SIC 2439

STRUCTURAL MEMBERS, NOT ELSEWHERE CLASSIFIED

This classification covers establishments primarily engaged in producing laminated or fabricated trusses, arches, and other structural members of lumber. Establishments primarily engaged in fabrication on the site of construction are classified in Division C, Construction. Establishments primarily engaged in producing prefabricated wood buildings, sections, and panels are classified in SIC 2452: Prefabricated Wood Buildings and components.

NAICS Code(s)

321912 (Cut Stock, Resawing Lumber, and Planing)

321214 (Truss Manufacturing)

321213 (Engineered Wood Member (except Truss) Manufacturing)

According to the U.S. Census Bureau, engineered wood member manufacturers operating in the United States shipped $1.8 billion worth of goods, compared to $1.7 billion in 2000. U.S. manufacturers of wood trusses shipped $4.2 billion worth of goods, compared to $4.3 billion in 2000. Sales for both industry segments had grown steadily throughout the late 1990s and early 2000s, boosted first by U.S. economic prosperity and then by brisk housing starts, the result of historically low interest rates.

In the early 2000s, most of this industry's products were used in new construction, with a fairly even distribution between residential and nonresidential markets. While residential construction increased throughout the early 2000s, nonresidential construction grew at a sluggish rate due to weak economic conditions in the United States and to the extensive building done in the late 1990s.

The industry faced the same supply constraints as did other wood-working industries. This was largely the result of environmental pressures, particularly the efforts to save the endangered spotted owl in the Pacific Northwest and to save tropical rain forests abroad.

Traditionally, mills in this industry cut joists, beams, and other structural members from large logs, but during the 1990s and 2000s, engineered wood products became increasingly popular. These innovative building materials could be made from small young trees instead of the large old trees where endangered owls lived. Moreover, these new products were often stronger than a product sawed from a single piece of lumber.

One engineered product, laminated veneer lumber, was made by using adhesive, heat, and pressure to glue together numerous layers of high-grade veneer. It was used both for the flanges of I-joists and for the construction of beams. The production of laminated veneer lumber, and a similar product, glulam timber, increased throughout the 1990s.

Engineered wood products such as parallel strand lumber and laminated strand lumber were made with strands of wood coated with adhesive and pressed into boards. When oriented strand board (OSB) was introduced during the 1980s, it was often mistaken for an inferior nonstructural panel, but, by the late 1990s, the production of OSB was one of the most rapidly expanding segments of the engineered wood products industry. OSB cost less than plywood but met the same structural performance standards.

Other engineered wood products included series joists, which were used to support floors or ceilings. Floors made with series joists were less apt to squeak, because they were less prone to warping. Similarly, wooden I-joists were so strong that they competed with steel I-beams in small buildings where building codes allowed the use of wood.

Current Conditions

In 1999, the Structural Board Association reported that OSB was the leading structural panel in North America used for residential sheathing. About 20 mills that made OSB had been started during the mid-1990s, and at the turn of the twenty-first century, at least nine firms were planning to either open new OSB mills or increase the capacity of existing operations. The increased production, however, created a temporary oversupply of the product. At the same time, demand decreased because of a financial crisis in Asia. Although prices dropped, the continuing strength of the U.S. housing market supported the industry until prices rose again. OSB was expected to become increasingly popular for use in floors and in commercial and industrial applications. New resins and additives were being tested to increase the durability of OSB, and some types of OSB were being manufactured to resist moisture and intrusion by insects.

OSB's share of the North American sheathing market, which stood at 50 percent in 1998, increased another 25 percent between 1998 and 2003, according to the November 2003 issue of Home Channel News . "OSB has eclipsed plywood as a sheathing product in new housing, capturing nearly 75 percent of the North American market for floor, wall and ceiling panels, according to the Structural Board Association." OSB manufacturers planned to next target the remodeling sector, which accounted for less than 15 percent of OSB's annual consumption. OSB producers would like to change that ratio."

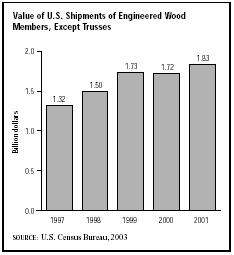

Because residential construction accounts for nearly half the market for engineered wood products, this industry is closely tied to U.S. housing starts. As a result, the strong economy of the mid- to late 1990s had brought rising revenues. Even when the economy declined in the early 2000s, housing starts remained strong due to record low interest rates. In fact, housing starts reached a 25- year high of 1.84 million units in 2003, according to the National Association of Home Builders. This trend bolstered many segments of the construction industry, including structural members. Another trend propelling the growth in this industry was the tendency for new houses to be bigger than those built in the early 1990s. The average square footage of a new home in 2002 was 2,230, compared to 2,080 in 1990. Consequently, the value of shipments for wood members, except trusses, grew from $1.32 billion in 1997 to $1.83 billion in 2001. The value of shipments for wood trusses grew from $3.4 billion to $4.2 billion over the same time period.

Industry Leaders

The largest company with structural lumber as its primary product was TJ International Inc. (Boise, Idaho), with 3,735 employees and sales of $800 million in 1999. The company reported record sales in 1997, 1998, and 1999, following a decade of steadily increasing revenues. Its subsidiaries, Norco Windows Inc. and Trus Joist MacMillan L.P., had combined sales of $706 million. Trus Joist MacMillan was the world's leading manufacturer and marketer of engineered lumber. It was jointly owned by TJ International and a Canadian company, MacMillan Bloedel Inc. In June 1999, MacMillan Bloedel was acquired by Weyerhaeuser Company, one of the world's largest forest products firms. In early 2000, Weyerhaeuser also acquired TJ International, which continues to operate as a unit of Weyerhaeuser.

Another primary contender in the category was Boise Cascade Corp. (Boise, Idaho), with 55,618 employees and 2003 sales of $8.2 billion. Wickes Inc. (Vernon Hills, Illinois) had 1,991 employees and sales of $557 million in 2002; the firm filed for Chapter 11 bankruptcy protection in 2004. Building Materials Holding Corp., based in Boise, Idaho, had 8,300 employees and

sales of $1.4 billion. Lumbermen's of Washington Inc. (Olympia, Washington) had 1,400 employees and sales of $317 million.

Various large diversified companies also made products in this classification. These included Georgia-Pacific Corporation's Building Products Division, a subsidiary of Georgia Pacific Corp. (Atlanta, Georgia); Union Camp Corp. (Wayne, New Jersey), which was acquired by International Paper Co. in 2000; Masco Corp. (Taylor, Michigan), which had sales of $10.9 billion in 2003; Stock Building Supply (Raleigh, North Carolina), which was formerly named Carolina Builders Corp.; and GAF Corp. (Wayne, New Jersey), which had sales of $1.5 billion in 2002.

Work Force

According to the U.S. Census Bureau, roughly 43,000 people were employed in the industry in 2000. Florida, California, Oregon, and North Carolina were the leading states for employment in this industry. Labor Department statistics indicated that the industry had one of the highest accident rates of any manufacturing industry, and that it had a higher accident and illness rate than the other woodworking industries.

America and the World

In the mid-1990s, Canadian building authorities called for an objective-based National Building Code which would allow for greater use of wood-based structural members. According to the Structural Board Association, half of the goods produced at mills in Alberta, Canada, in the late 1990s were products such as webs of I-beams made with OSB. According to the Engineered Wood Association, about 70 percent of structural wood panels (OSB and plywood) exported from North America went to Japan, Europe, and Mexico. Exports of structural wood panels reached 1.3 billion feet in 1998, and the association predicted that they would rise to 2.4 billion feet by the year 2003.

Further Reading

Canlen, Brae. "Not Your Builder's OSB." Home Channel News, 3 November 2003.

National Association of Home Builders. "Housing Facts, Figures, and Trends 2004." Available from http://www.nahb.org/ .

——. "Total Housing Starts for 2003 Highest in 25 Years," 2004 January 21. Available from http://www.nahb.org/ .

U.S. Census Bureau. "Statistics for Industry Groups and Industries: 2000." February 2002. Available from http://www.census.gov/prod/2002pubs/m00as-1.pdf .

——. "Value of Shipment for Product Classes: 2001 and Earlier Years." December 2002. Available from http://www.census.gov/prod/2003pubs/m01as-2.pdf .

Comment about this article, ask questions, or add new information about this topic: