PRODUCT LIFE CYCLE

AND INDUSTRY LIFE CYCLE

Recognizing that all living things go through a cycle of birth, growth, maturity, and death, the inspiration for the concepts of product life cycle and industry life cycle comes from biology. The life-cycle concept is an appropriate description of what happens to products and industries over time. When applied to organizations, the product life cycle and industry life cycle contain the four stages of introduction, growth, maturity, and decline.

This concept is much more than an interesting analogy of business and biology. In biology, a living organism's position in its life cycle leads to different courses of action concerning the organism's future. An industry's position and a product's position in their life cycles also lead to very different decisions concerning their futures. Consequently, the life-cycle concept was adopted from biology for use as a strategic planning tool for products and industries.

The following sections define the terms, explain why products have a life cycle, describe the stages of the product life cycle, and examine the strategic implications of the product life cycle.

DEFINITIONS

The life cycle can be used to observe the behavior of many concepts in business. In its classic form, which is described in a later section, it is best applied to products and industries. Used in this form, a product is not individual but a group of similar products. For example, the Chevrolet Malibu, Ford Taurus, and Honda Accord are a product group of mid-sized sedans.

Industry is a much broader classification than product; an industry consists of many similar groups of products. The product groups of mid-size sedan, pickup truck, and sport-utility vehicle all belong to the automobile industry.

Generally, industries have longer life cycles than products. The automobile industry has lasted more than 100 years and shows no signs of declining. However, the large family-sedan appears to be well into the decline stage. After decades of dominance in the automobile industry, only a few large cars, such as Ford's Crown Victoria, are being manufactured.

The life-cycle concept also describes individual brand products, such as the Ford Taurus. However, individual products in a group of products usually have much shorter life cycles, and they do not always follow the classic shape of the product life cycle. They may be introduced and die, and then be reintroduced again at a latter point. For example, the Chevrolet Nova has had more than one life cycle. Consequently, products are defined as groups of similar products, and industries defined as a collection of comparable product groups.

The discussion that follows is applicable to both industries and products. The terms product life cycle and industry life cycle both refer to the four stages of introduction, growth, maturity, and decline. To simplify the discussion, both the product life cycle and industry life cycle will be combined and simply called the product life cycle.

RATIONALE FOR THE PRODUCT

LIFE CYCLE

Since products are not living beings, why do they have life cycles? The reason is that society accepts products at different rates, but all go through similar stages of societal acceptance. This acceptance of innovations by societies is called the diffusion of innovations. As society begins to adopt and accept an innovation, the new product grows, eventually reaching maturity. When there is a better alternative to the product or when public preference changes, the products will enter a decline, possibly ending with the death of the product.

The diffusion-of-innovations concept categorizes society by the speed with which the individual members adopt a new product. It classifies people into the five categories of innovators, early adopters, early majority, late majority, and laggards.

INNOVATORS.

The first people in a society to adopt a new product are the innovators. These people are risk takers and may be looking for new products to try. They represent only 2.5 percent of the population. Though these people are the first to try a product, they are not usually opinion leaders. Consequently, they do not pass information about the product to the rest of the population.

EARLY ADOPTERS.

The early adopters have many opinion leaders in their ranks. They are the first people in the neighborhood to try a new product, and many of them willingly pass the information about the product onto other people. Their experiences can determine whether a product will have a long or short life cycle. They represent about 13.5 percent of the population.

EARLY MAJORITY.

Once the early adopters have tried and given their approval to a product, the early majority will begin to follow. Thirty-four percent of the population is in this category. Since they represent such a large percent of the population, the adoption by the early majority causes the new product to enter a period of rapid growth.

LATE MAJORITY.

After a significant portion of the population has adopted a product, the late majority will consider its use. These people are not risk takers; they typically wait until they see the product approved by others. They also represent about 34 percent of the population. Once they have adopted the product, the innovators, early adopters, early majority, and late majority represent a total of about 84 percent of the population. By this point, the new product will have reached its maturity.

LAGGARDS.

The last category of society to adopt a new product is generally fearful about trying new things. Often, they wait until being forced to adopt because the alternate product is no longer being produced. The laggards represent about 16 percent of the population.

NEW-PRODUCT DEVELOPMENT

Although product development is not usually recognized as a formal stage in the product life cycle, many ideas for long-term product planning are derived from the concepts that are generated through this preliminary process. Product development is defined as a strategy for company growth by offering modified or new products to current market segments. Additionally, product development focuses on turning product concepts into a physical product, while ensuring that that the idea can be turned into a workable product through each stage.

In the product development stage, costs begin to accumulate due to the investment in proposed concepts and ideas. Before introduction, a successful product in the marketplace will go through the following eight distinct stages of new product development: idea generation, idea screening, concept development, marketing strategy, business analysis, product development, test marketing, and commercialization.

Idea generation usually stems from the organization's internal sources (R&D, engineering, marketing). Company employees will brainstorm new ideas to generate viable product concepts. Additionally, a company may also analyze their competition's new product offerings with the intention of differentiating and improving on existing designs.

Ideas are ultimately screened, reducing the number of unrealistic concepts and focusing on realistic, attainable concepts. A single idea is developed into a product concept. Concepts are then tested to measure how appealing the product might be to consumers from the anticipated target market. Testing may range from focus groups to random surveys.

After concept testing, a marketing strategy is needed to define how the product will be positioned in the marketplace. Identifying the product's anticipated target market, financial expectations, distribution channels, and pricing strategy are also determined at this time.

Business analysis, including sales forecasting, determines if the product will be profitable to manufacturer. Many factors are considered when judging the products anticipated profitability. Managers will look at the length of time it takes for the product to be profitable, cost of capital, and other financial considerations when deciding weather to proceed with development. If the concept is approved, a prototype is created from the product concept.

The prototype undergoes rigorous testing to ensure safety and effectiveness of the product. These tests are a good measure for determining whether or not a product is safe and if it should if the designers should move forward with the creation of the product.

Once a successful prototype is developed, companies perform test marketing on the product. Typically, a company will conduct formal research on a product concept to see if the proposed idea has validity with the targeted audience. Again, customer surveys and focus groups are conducted with the intention of testing the product on a sample of the targeted demographic. The testing is then analyzed to measure consumer reaction to the product. Once all the information is available and the company decides to introduce the product, high commercialization costs are incurred.

STAGES OF THE PRODUCT LIFE CYCLE

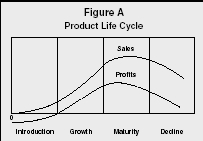

As stated above, the product life cycle consists of four stages: introduction, growth, maturity, and decline. Figure A illustrates the product life cycle. Determination of a product's stage in its life cycle is not based on age, but on the relationship of sales, costs, profits, and number of competitors. Each of these stages is described below.

Product Life Cycle

INTRODUCTION.

When a new product is introduced to a market, the innovators may be the only people aware of the new product. If the product is a new product class, the innovators may not know what the product uses are. Recalling that the innovators represent only a small percent of the population, the sales of the new product will be low. However, there is an advantage in this situation in that the new product does not yet have any competition. During the introduction stage of a new product, the developer enjoys a monopoly.

Unfortunately, the product monopoly does not usually translate to immediate profits. The product may have been in development for a long time and considerable development costs are still in the recovery phase. Also, an expensive marketing effort may be needed to introduce the product to the public. With low sales and high expenses, the introduction stage of the life cycle is usually a money loser for the company. However, the hope is for the future of the product, and the company usually is more than willing to incur the losses.

GROWTH.

As the early adopters begin to try the product, a sale begins to grow and profits usually start to follow. This is a great time for a company introducing a new product because the company still enjoys a monopoly early in the growth stage. The company is reaping all the sales and profits of the new product. When Chrysler introduced the idea of the minivan, they were in this enviable position of having the only minivan on the market.

As the early adopters begin influencing the early majority, sales and profits sore. The competition has also been watching from the new product's inception. Unfortunately for the original firm, the competition has also noticed the new product's success. Although they cannot be the first, the competition races to offer their own products and gain a share of a growing market. Chrysler's minivan did not maintain its monopoly for long; soon, the other major automobile manufacturers offered models to compete with Chrysler. Although total sales and profits continue to grow throughout the growth stage, they are divided among many manufacturers.

MATURITY.

By the end of the growth stage of the life cycle, the market is beginning to become very competitive, and this trend continues into the early period of the maturity stage. Besides many more manufacturers offering their products, the producers continue the product-differentiation process begun in the growth stage. The result is a market saturated with many manufacturers offering many models of the product. These manufacturers produce a multitude of models, from desktop computers to notebooks.

With so many companies now in the market, the competition for customers becomes fierce. Although total sales continue to grow during the first part of the maturity stage, the increased competition causes profits to peak at the end of the growth stage and beginning of the maturity stage. Profits then decline during the remainder of the maturity stage. The declining profits mean that the market is not as attractive to companies as it was in the growth stage.

In the growth stage, even inefficient companies made money. However, only the best companies and their products survive in the maturity stage. Manufacturers begin to drop out as they see profits turn to losses. Though there is still competition in the computer industry, for example, companies such as Dell and Apple have emerged as the leaders in the market. During the later part of the maturity stage, even sales begin to dip, putting more pressure on the remaining manufacturers.

DECLINE.

The number of companies abandoning the market continues and accelerates in the decline stage. Not only does the efficiency of the company play a factor in the decline, but also the product category itself now becomes a factor. By this time, the market may perceive the product as "old," and it may no longer be in demand. For example, the public replaced their preference for station wagons with their desire for minivans. Advancing technology may also bypass and replace a product, as when tapes and CDs replaced the vinyl record.

The product will continue to exist as long as a few manufacturers can maintain profitability. The laggards will resist switching to the alternative, and manufacturers who can profitably serve this niche will continue to do so. Eventually, even the laggards will switch, and the last companies producing the product will be forced to withdraw, thereby killing the product group.

PRODUCT STRATEGIES DURING

THE PRODUCT LIFE CYCLE

Depending on the stage of the product life cycle, the marketing strategy should vary to meet the changing conditions. The marketing mix consists of the product, promotion, price, and distribution. Each element must change with the product life cycle if the company expects to maximize sales and profits. It is important to note that as products move through each stage of the life cycle, they should be monitored and re-evaluated in terms of reducing both production costs and the time it takes to make a product or service profitable with its new position.

Strategic options for products during the product life cycle are examined below.

INTRODUCTION STAGE.

In the introduction stage, the product's novelty and lack of competition dominate the marketing strategy. The public is not aware of the product and does not know what benefits it offers them.

Product strategy is focused on introducing one model. Since the public is unaware of the product, to offer more models could confuse them as they learn the purpose of the product. This model may offer various options, but there are usually no major variations on the basic idea of the product. The cost of development may also prohibit the company from developing more models for introduction. With no competition yet in the product category, one model is adequate for introduction.

Since the product is new, persuading the market to buy the product is of secondary importance to informing the public that the product exists. It is the innovators who will begin to buy the product, and they need to be informed. With only one company offering the product, those innovators that decide to purchase the product have only one company from which they can purchase the product. Consequently, the promotion efforts concentrate on informing the public of the product benefits and the company producing the product. Persuasion to buy a particular brand is not needed in the introduction stage.

The pricing policy offers the company an opportunity to regain some development costs. Since the company's product is not only new to the company, but also introduces a new product, the company can use a skimming pricing strategy; that is, a very high price for the new product. Though the high price of the new product may deter some potential customers, many innovators and early adopters will pay the high price to own the new product. The first electronic calculators, for example, were quite expensive. If the product is easily copied, however, the developer may want to use a low-price penetration policy to deter future competition.

Since there are few purchasers in the introduction stage, the distribution does not need to be widespread. The innovators are risk takers and desire to purchase something new. Consequently, they may seek out the distributors carrying the new product, and only a few distributors will suffice.

GROWTH STAGE.

In the growth stage, the early adopters, followed by the early majority, begin to consume the product in growing numbers. The increasing sales result in the emergence of profits rather than losses.

During the early part of the growth stage, the company can continue its product policy of offering one basic model. However, if the new product group is successful, eventually competitors will offer their own products to compete in the new category. At that point, the original company will need to offer more models. The models should be differentiated from one another so that the company can continue to attract the new customers coming into the market.

Even with competition beginning to offer their products in the new category, the original company still dominates the market. However, as the market leader rather than a monopoly, the company will need to change its promotion policy of informing the public about their new product and new product category.

With an informing policy, the market leader would still receive the majority of new sales. Unfortunately for the original company, the competition will not be using an informative policy. They will be trying to persuade the public why their product is better than the market leader's product. Consequently, the market leader should switch to a persuasive promotion policy.

As the competition enters the market, they will probably be offering products at prices lower than the price of the original product. This is a penetration pricing policy designed to take sales away from the market leader. If the original company used a skimming pricing policy, its continued use would surely lead to rapid lost sales to the competition unless it is altered. Prices should be lowered so that sales can continue to grow, and the competition kept at bay.

In a growing market, the company's exclusive distribution policy would limit the potential growth for the firm, and sales would go to the competition. Consequently, the company must increase its product distribution to maintain its leadership in the market.

MATURITY STAGE.

Many competitors characterize the maturity stage. With the large number of firms producing products, the competition for customers becomes quite intense, and profits decline. The strategy for firms during the maturity stage becomes one of survival, as many competitors will eventually withdraw from the market.

With many companies offering several models of the product, the number of products on the market becomes tremendous. The original company must continue differentiating their models so that the market is aware of the differences in the company's products and the competitors' products. The customers are going to ask why they should buy a particular company's product; just because the product was the first on the market is not going to persuade the customers to continue buying the product. Quality, styling, and product features are a few of the means of differentiating the product from the competition.

During the maturity stage, the need to inform the public has long since passed. Now, the promotion strategy focus is on continuing the persuasion tactics started during the growth stage. The purpose of persuasion is to position the product to the market, which involves creating an image for a product. The image should not be an advertiser's creation, but based on the reality of the product.

The differentiation methods of quality, styling, and features are excellent means of positioning a product. For example, a Chevrolet Corvette and Porsche Boxster are both sports cars, but consumers see the different positions of the cars. The company differentiates its products and uses promotion to create the different position image. Each company hopes that its position is preferred by the consumers.

With the intense competition, management keeps the price of the product to its lowest possible level. For example, the competition for entry-level personal computers has now shifted to offering the lowest price. All of the companies in a mature market must now watch costs carefully.

Every aspect from development through production through marketing is designed to offer the lowest cost possible. A cost and a price advantage over competitors in this stage are significant competitive advantages. Consumers are aware of prices and will reward the company with the lower price, all else being equal. The firm that does not have a significant cost advantage risks losing customers and going out of business.

The absence of a company's product in a particular location may result in lost sales during the maturity period. Widespread distribution is essential. If the company's product is not in a particular location, one or more of the competitors' products are likely to be there. The firm cannot risk losing sales simply because their products were not available.

DECLINE STAGE.

During the decline stage, sales and profits begin an even sharper drop, and the number of competitors is reduced even further. With public preference for this product waning, the decline stage continues until the last of the producers cannot make a profit, and the product category dies.

The product strategy now becomes one of reducing the number of models offered. With the public abandoning the product and competition declining, the need for many models is no longer there. The company now focuses its attention on the costs and profitability of the remaining models. Costs, such as research and development and production, are cut to the minimal amount necessary. After the cost cuts, management eliminates those products that are no longer profitable.

The promotion efforts also include an examination of costs. Only the minimal amount of promotion necessary to keep the product selling is done. The remaining people in the market want the product and do not need to be convinced that they should buy the product. They only need to know that the product is still available. Consequently, the promotion effort shifts to reminder promotion.

Products' prices are also kept as low as possible during the decline stage. Since the number of competitors has dropped, it may seem that a company could raise prices. If the remaining customers maintain strong brand loyalty, this policy might be possible. However, the product has fallen out of favor, and customers have other product alternatives. A price increase that could not be justified by cost increases runs the risk of alienating even the few customers left purchasing the product. Consequently, the strategy should be to keep the prices as low as possible.

Cost is also an overriding factor in the distribution of the product during the decline stage. The declining sales may not justify the widespread distribution reached during the maturity stage. Only those areas or markets that are still profitable should be covered, and the unprofitable distribution outlets eliminated. Hopefully for the last companies producing the product, the brand-loyal customers or laggards will seek out the limited locations of the products and continue purchasing it.

DECLINE STAGE TRAP.

Just because a product's sales begin to decline does not mean that the product life cycle has reached the decline stage. However, if the company believes that the product is in a decline, the implementation of the decline stage strategies may lead to the death of the product long before its time.

Before the strategies for declining products are tried, the company should definitely establish that the product is in decline. The company should first follow strategies to boost sales and not resign themselves to the cost-cutting strategies of the decline stage. For example, Arm & Hammer could have easily decided that their baking soda was dying, and implemented decline stage strategies. However, they chose to fight for its life. They differentiated the product by finding new uses—such as a deodorizer and an ingredient in toothpaste. They so successfully repositioned the product that many people now think about baking soda as a deodorizer first and disregard its original use in baking.

Borrowed from biology, the life-cycle concept has been adapted and applied to products and industries. The product life cycle maintains that products and industries move through the stages of introduction, growth, maturity, and decline. By viewing a product from the perspective of its product-life-cycle position, management can use the product life cycle as a valuable decision-making tool. As the product moves through its life cycle, the appropriate strategies for its future development vary greatly. Knowledge of the appropriate strategies can help guide management actions.

SEE ALSO: Product Design ; Product-Process Matrix ; Strategic Planning Tools ; Strategy Formulation ; Strategy Implementation

James Henley

Revised by Matthew Ross

FURTHER READING:

Hawkins, Del I., Roger J. Best, and Kenneth A. Coney. Consumer Behavior: Building Marketing Strategy. Boston, MA: McGraw-Hill, 1998.

Kotler, Philip, and Gary Armstrong. Principles of Marketing. Upper Saddle River, NJ: Prentice Hall, 2001.

Perreault, William D., Jr., and E. Jerome McCarthy. Basic Marketing: A Global-Managerial Approach. Boston, MA: Irwin McGraw-Hill, 1999.

Teresko, John. "Making a Pitch for PLM." Industry Week 253, no. 8 (August 2004): 57.

VERY EASILY ONE CAN UNDERSTAND AFTER READING THIS WHAT IS GROWTH CYCLE

THANKS