SIC 2436

SOFTWOOD VENEER AND PLYWOOD

This classification includes establishments primarily engaged in producing commercial softwood veneer and plywood from veneer produced in the same establishment or from purchased veneer. Establishments primarily engaged in producing commercial hardwood veneer and plywood are classified elsewhere in SIC 2435: Hardwood Veneer and Plywood. Establishments primarily engaged in the production of veneer used in the same establishment for the manufacture of wood containers such as fruit and vegetable baskets and wood boxes are classified elsewhere in various wood container manufacturing industries.

NAICS Code(s)

321212 (Softwood Veneer and Plywood Manufacturing)

Plywood was first developed in 1905 in St. John, Oregon. Plywood comes in different grades depending on the quality of surfaces and the type of adhesive.

Softwood veneer is made by cross-laminating veneers, such as pine, spruce, fir, and hemlock. The grains are placed at right angles to improve strength; panels are made in 4-by-8 foot sizes, with a thickness up to three-quarters of an inch. Veneers are bonded together using a waterproof or moisture-resistant adhesive.

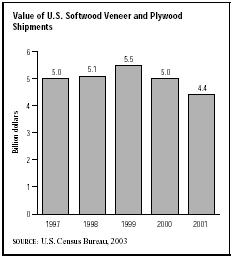

The Bureau of the Census reported the value of output for the plywood and veneer (softwood) manufacturing industry as $4.4 billion for 2001. The demand for veneer and plywood depends on the construction industry. Nearly 48 percent of veneer and plywood output goes to construction, mainly residential. Roughly 25 percent of the output is used in other lumber and wood products industries, with an additional 11 percent in furniture and fixtures. Rough softwood plywood accounts for more than 50 percent of total product shipments, followed by sanded softwood plywood and nonreinforced softwood veneer at 15 percent and 13 percent, respectively.

As with other construction material producing industries, this industry suffered during the economic recession of 1990 to 1991, but it benefited tremendously from the surge in housing construction at the end of 1993. Growth continued until 1996, when shipments dropped back to 1993 levels. In 1997, product shipments increased by 1 percent to about five billion dollars compared to the previous year, which was again attributed to healthy housing starts. Due in part to the strengthening U.S. economy, shipments increased to $5.15 billion in 1998 and to $5.56 billion in 1999. However, when the U.S. economy weakened in 2000, shipments declined to five billion dollars that year and to $4.4 billion in 2001. Increased housing starts in the early 2000s were expected to bolster shipments values.

Competition continues to increase from the Oriented Strand Board (OSB) industry since this product's average price is around 20 percent lower than plywood due to the simpler manufacturing process. In 1998, OSB owned more than 50 percent of the North American sheathing market. This figure had grown another 25 percent by 2003, according to a November 2003 issue of Home Channel News . "OSB has eclipsed plywood as a sheathing product in new housing, capturing nearly 75 percent of the North American market for floor, wall and ceiling panels, according to the Structural Board Association." The one market segment plywood has been able to retain, the remodeling sector, was likely to face increased competition from OSB throughout the early 2000s. "Plywood is the first choice among many remodelers, who account for less than 15 percent of OSB's annual consumption. OSB producers would like to change that ratio."

Plywood manufacturers were trying to fight back by improving technology and looking for alternative markets. Better adhesives made softwood plywood less expensive to produce. Specialty markets, including highervalued products, were being pursued.

Throughout the late 1990s plywood production shifted from the West to the South, which produced more than 75 percent of all grades of softwood plywood. According to the U.S. Department of Commerce, the West was expected to dominate high-end construction applications.

The largest firm in the industry is Stamford, Connecticut-based International Paper Co., which acquired Champion International Corp. in 2000 and posted sales of $25.1 billion in 2003. Other leading companies in the industry include Georgia-Pacific Corp., based in Atlanta, Georgia, with 2003 sales of $20.2 billion. In 2002, the firm added to its plywood operations by acquiring two mills, one in Texas and one in Louisiana, from Louisiana-Pacific Corp. Another significant player, Oregon-based Roseburg Forest Products Co. posted 2002 sales totaling $750 million.

According to the Commerce Department, total employment for the industry dropped 20 percent from 38,000 in 1987 to 31,000 in 1992. Average earnings for workers in the industry rose during that time from just less than $10.00 an hour to approximately $10.50 an hour. Employment dropped from 29,000 in 1997 to 27,573 in 2000, with workers earning an average wage of $13.00 an hour in 2000. Most employees are found in the states of Oregon, Louisiana, Texas, and Arkansas.

International trade has been favorable but volatile for the U.S. softwood plywood and veneer industry in recent years. The economic recession led to sharp declines in imports in the early 1990s. The gradual economic recovery, coupled with timber-cutting restrictions that arose out of environmental concerns and the liberalization of trade, resulted in a sharp reversal of this decline in imports. Between 1991 and 1993, imports soared 55 percent, reaching $77 million. Between 1992 and 1996,

imports slowed down, increasing only 10 percent overall. Imports jumped to $109 million in 1997, a 23 percent increase from the previous year, with more than three-fourths coming from Canada. Increased imports from South America and Asia, particularly China, were expected to pose intense competition to U.S. plywood mills in the early 2000s. In fact, southern yellow pine plywood imports from Brazil grew more than twofold in 2001.

Exports surged as a result of trade liberalization, increasing 27 percent between 1989 and 1993, despite a 16 percent drop between 1990 and 1991. Between 1992 and 1996, exports saw a negative growth of 2 percent. However, exports increased 24 percent in 1997 (compared to the previous year) to $392 million, due to strengthening European markets. The United Kingdom, Canada, and Germany were the leading export markets. Growth rates in exports were expected to be only 1 to 2 percent through the early 2000s. Competition from OSB also remained a threat for the export market.

The industry has been challenged by the cost of complying with the growing environmental regulation of indoor pollutants. The industry set voluntary formaldehyde emission standards, and the U.S. Environmental Protection Agency (EPA) was collecting information on other forms of indoor pollutants. In the early 1990s, a national EPA investigation resulted in several companies paying millions of dollars in fines and equipment upgrades. On the other hand, timber companies and the products made from their wood were making efforts to become certified as being eco-friendly with regard to logging practices. The Forest Stewardship Council has certified 50 million acres of forest around the world.

Further Reading

"Brazil Ply Gains." Wood-Based Panels International, June-July 2002.

Canlen, Brae. "Not Your Builder's OSB." Home Channel News, 3 November 2003.

U.S. Census Bureau. "Statistics for Industry Groups and Industries: 2000." February 2002. Available from http://www.census.gov/prod/2002pubs/m00as-1.pdf .

——. "Value of Shipment for Product Classes: 2001 and Earlier Years." December 2002. Available from http://www.census.gov/prod/2003pubs/m01as-2.pdf .

Comment about this article, ask questions, or add new information about this topic: