RETAIL TRADE

Retailing is the sector of the economy that offers goods and services for sale directly to the ultimate consumers, usually private individuals. It is related to wholesale trade, which is the purchase of goods or services in bulk by businesses or persons who may add something to those goods or services, or use them in production. Wholesalers usually do not deal directly with the end user.

By definition, retailers are primarily marketing and distribution organizations. In conventional merchandise retailing, they typically provide a conduit between a host of companies that specialize in producing goods and consumers who require those goods all at one site, the store. For more service-oriented retail operations, e.g., restaurants, the supplier relationship is somewhat different, but many of the same market dynamics still hold. As such, retailers are only effective to the degree they create convenience and value—broadly defined—for both customers and suppliers. In an era when some manufacturers would just as soon use the Internet to reach their markets directly—and do—retailers must redouble their efforts to create compelling value propositions and other enticements for customers. These may take the form of low prices, innovative product/service mixes, rewarding shopping experiences, customer perks, or any number of other marketing strategies.

ORGANIZATIONAL AND STATISTICAL

PORTRAIT

The retail industry represents a major component of industrial, market based economies. In the United States, retailing consistently employed around one-fifth of the labor force, or well over 22 million workers, as of 1999. In 1998, U.S. retail trade was worth nearly $2.7 trillion in annual sales. However, sales growth at the aggregate level has been fairly slow in this mostly mature sector, and profit margins in many retail categories tend to be very thin. Adjusting for inflation, the entire retail sector's sales grew by less than 14 percent for the nine year period of 1990-98. Indeed, a boom year for retailers is 5 or 6 percent growth—a rate that in the high-tech sectors would cause investors to frantically liquidate their shares.

Retail trade has always been an important factor in the nation's economy and credit outlook. Retailers purchase items for sale with no guarantee of selling them, often borrowing large sums to make the goods available to customers. Customers, in turn, often purchase items on credit, using store or national credit cards.

RETAIL CATEGORIES

There are more than one million retail companies in the United States. For statistical and market analysis purposes, these retailers are usually categorized by what they sell. Using classification systems such as the Standard Industrial Classification (SIC) or the newer North American Industry Classification System (NAICS), the Census Bureau groups these establishments according to their principal merchandise line—the line that accounts for the largest share of store sales. Thus in general studies, a store such as Kmart which carries furniture, but sells far more clothing, might have its furniture sales reported under the principal line, clothing. This is, of course, a distortion, and professional analysts often seek to separate sales by each product line in order to create a more accurate profile.

The most general statistical categories for retailing are durable and nondurable goods. The conventional distinction between them is that durable goods are expected to have a life span of one year or more, whereas nondurables last less than a year (though this is not literally true in all cases). Durable goods include items like home appliances, electronics, furniture, motor vehicles, and so forth. Examples of nondurables include food, pharmaceuticals, toiletries, and paper products. Nondurable goods as a whole tend to be the larger sales category; as of 1998 nondurables represented 58 percent of retail sales compared to 42 percent for durables.

NONSTORE RETAILING.

Retailers are also classified by whether or not they sell their wares in physical stores. While the vast majority do sell at physical outlets, nonstore retailing in the United States is a robust $80 billion industry—and one that has been growing more than twice as fast as conventional retailing. Net nonstore sales growth from 1990 to 1998 was in excess of 35 percent after inflation. Mail order services make up 70 percent of nonstore retailing by sales volume, although the category also includes vending machine operators and direct selling businesses (e.g., telemarketing, door-to-door).

E-COMMERCE.

The latest form of nonstore retailing is over the Internet and World Wide Web. In electronic commerce, or e-commerce, the distinction between retailers and manufacturers (or even wholesalers) can be minimal to the end user. Behind the interface the differences remain, for electronic retailers still aggregate merchandise that others produce and market it to end users. But here, in theory at least, the added costs of having a middleman can be more apparent to consumers and, with consumers having equally convenient access to both retailer and manufacturer, place retailers at a competitive disadvantage. In practice, thus far at least, manufacturers have tended not to compete with retailers on price. In fact, many retailers on the Internet offer better prices than the producer does, for example, in packaged software sales, because software vendors tend to sell their products only at list price, whereas e-commerce retailers may offer discounts.

The importance of the electronic marketplace over the long run cannot be understated. A major study released in 1999 by two University of Texas economists indicated that the economic value of Internet-related activity was worth some $302 billion in 1998. Of this amount, $102 billion came from e-commerce, a level consistent with other analysts' estimates. While much of this was business-to-business trade, and technically outside the scope of retailing by conventional definition, consumer online purchases were reckoned at more than $10 billion by other researchers. In another gauge of consumer Internet commerce, some analysts estimated that during the 1998 holiday shopping season 8.5 million households bought gift items over the Internet, a more than fourfold increase from a year earlier.

HISTORY AND TRENDS

In the late 18th century in Europe, and slightly later in the United States, the mix of ample goods and enough people with disposable income to purchase those goods reached the critical mass needed to fuel the rise of a merchant class and a multitude of shops. Colonial American towns were lined with shops where the purchase of goods and the exchange of social niceties was a way of life. Frontier settlers were treated to "portable" stores in the form of peddler wagons until enough people lived in one area to support a store. This pattern continued well into the 20th century with a cluster of stores downtown that sold many goods, and a few food and general merchandise stores in the neighborhoods.

In the 1960s, retailing began to take on a new face. Retailers followed their customers to the suburbs with an array of strip malls; then in the 1970s and 1980s giant indoor shopping malls; and in the 1990s, the return of the strip mall and the emergence of the electronic shopping place.

One of the most pervasive U.S. retail trends over the second half of the 20th century was consolidation and the rise of large chain stores to replace smaller, local ones. This occurred perhaps earliest in the grocery store arena with the so-called supermarket revolution, extending roughly from the 1950s to the 1970s, which drove many smaller, independent grocery sellers out of business. A parallel movement that originated in the same period was the rise of the so-called category killer, epitomized by stores such as Toys 'R' Us, Inc. First appearing in the 1950s, Toys 'R' Us offered a very wide selection of items in its market category and sometimes at lower prices than smaller retailers. In theory, the category killer exhausted consumers' need to shop around for a particular item of interest because one store carried nearly everything.

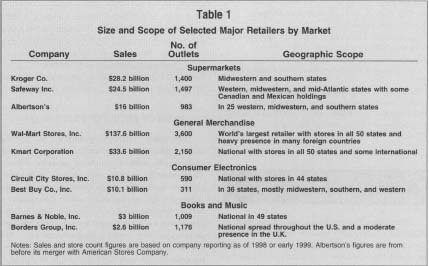

Both consolidation and the growth of large-format chain stores continued and in many retail segments accelerated in the 1980s and 1990s. The category killer or "superstore" format was adopted in such diverse areas as hardware and home repair, office supplies, consumer electronics, and books. At the same time, mergers and acquisitions were a regular feature on the retail landscape, with a handful of stores in each category competing for market share as the top-tier national and superregional chains. Table I compares the size and geographic scope of some of the leading chains in several retail categories.

Retailing is highly competitive and large discount chains and specialty retailers alike compete aggressively for consumer dollars. As an example, food retailing has witnessed the discount/warehouse wars, enticing customers to buy in bulk at a discount. Retailers have sought to tailor their methods to reach consumers who are increasingly short of time, looking to get the best buy for their dollar, and demanding superior customer service.

At the same time, the very act of shopping has undergone change in a number of ways. Shopping is increasingly viewed as a utilitarian task, and the once-vaunted suburban shopping malls have actually experienced declining sales net of inflation. In women's retailing, where the traditional store concept is most alive, inroads have been made by electronic shopping, shopping in catalogs, and shopping by television and phone—all time-saving efforts.

Part of the reason for these changes in retailing is that the demographics of the U.S. market changed significantly in the last quarter of the 20th century. Single-parent families, dual-income families, and smaller families are just a few of the socioeconomic trends influencing retail markets. Cultural diversity and tolerance have also greatly affected the sector. Recognizing a diversified market, many retailers now target their ad campaigns to segments of the market once ignored. There have been, for example, campaigns for larger-sized women's clothing, ads targeted specifically toward Hispanics or African Americans, and the plethora of media efforts to gain the dollars of the fickle but lucrative teen market.

Size and Scope of Selected Major Retailers by Market

| Company | Sales | No. of Outlets | Geographic Scope |

| Supermarkets | |||

| Kroger Co. | $28.2 billion | 1,400 | Midwestern and southern states |

| Safeway Inc. | $24.5 billion | 1,497 | Western, midwestern, and mid-Atlantic states with some Canadian and Mexican holdings |

| Albertson's | $16 billion | 983 | In 25 western, midwestern, and southern states |

| General Merchandise | |||

| Wal-Mart Stores, Inc. | $137.6 billion | 3,600 | World's largest retailer with stores in all 50 states and heavy presence in many foreign countries |

| Kmart Corporation | $33.6 billion | 2,150 | National with stores in all 50 states and some international |

| Consumer Electronics | |||

| Circuit City Stores, Inc. | $10.8 billion | 590 | National with stores in 44 states |

| Best Buy Co., Inc. | $10.1 billion | 311 | In 36 states, mostly midwestern, southern, and western |

| Books and Music | |||

| Barnes & Noble, Inc. | $3 billion | 1,009 | National in 49 states |

| Borders Group, Inc. | $2.6 billion | 1,176 | National spread throughout the U.S. and a moderate presence in the U.K. |

| Notes: Sales and store count figures are based on company reporting as of 1998 or early 1999. Albertson's figures are from before its merger with American Stores Company | |||

On the management side of retailing, three important themes have been: (1) inventory control and other forms of cost control to improve profitability and cash flow; (2) related efficiencies gained from electronic ordering and management, such as reducing paperwork and inaccuracies; and (3) strategic relationships with vendors to control source costs and implement high-tech supply chain management.

RETAIL THEORY AND PUBLICATIONS

As in most major economic sectors, there is a strong body of literature and theories covering the methods and processes used in corporate retailing. Several academic and trade journals exist for retailing in general, as well as for specific segments, such as supermarkets, drug stores, or apparel stores. Topics addressed include pricing theory, business philosophy and strategy, consumer behavior, innovative practices, and current trends and issues facing the industry.

EMPLOYMENT PROFILE

Employment prospects in the retail store sector have always been most abundant in sales, and the majority of that workforce has been, traditionally, female. Sales persons, one of the industry's largest occupational groups, represent approximately 20 percent of the retail workforce, and cashiers make up an additional 15 percent. Each of these categories was expected to add several hundred thousand new positions in the United States over the period 1996-2006, according to Bureau of Labor Statistics projections. In fact, cashier positions were expected to be the single largest occupational growth category in terms of the number of new jobs added.

Despite the copious job openings in these areas of retailing, they are mostly unskilled and relatively low-paying positions, at least until workers reach management level. Approximately two of every five retail sales employees were part-time workers. This is significant because many part-time workers do not earn pension or health benefits. In addition, the use of many part-time workers means that merchants do not have to pay overtime to stay open seven days a week.

The retail corporate staff also includes buyers (usually college educated), financial managers, human resource specialists, finance and accounting staff, advertising and marketing personnel, and display specialists.

To prepare for careers in retail management, many colleges and universities offer associate and bachelor degrees in retail-related studies. A few offer advanced degrees, most notably the University of Arizona, which has a doctoral program. Common academic specializations include retail marketing, merchandising, and retail management.

FURTHER READING:

Berman, Barry, and Joel R. Evans. Retail Management: A Strategic Approach. Upper Saddle River, NJ: Prentice Hall, 1998.

"Key Success Factors from Leading Retailers." International Journal of Retail & Distribution Management, June-July 1997.

Levy, Michael, and Barton A Weitz. Retail Management. Chicago: Richard Irwin, 1998.

National Retail Federation. National Retail Federation: The World's Largest Retail Trade Association. Washington, 1999. Available from www.nrf.com .

"Report Quantifies Economic Impact of U.S. Internet-Related Companies." Wall Street Journal, 10 June 1999.

Reynolds, Jonathan. "Retailing on the Net." International Journal of Retail & Distribution Management, February-March 1999.

U.S. Bureau of Labor Statistics. Occupational Outlook. Washington: GPO, biannual. Available from www.bls.gov . Wakefield, Kirk L., and Julie Baker. "Excitement at the Mall: Determinants and Effects on Shopping Response." Journal of Retailing, winter 1998.

Comment about this article, ask questions, or add new information about this topic: