SIC 3579

OFFICE MACHINES, NOT ELSEWHERE CLASSIFIED

Companies principally engaged in manufacturing miscellaneous office machines and devices comprise this industry classification. Such devices include typewriting, mailroom, and dictation machines. In addition, a multitude of companies in the industry produce specialty products, such as paper shredders, envelope stuffing machines, ticket counters, and coin wrapping machines. Establishments primarily engaged in manufacturing modems, facsimile machines, and other communications interface equipment are classified in SIC 3661: Telephone and Telegraph Apparatus.

NAICS Code(s)

339942 (Lead Pencil and Art Good Manufacturing)

334518 (Watch, Clock, and Part Manufacturing)

333313 (Office Machinery Manufacturing)

Industry Snapshot

This industry had many diverse product offerings, including time clocks, stapling machines, binding machines, collating and sorting machines, forms handling equipment, address labeling machines, automatic list finders, embossing machines, and ticket counters. Sales of miscellaneous office machines fluctuated with other economic trends. While some segments of this industry were growing, particularly those that incorporated new digital and automating capabilities, other segments were declining. The main reasons for this decrease included an increased use of computers, foreign competition, increased productivity, reduced corporate spending, and U.S. demographic changes.

Manufacturers responded to the more competitive environment of the 1990s and early 2000s by integrating the latest technology into new product offerings, infiltrating new channels of distribution and targeting home offices. Sustaining the industry during this period were record numbers of new business starts; all of the new businesses required office equipment and supplies. In addition, the booming success of the direct mail industry contributed to growth in the mailroom equipment segment of the market.

Organization and Structure

Typewriters. Typewriters and word processing machines accounted for a large segment of the miscellaneous business machines industry. While most of the units sold were electronic typewriters, some companies were still marketing electromechanical typewriters, which resemble traditional manual typewriters but use electricity to reduce the effort required by the typist and to increase the quality of type.

Electronic typewriters take the electromechanical concept a step further by reducing the number of moving parts and featuring advanced capabilities. For instance, many electronic typewriters can recall a series of pressed keys and then delete those characters from a sheet of paper on command. Some units also allow the typist to store a word or phrase in the machine's memory, which automatically recalls and prints on command.

A third model of typewriter is the personal word processor (PWP). PWPs allow the typist to view text on a screen before it is actually transferred to paper, much like a personal computer (PC). Most PWPs are simply an electronic typewriter with a liquid crystal display and a central processing unit attached. Unlike PCs, PWPs usually offer access only to internally stored proprietary software programs. Many PWPs are also equipped with spreadsheet software, and some advanced units offered disk drives, DOS compatibility, and hand-held scanners.

Typewriters and PWPs were less expensive and typically regarded as easier to use than most PCs. Even so, they continued to lag far behind PCs in popularity, despite efforts by major manufacturers to catch up. In 1996, Olympia, a home office company based in Dallas, launched a major effort to market its electronic typewriters as viable alternatives to PCs for performing simple word processing tasks without the hassle of booting up a computer. In 2000, Smith Corona Corp. announced its intentions to launch a series of new typewriters and supplies and to step up its marketing efforts with the goal of increasing typewriter sales. Despite these efforts, consumers were still expected to continue to choose the PC's versatility over the typewriter's simplicity in the new century.

Mailroom Equipment. Another major segment of the industry consisted of mailroom equipment. Designed to meter, sort, and track mail, such machines were used by the postal service, as well as private organizations. While sorting machines could mean an initial cost of anywhere from $5,000 to $500,000, they greatly reduced the cost of sorting mail manually from $35 per thousand to less than $3 per thousand pieces of mail. The most advanced sorters utilized optical character recognition (OCR) to read addresses and U.S. Postal Service bar codes.

Shredders. Shredders, used to destroy internal printed documents, accounted for a slim segment of the market. In the mid-1990s, personal shredders used by small companies and professional practices ranged widely in options and prices. The more advanced models featured conveyer belts and were capable of shredding boxes, metal binders, and entire wastebaskets. Simple model paper shredders represented the fastest growing segment of the miscellaneous office products industry in the mid-1990s, mainly due to their increased popularity for home use. Consumers began buying shredders in increasing numbers because of privacy concerns and because the prices of these devices had decreased to the point that they were now affordable for the average consumer.

Other Products. Making up the remaining portion of the miscellaneous office machines industry were a variety of specialty devices. Dictation machines, for instance, have been used by professionals and executives, for whom certain jobs require the recording of their voices for later transcription. In 2002, liquid crystal displays (LCDs) commanded a larger portion of the market.

Background and Development

The business machine industry emerged from the industrial revolution in the latter part of the nineteenth century. As the need to record and manage business information grew, several products, including the typewriter, were developed to meet demands. Although the typewriter was invented in 1714 by London engineer Henry Mill, the most famous devices were developed in the late 1800s. The Remington typewriter, first offered to the public in 1874, was one of the more popular early machines.

The first electromechanical typewriter was invented by Thomas Edison in 1872, although practical application of this device did not occur until the twentieth century. One of the first electric models, the Electromatic, was purchased by International Business Machines in 1933; after World War II, several other companies introduced electric typewriters. During the post-war era, the business machine industry flourished. A booming economy and new technology soon prompted the development of a plethora of labor-saving devices.

While dictation machines also gained widespread public acceptance during the mid-1900s, the invention of the integrated circuit in the 1960s brought hand-held recording devices into the professional mainstream. Dictaphones remained the primary means of recording information for doctors, lawyers, and business executives throughout the 1970s and much of the 1980s. The advent of personal computers, notebook computers, and cellular telephone technology adversely affected sales of dictation equipment in the 1980s, and by the early 1990s dictation machines were largely being replaced with machines featuring alternative technologies.

As increasingly inexpensive computer and cellular technology was rendering Dictaphones and typewriters obsolete, many business machine companies struggled to adapt to evolving market demands. Nevertheless, technological advances were opening new markets for other miscellaneous business machines—particularly postal equipment—in demand due to increased postal volume and new postal requirements for addresses.

Shipments of miscellaneous business machines peaked in 1985 at more than $5 billion. After that time, however, several factors combined to deflate revenues and profit margins for manufacturers. Most importantly, the popularity of superior computer technology was affecting revenues from industry staples such as typewriters and dictation equipment. Although business machine manufacturers countered with PWPs and other low-cost, higher technology products, computers threatened to eventually deplete the market for even those items.

At the same time that computers and cellular phones were making industry waves, the U.S. business machine market experienced an economic recession in the late 1980s. Revenues from miscellaneous business machines fell to about $3.2 billion in 1987. Although sales picked up in 1988 and 1989, shipments only reached $3.5 to $4.0 billion per year before slumping again in the early 1990s.

In addition to alternative technologies and the economic recession, manufacturers were also facing a more competitive market in the 1980s and early 1990s. Many products, such as typewriters, had become low-cost commodity items that offered slim profit margins. In response to price competition from both domestic and foreign manufacturers, many U.S. companies moved their production operations overseas or increased automation in domestic facilities. The number of establishments in the industry dropped 23 percent from 1990 to 1996. As a result, industry employment in the United States plummeted from about 45,000 in 1982 to about 30,000 in the early 1990s.

According to government figures, both the value of shipments and the number of establishments within the industry were expected to continue their downward slope through the end of the 1990s until the year 2000, when sales were expected to drop to $3.1 billion and the number of establishments were predicted to be as low as 129. As a result of this downward trend, employment in the industry was predicted to plummet below 20,000.

In response to these declining figures, manufacturers scrambled to buoy profits and remain competitive. Besides diverting investments into competing industries, such as computer-related office products, producers tailored product offerings to appeal to the growth market of the 1990s—small businesses.

By the mid-1990s about 40 million home offices had emerged. Because the average home office spent $40 to $50 per week on business supplies, manufacturers increasingly catered to this segment. In an effort to reach small businesses and home office buyers, manufacturers also adjusted their marketing and distribution strategies in the mid-1990s. While producers once sold products primarily through dedicated office device resellers, many companies were using 50 or more different types of retailers to move their equipment in the 1990s.

One of the fastest growing distribution channels during this time was the discount superstore and business center, such as Wal-Mart, Office Depot, and K-Mart. In the mid-1990s, manufacturers distributed an estimated 7-10 percent of their shipments through these retail chains, and some industry participants suggested that this figure would eventually exceed 20 or 30 percent. By 1997, there were more than 1,600 superstores in the North American market.

Manufacturers also boosted sales by emphasizing distribution through equipment leasing companies. Many businesses favored the lease agreement in order to take advantage of changing technology and certain tax benefits. In addition, leasing allowed companies to reduce their capital equipment investment—an important point in the capital-starved environment of the 1990s.

Current Conditions

According to the Direct Mail Information Service, reported in Print Week, spending on direct mail continued to rise in the 2000s. Despite the trend toward electronic communication and commerce, the printed direct mail industry continued to grow. According to a study done by Pitney Bowes in 2003, the majority of consumers preferred regular mail over e-mail; 86 percent preferred it for confidential materials and 66 percent preferred it for any document. This was good news to those businesses that employed direct mail, and excellent news for manufacturers of mailroom equipment and machinery.

Consequently, demand for better, faster, and more flexible mailroom equipment continued. New markets were opening up for shrink-wrapping equipment, enveloping machinery, and polythene postal wrap equipment. The trend also was toward automated digital equipment and electronic-linked equipment and network systems for mail information and services. According to Pitney Bowes, more than 60 percent of the market in 2003 was comprised of digital equipment. Growth in this segment also was assured due to the number of businesses creating in-house mailroom systems.

The export market was growing even faster than the domestic market, buoyed by currency valuations. In 2002, Japan was the fastest growing importer of goods from this industry, primarily due to the newer digital equipment capabilities.

Although not growing at the rate of newer technologies, the business market for typewriters was still strong in the early 2000s, since many office tasks were simpler or only possible on typewriters. From banks and doctors' offices to libraries and real estate offices, the typewriter was still a part of business as usual. As of 2000, the typewriter market was $400 million.

Industry Leaders

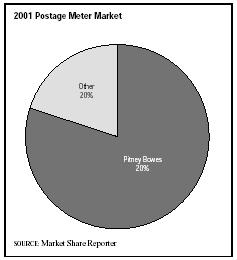

As of 2001, the industry leader remained Canon USA Inc., of Success, New York, with $8.8 billion in sales and 11,000 employees. Because Canon manufactures such a variety of products, it is difficult to discern how much of that total was attributable to the miscellaneous office equipment industry. In second place was Chicago-based Oce-USA Inc., with sales of $3.6 billion and 3,100 employees. Rounding out the top three was Pitney Bowes Inc. of Stamford, Connecticut, with $2.3 billion in sales and 26,700 employees. Pitney Bowes was the 2001 leader in the postage meter segment, commanding 80 percent of the market.

In 2001, the government spent more than $319 million on office machines. SRI International had the majority of this market share sewn up at 28 percent. Xerox Corp. and Berkshire Hathaway followed with 13 percent and 10 percent, respectively.

Research and Technology

Manufacturers sought to retain market share and revenues by delivering new products and technology in

the 1990s. PWPs represented efforts by typewriter companies to combat the dominance of PCs. Smith Corona introduced a new selection of typewriters and related equipment in an effort to boost the company's lagging sales. Olympia also expanded its line of electronic typewriters and other office equipment.

Competitors also were improving other office products such as shredders and digital voice recorders. In 1998, Alleghany Paper Shredders Corp. introduced two automated high-volume shredders designed to cut labor costs by allowing one operator to do the work of two or three. In 1999, Olympus began offering a digital voice recorder that could record thoughts and memos on a flash memory card to be edited and/or converted to text. In 2000, Royal announced the introduction of several new office products, including a computer-based time clock and four new crosscut shredders with all of the latest features.

In the mailroom equipment segment, the trend was toward greater automation and greater digital capabilities. Along with greater opportunities for e-commerce, a newer segment of the industry, bar code printers, was expected to grow at a whopping 8 percent annually through 2007, according to research analysts. This projection was largely due to the trend toward direct coding and marking, new compliance standards, and mobility of the 2000s workforce.

Further Reading

Avery, Susan. "With New Postage Meters Buyers Can Stamp Out Costs." Purchasing, 17 July 2003.

Baker, Deborah J., ed. Ward's Business Directory of US Private and Public Companies. Detroit, MI: Thomson Gale, 2003.

"Clack, Clack. The Typewriter's Back?" Wall Street Journal, 14 January 2000.

Danielli, Darryl. "Product Portfolio: Buyers' Guide—Mailroom Equipment." Print Week, 2 August 2002.

Gilroy, Amy. "Royal to Display Linux-Equipped PDA at CES." Twice, 6 January 2000.

Greenberg, Molly. "Memo to the Tech Graveyard: Don't Bury the Typewriter Yet." Business First-Columbus, 11 August 2000.

Hoover's Company Fact Sheet. "Canon USA Inc." 3 March 2004. Available from http://www.hoovers.com .

Lazich, Robert S., ed. Market Share Reporter. Detroit, MI: Thomson Gale, 2004.

"Pitney Bowes: Our Company." 2004. Available from http://www.pb.com .

"What's Ahead for Bar Code Printers." Modern Materials Handling, September 2003.

Comment about this article, ask questions, or add new information about this topic: