $38, the investor in the stock will have a profit of $800 ($3,800 - $3,000), or 26.7 percent. Assuming the options rise in price to $3 ($38 —. $35), and, it is likely the price will be higher, Investor B realizes a profit of $1,500($4,500 - $3,000), or 50 percent.

The call option purchaser also has the benefit of limited risk. Should the price of the underlying security decline, the option holder's maximum loss is always the price paid for the option (i.e., his total investment in the option).

A holder of an American call option can always exercise the option before the expiration date. This is done only when the market value of the underlying security is above the exercise price of the option. Because the commissions to sell an option, however, are less than the commissions to both buy and sell the underlying security, most option holders prefer to simply sell the option rather than exercise it. Should the option be exercised, the Options Clearing House randomly selects a member with an outstanding short position in the same option to conclude the transaction.

Another strategy for call options, assuming the holder believes there will be a rising market and wishes to purchase the underlying security in the future, is to lock in the price of the underlying security. This is especially useful if the investor anticipates cash flow in the future to pay for the purchase.

A final strategy for which call options are used is to hedge against a short sale since the option establishes the maximum price that will have to be paid for a security in order to satisfy the obligation of a short sale.

Lastly, should an investor sell a stock at a loss, buying a call option within the 30-day period before and after the sale would constitute a wash sale and result in the loss being disallowed for income tax purposes.

SELLERS' STRATEGIES

Assume an owner of 100 shares of stock that cost $50 a share can write an option at a premium of $5 per share. The stock would be deposited with the writer's broker and his account would be credited for $500. Note that the $500 belongs to the writer whether or not the option is exercised. It is erroneous, therefore, to think of the premium as a "down payment."

If the exercise price is below the market value of the security as the expiration date is approached, option writers can reasonably assume an option will be exercised and they will have to deliver the underlying security. Note that writers can always terminate their obligation to deliver the security by simply purchasing an identical option at the current premium, thereby liquidating their position.

[ Ronald M. Horwitz ]

FURTHER READING:

Brigham, Eugene F., Louis C. Gapenski, and Michael C. Ehrhardt. Financial Management: Theory and Practice. 9th ed. Fort Worth, TX: Dryden Press, 1999.

Hull, John C. Options, Futures, and Other Derivatives. 3rd ed. Upper Saddle River, NJ: Prentice Hall, 1997.

Kolb, Robert W. Understanding Options. New York: Wiley, 1995.

Wilson, Thomas E., and others. "Valuing Stock Options: A Cost-Effective Spreadsheet Template." CPA Journal 65, no. 3 (March 1995): 50.

Comment about this article, ask questions, or add new information about this topic: