ETHICS

Webster's Collegiate Dictionary defines "ethics" as the "discipline dealing with what is good and bad and with moral duty and obligation," "a set of moral principles or value" or "a theory or system of moral values." Ethics assists individuals in deciding when an act is moral or immoral, right or wrong. Ethics can be grounded in natural law, religious tenets, parental and family influence, educational experiences, life experiences, and cultural and societal expectations.

Ethics in business, or business ethics as it is often called, is the application of the discipline, principles, and theories of ethics to the organizational context. Business ethics have been defined as "principles and standards that guide behavior in the world of business." Business ethics is also a descriptive term for the field of academic study in which many scholars conduct research and in which undergraduate and graduate students are exposed to ethics theory and practice, usually through the case method of analysis.

Ethical behavior in business is critical. When business firms are charged with infractions, and when employees of those firms come under legal investigation, there is a concern raised about moral behavior in business. Hence, the level of mutual trust, which is the foundation of our free-market economy, is threatened.

Although ethics in business has been an issue for academics, practitioners, and governmental regulators for decades, some believe that unethical, immoral, and/or illegal behavior is widespread in the business world. Numerous scandals in the late 1990s and early 2000s seemed to add credence to the criticism of business ethics. Corporate executives of WorldCom, a giant in the telecommunications field, admitted fraud and misrepresentation in financial statements. WorldCom's former CEO went on trial for alleged crimes related to this accounting ethics scandal.

A similar scandal engulfed Enron in the late 1990s and its former CEO, Ken Lay, also faced trial. Other notable ethical lapses were publicized involving ImClone, a biotechnological firm; Arthur Andersen, one of the largest and oldest public accounting firms; and Healthsouth, a large healthcare firm located in the southeast United States. These companies eventually suffered public humiliation, huge financial losses, and in some cases, bankruptcy or dissolution. The ethical and legal problems resulted in some corporate officials going to prison, many employees losing their jobs, and thousands of stockholders losing some or all of their savings invested in the firms' stock.

Although the examples mentioned involved top management, huge sums of money, and thousands of stakeholders, business ethics is also concerned with the day-to-day ethical dilemmas faced by millions of workers at all levels of business enterprise. It is the awareness of and judgments made in ethical dilemmas by all that determines the overall level of ethics in business. Thus, the field of business ethics is concerned not only with financial and accounting irregularities involving billions of dollars, but all kinds of moral and ethical questions, large and small, faced by those who work in business organizations.

The discussion that follows is organized into three parts: (1) the major theories or "moral philosophies" that are applied to business ethics; (2) a well-established model of ethical decision-making in business; and (3) the factors that affect individual ethical decision-making in the business context.

APPROACHES TO ETHICAL

DECISION-MAKING

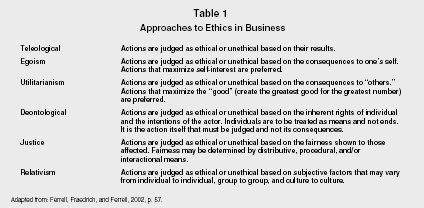

Philosophers have studied and written about ethics for thousands of years. The moral philosophies or ethical "theories" that have been developed form the foundation for ethics in business. Table 1 shows some of the major ethical philosophies that are applied to business ethics. Each of the ethical philosophies is briefly considered in this section.

TELEOLOGY.

Teleological theories of ethics focus on the consequences caused by an action and are often referred to as "consequentalist" theories. By far the most common teleological theories are egoism and utilitarianism.

EGOISM.

Egoism defines right and wrong in terms of the consequences to one's self. Egoism is defined by self-interest. An egoist would weigh an ethical dilemma or issue in terms of how different courses of action would affect his or her physical, mental, or emotional well being. Thus, an egoist, when faced with a business decision, would tend to choose the course of action that he or she believes would best serve self-interest.

Although it seems likely that egoism would potentially lead to unethical and/or illegal behavior, this philosophy of ethics is, to some degree, at the heart of a free-market economy. Since the time of political economist Adam Smith, advocates of a free market unencumbered by governmental regulation have argued that individuals, each pursuing their own self-interest, would actually benefit society at large.

This point of view is notably espoused by the famous economist Milton Friedman, who suggested that the only moral obligation of business is to make a profit and obey the law. However, it should be noted that Smith, Friedman, and most others who advocate unregulated commerce, acknowledge that some restraints on individuals' selfish impulses are required.

Approaches to Ethics in Business

| Teleological | Actions are judged as ethical or unethical based on their results. |

| Egoism | Actions are judged as ethical or unethical based on the consequences to one's self. Actions that maximize self-interest are preferred. |

| Utilitarianism | Actions are judged as ethical or unethical based on the consequences to "others." Actions that maximize the "good" (create the greatest good for the greatest number) are preferred. |

| Deontological | Actions are judged as ethical or unethical based on the inherent rights of individual and the intentions of the actor. Individuals are to be treated as means and not ends. It is the action itself that must be judged and not its consequences. |

| Justice | Actions are judged as ethical or unethical based on the fairness shown to those affected. Fairness may be determined by distributive, procedural, and/or interactional means. |

| Relativism | Actions are judged as ethical or unethical based on subjective factors that may vary from individual to individual, group to group, and culture to culture. |

UTILITARIANISM.

In the utilitarian approach to ethical reasoning, one emphasizes the utility, or the overall amount of good, that might be produced by an action or a decision. For example, companies decide to move their production facilities from one country to another. How much good is expected from the move? How much harm? If the good appears to outweigh the harm, the decision to move may be deemed an ethical one, by the utilitarian yardstick.

This approach also encompasses what has been referred to as cost-benefit analysis. In this, the costs and benefits of a decision, a policy, or an action are compared. Sometimes these can be measured in economic, social, human, or even emotional terms. When all the costs are added and compared with the results, if the benefits outweigh the costs, then the action may be considered ethical.

One fair criticism of this approach is that it is difficult to accurately measure costs and benefits. Another criticism is that the rights of those in the minority may be overlooked.

Utilitarianism is like egoism in that it advocates judging actions by their consequences, but unlike egoism utilitarianism focuses on determining the course of action that will produce the greatest good for the greatest number of people. Thus, it is the ends that determine the morality of an action and not the action itself (or the intent of the actor).

Utilitarianism is probably the dominant moral philosophy in business ethics. Utilitarianism is attractive to many business people, since the philosophy acknowledges that many actions result in good consequences for some, but bad consequences for others. This is certainly true of many decisions in business.

DEONTOLOGY.

Deontological theories of ethics focus on (1) the rights of all individuals and (2) the intentions of the person(s) performing an action. Deontological theories differ substantially from utilitarian views on ethics and would not allow, for example, the harming of some individuals in order to help others. To the deontologist, each person must be treated with the same level of respect and no one should be treated as a means to an end.

Deontology proposes that the principles of ethics are permanent and unchanging—and that adherence to these principles is at the heart of ethical behavior. Many deontologists believe that the rights of individuals are grounded in "natural law." Deontology is most closely associated with the German philosopher Immanuel Kant.

JUSTICE.

Justice-based theories of ethics concern the perceived fairness of actions. A just (ethical) action is one that treats all fairly and consistently in accord with ethical or legal standards. Justice theories of ethics are closely associated with the philosopher John Rawls.

To determine the fairness of an action, one often appeals to distributive, procedural, and/or interactional rules. Distributive fairness is based on the outcomes received by individuals and their perceptions of these outcomes. Procedural fairness is based on the processes (policies, procedures, rules) employed to reach decisions. Individuals evaluate the fairness of these processes in addition to (or instead of) the outcomes received.

Finally, interactional fairness relates to the personal treatment one receives in the administration of a decision-making process. Interpersonal fairness has to do with the respect and consideration shown in the administration of decisions. Informational fairness has to do with the explanations and accounts provided for the decisions made.

The study of organizational justice has become a major field within organizational behavior. To date, however, there has not been a complete integration between justice perceptions and ethical theory.

RELATIVISM.

Teleological, utilitarian, and justice theories of ethics are all "universal" theories, in that they purport to advance principles of morality that are permanent and relatively enduring. Relativism states that there are no universal principles of ethics and that right and wrong must be determined by each individual or group.

The relativist believes that standards of right and wrong change over time and are different across cultures—and does not accept that some ethical standards or values are superior to others. The concept of relativism can probably be summarized as "What's right for one may not be right for another," or "When in Rome, do as the Romans do."

INDIVIDUAL ETHICAL DECISION-MAKING

There are many approaches to the individual ethical decision-making process in business. However, one of the more common was developed by James Rest and has been called the four-step or four-stage model of individual ethical decision-making. Numerous scholars have applied this theory in the business context. The four steps include: ethical issue recognition, ethical (moral) judgment, ethical (moral) intent, and ethical (moral) behavior.

ETHICAL ISSUE RECOGNITION.

Before a person can apply any standards of ethical philosophy to an issue, he or she must first comprehend that the issue has an ethical component. This means that the ethical decision-making process must be "triggered" or set in motion by the awareness of an ethical dilemma. Some individuals are likely to be more sensitive to potential ethical problems than others. Numerous factors can affect whether someone recognizes an ethical issue; some of these factors are discussed in the next section.

ETHICAL (MORAL) JUDGMENT.

If an individual is confronted with a situation or issue that he or she recognizes as having an ethical component or posing an ethical dilemma, the individual will probably form some overall impression or judgment about the rightness or wrongness of the issue. The individual may reach this judgment in a variety of ways, as noted in the earlier section on ethical philosophy.

ETHICAL (MORAL) INTENT.

Once an individual reaches an ethical judgment about a situation or issue, the next stage in the decision-making process is to form a behavioral intent. That is, the individual decides what he or she will do (or not do) in regard to the perceived ethical dilemma.

According to research, ethical judgments are a strong predictor of behavioral intent. However, individuals do not always form intentions to behave that are in accord with their judgments, as various situational factors may act to influence the individual otherwise.

ETHICAL (MORAL) BEHAVIOR.

The final stage in the four-step model of ethical decision-making is to engage in some behavior in regard to the ethical dilemma. Research shows that behavioral intentions are the strongest predictor of actual behavior in general, and ethical behavior in particular. However, individuals do now always behave consistent with either their judgments or intentions in regard to ethical issues. This is particularly a problem in the business context, as peer group members, supervisors, and organizational culture may influence individuals to act in ways that are inconsistent with their own moral judgments and behavioral intentions.

Some specific factors that influence the individual ethical decision-making process, as outlined above, are presented in the final section of this essay.

FACTORS AFFECTING ETHICAL

DECISION-MAKING

In general, there are three types of influences on ethical decision-making in business: (1) individual difference factors, (2) situational (organizational) factors, and (3) issue-related factors.

INDIVIDUAL DIFFERENCE FACTORS.

Individual difference factors are personal factors about an individual that may influence their sensitivity to ethical issues, their judgment about such issues, and their related behavior. Research has identified many personal characteristics that impact ethical decision-making. The individual difference factor that has received the most research support is "cognitive moral development."

This framework, developed by Lawrence Kohlberg in the 1960s and extended by Kohlberg and other researchers in the subsequent years, helps to explain why different people make different evaluations when confronted with the same ethical issue. It posits that an individual's level of "moral development" affects their ethical issue recognition, judgment, behavioral intentions, and behavior.

According to the theory, individuals' level of moral development passes through stages as they mature. Theoretically, there are three major levels of development. The lowest level of moral development is termed the "pre-conventional" level. At the two stages of this level, the individual typically will evaluate ethical issues in light of a desire to avoid punishment and/or seek personal reward. The pre-conventional level of moral development is usually associated with small children or adolescents.

The middle level of development is called the "conventional" level. At the stages of the conventional level, the individual assesses ethical issues on the basis of the fairness to others and a desire to conform to societal rules and expectations. Thus, the individual looks outside him or herself to determine right and wrong. According to Kohlberg, most adults operate at the conventional level of moral reasoning.

The highest stage of moral development is the "principled" level. The principled level, the individual is likely to apply principles (which may be utilitarian, deontological, or justice) to ethical issues in an attempt to resolve them. According to Kohlberg, a principled person looks inside him or herself and is less likely to be influenced by situational (organizational) expectations.

The cognitive moral development framework is relevant to business ethics because it offers a powerful explanation of individual differences in ethical reasoning. Individuals at different levels of moral development are likely to think differently about ethical issues and resolve them differently.

SITUATIONAL (ORGANIZATIONAL) FACTORS.

Individuals' ethical issue recognition, judgment, and behavior are affected by contextual factors. In the business ethics context, the organizational factors that affect ethical decision-making include the work group, the supervisor, organizational policies and procedures, organizational codes of conduct, and the overall organizational culture. Each of these factors, individually and collectively, can cause individuals to reach different conclusions about ethical issues than they would have on their own. This section looks at one of these organizational factors, codes of conduct, in more detail.

Codes of conduct are formal policies, procedures, and enforcement mechanisms that spell out the moral and ethical expectations of the organization. A key part of organizational codes of conduct are written ethics codes. Ethics codes are statements of the norms and beliefs of an organization. These norms and beliefs are generally proposed, discussed, and defined by the senior executives in the firm. Whatever process is used for their determination, the norms and beliefs are then disseminated throughout the firm.

An example of a code item would be, "Employees of this company will not accept personal gifts with a monetary value over $25 in total from any business friend or associate, and they are expected to pay their full share of the costs for meals or other entertainment (concerts, the theater, sporting events, etc.) that have a value above $25 per person." Hosmer points out that the norms in an ethical code are generally expressed as a series of negative statements, for it is easier to list the things a person should not do than to be precise about the things a person should.

Almost all large companies and many small companies have ethics codes. However, in and of themselves ethics codes are unlikely to influence individuals to be more ethical in the conduct of business. To be effective, ethics codes must be part of a value system that permeates the culture of the organization. Executives must display genuine commitment to the ideals expressed in the written code—if their behavior is inconsistent with the formal code, the code's effectiveness will be reduced considerably.

At a minimum, the code of conduct must be specific to the ethical issues confronted in the particular industry or company. It should be the subject of ethics training that focuses on actual dilemmas likely to be faced by employees in the organization. The conduct code must contain communication mechanisms for the dissemination of the organizational ethical standards and for the reporting of perceived wrongdoing within the organization by employees.

Organizations must also ensure that perceived ethical violations are adequately investigated and that wrongdoing is punished. Research suggests that unless ethical behavior is rewarded and unethical behavior punished, that written codes of conduct are unlikely to be effective.

ISSUE-RELATED FACTORS.

Conceptual research by Thomas Jones in the 1990s and subsequent empirical studies suggest that ethical issues in business must have a certain level of "moral intensity" before they will trigger ethical decision-making processes. Thus, individual and situational factors are unlikely to influence decision-making for issues considered by the individual to be minor.

Certain characteristics of issues determine their moral intensity. In general, the research suggests that issues with more serious consequences are more likely to reach the threshold level of intensity. Likewise, issues that are deemed by a societal consensus to be ethical or unethical are more likely to trigger ethical decision-making processes.

In summary, business ethics is an exceedingly complicated area, one that has contemporary significance for all business practitioners. There are, however, guidelines in place for effective ethical decision making. These all have their positive and negative sides, but taken together, they may assist the businessperson to steer toward the most ethical decision possible under a particular set of circumstances.

SEE ALSO: Goals and Goal Setting ; Mission and Vision Statements

James H. Conley

Revised by Tim Barnett

FURTHER READING:

Barnett, Tim, and Sean Valentine. "Issue Contingencies and Marketers' Recognition of Ethical Issues, Ethical Judgments, and Behavioral Intentions." Journal of Business Research 57 (2004): 338–346.

Beauchamp, Tom L., and Norman E. Bowie. Ethical Theory and Business. Englewood Cliffs, NJ: Prentice Hall, 1993.

Ferrell, O.C., John Fraedrich, and Linda Ferrell. Business Ethics. Boston, MA: Houghton Mifflin Company, 2002.

Hosmer, LaRue Tone. The Ethics of Management. Homewood, IL: Irwin, 1991.

Kuhn, James W., and Donald W. Shriver, Jr. Beyond Success. New York, NY: Oxford University Press, 1991.

MacIntyre, Alasdair. After Virtue. Notre Dame, IN: University of Notre Dame Press, 1984.

Paine, Lynn Sharp. "Managing for Organizational Integrity." Harvard Business Review (March-April 1994).

Post, James E., William C. Frederick, Anne T. Lawrence, and James Weber. Business and Society. New York: McGraw-Hill, 1996.

Raiborn, Cecily A., and Dinah Payne. "Corporate Codes of Conduct: A Collective Conscience and Continuum." Journal of Business Ethics 9 (1990): 879–889.

Trevino, Linda K., and Michael E. Brown. "Managing to Be Ethical: Debunking Five Business Ethics Myths." Academy of Management Executive 18 (2004): 69–81.

Comment about this article, ask questions, or add new information about this topic: