Retail Clothing Store

BUSINESS PLAN BOSTON RAGS CLOTHING STORE

423 West Oaks Boulevard

Hartford, Connecticut 06103

This plan outlines how Boston Rags, a start-up retail men's, women's, and children's clothing store, will provide the Hartford community with unique clothing they would normally purchase outside of the state.

- EXECUTIVE SUMMARY

- COMPANY SUMMARY

- PRODUCTS

- MARKET ANALYSIS SUMMARY

- STRATEGY & IMPLEMENTATION SUMMARY

- MANAGEMENT SUMMARY

- FINANCIAL PLAN

- APPENDIX

EXECUTIVE SUMMARY

Boston Rags Clothing Store will be a start-up retail men's, women's, and children's clothing store specializing in unique clothing from other parts of the U.S. This business will be a casual urban wear traditional clothing store which will be run by the owners, Nancy Seymour and Joanne Arbor, as a Partnership. It will be located at 423 West Oaks Boulevard, near downtown Hartford, Connecticut. This store will also have a local market and will serve both youth and adults. Our intent is to provide the community with unique clothing they would normally purchase outside of the state.

The business will be financed with $18,299 of the owners' money plus $35,444 from a business loan. Starting costs are $53,743. Sales are estimated at $187, 500 per year by the first year. A positive cash flow will be produced at the end of the first year.

There are no other urban wear stores located within 20 miles of the location selected for this store. Hartford is in an urban city of approximately 104,000 people which is also a part of Hartford County area containing approximately 408,000 people.

Nancy Seymour receives a Veteran's pension (from her late husband) which is adequate for support without drawing from the business. Joanne Arbor is employed full-time by Central Connecticut State University, which is also adequate support without drawing from the business. Joanne has managerial experience and basic knowledge of accounting. She has at least 7 years of retail experience.

Objectives

Boston Rags's main objectives are to:

- Establish a unique clothing retail business in the city of Hartford, Connecticut

- Create jobs

- Provide quality clothing and customer service at a reasonable price

- Achieve the largest market share in the city for urban wear

- Be an active and vocal member of the community, and to provide continual reinvestment through participation in community activities and financial contributions

- Achieve a profit within the first year

- Continually and consistantly increase total number of customers per year

- Increase average length of customer relationships and decrease customer turnover

Mission

Boston Rags Clothing Store is a retail clothing store specializing in unique clothing and accessories. We encourage customers to be experimental with new clothing styles. Our mission is to understand what our customers' needs and hopes are after buying urban wear clothing.

Boston Rags will maintain financial balance while delivering a quality product to our customers. We will make our clothing accessible throughout our community by way of establishing a retail location, fashion shows, and events. We will make a profit and generate cash. We will provide a rewarding work environment and fair compensation to our employees, ultimately provide excellent value to our customers, and a fair return to our owners.

Keys to Success

Boston Rags's keys to success include: implementing an effective cash flow plan, achieving efficiency, running our retail store professionally, and maintaining a serious business discipline to everything we do.

Boston Rags's cash flow plan is to:

- Maintain enough money on hand each month to pay the cash obligations the following month.

- Identify and eliminate deficiencies or surpluses in cash.

- Alter business financial plans to provide more cash if deficiencies are found.

- Invest any revealed excess cash in an accessible, interest bearing, low-risk account such as a savings account or short-term CD or T-bill.

- Eliminate credit and terms to customers (not credit card sales).

- Clearly understand the urban wear market, distribution costs and competition, and continually adjust accordingly.

- Keep enough cash, as needed cushion for security, on hand to cover expenses.

- Reduce accountant expenses by producing our own summary statistics and projections via accounting software.

COMPANY SUMMARY

The business will be named "Boston Rags Clothing Store." This is to identify the store with the city of Boston, Massachusetts, where most of the store's inventory will be purchased. The name is registered in Hartford County under an assumed name.

Boston Rags Clothing Store's primary goal is to find customers and keep them coming back.

Boston Rags is designed to help customers change their look without buying an entirely new wardrobe. We will cater to the person wanting to build a new wardrobe by purchasing clothing and accessory pieces to add to clothing they already have.

Customers will rely on the business they purchase pieces from to give them continuous help and personal opinions. Theirs is a business that repeats and it will be easy to establish a strong clientele.

Customers will save money from having to buy a complete outfit by just purchasing pieces. They will also enjoy shopping in stores that are well inventoried and serviced-minded, such as Boston Rags.

Boston Rags will set the pace for urban fashion for all seasons. Last year's outfit will be accessorized to be this year's outfit. People like to buy clothing pieces and accessories to continue wearing clothing that would be out-of-date otherwise.

Boston Rags will also cater to all types of customers and for all occasions other than routine shopping. Examples: Wives buying gifts for their husbands, friends buying gifts for their friends, etc. Boston Rags's store will be a source of wearable gifts.

Retail profits can be as high as 65-85 percent on clothing and accessory pieces. The sales and profit margins in a specialty clothing and accessory store are higher than the average retail store. We have the opportunity to profit successfully.

The urban clothing market is the most exciting, fastest growing market for consumers. They will always look for unique clothing pieces and they will not hesitate to buy them.

Company Ownership

The business will be retail sales of urban clothing and associated products. Nancy Seymour will hold 50 percent ownership and Joanne Arbor will also hold 50 percent ownership. It will be set up as a partnership at start-up and then phase into a Limited Liability Corporation by the second year.

Start-up Summary

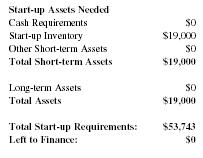

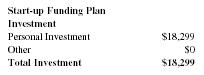

Total start-up expense (including fixtures, equipment, and grand opening) is $53,743. Startup assets required $19,000 in inventory. With the owners' investment of $18,299, the amount of additional start-up funds needed are $35,444. The details are included in the following chart and table. It is planned to start the business in the month of December because this is the Christmas seasonal month in which retail store are known to have high sales. Once established, business volume may be somewhat cyclical for that reason.

| Start-up Plan | |

| Start-up Expenses | |

| Grand Opening | $2,000 |

| Rent Deposit | $2,200 |

| Salaries and Wages | $1,200 |

| Payroll Taxes | $180 |

| Insurance | $219 |

| Telephone Deposit | $300 |

| Utilities Deposit | $840 |

| Office Supplies | $250 |

| Advertising | $600 |

| Accounting/Legal | $400 |

| Fixtures | $3,755 |

| Expensed Equipment | $4,500 |

| Repairs and Maintance | $6,900 |

| Carpet | $1,300 |

| Floor Tile | $800 |

| Sign | $1,000 |

| Counter | $4,000 |

| Travel | $4,200 |

| Burglar Alarm | $99 |

| Other | $0 |

| Total Start-up Expense | $34,743 |

| Start-up Assets Needed | |

| Cash Requirements | $0 |

| Start-up Inventory | $19,000 |

| Other Short-term Assets | $0 |

| Total Short-term Assets | $19,000 |

| Long-term Assets | $0 |

| Total Assets | $19,000 |

| Total Start-up Requirements: | $53,743 |

| Left to Finance: | $0 |

| Start-up Funding Plan | |

| Investment | |

| Personal Investment | $18,299 |

| Other | $0 |

| Total Investment | $18,299 |

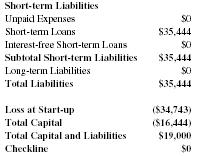

| Short-term Liabilities | |

| Unpaid Expenses | $0 |

| Short-term Loans | $35,444 |

| Interest-free Short-term Loans | $0 |

| Subtotal Short-term Liabilities | $35,444 |

| Long-term Liabilities | $0 |

| Total Liabilities | $35,444 |

| Loss at Start-up | ($34,743) |

| Total Capital | ($16,444) |

| Total Capital and Liabilities | $19,000 |

| Checkline | $0 |

Company Location and Facilities

Boston Rags Clothing Store will be located at 423 West Oaks Boulevard, Hartford, Connecticut. The store is approximately 2500 square feet. It contains two dressing rooms and a unisex restroom. Parking space is available in front of the store with additional spaces in the rear for overflow. The are a variety of businesses in the area that include Burger King, White Castle, and a flower shop along with Central Connecticut State University. This variety of businesses creates a constant flow of traffic during most business hours.

Business Operations

While a clothing retail store is not unique in itself, this business will have one-of-a-kind items and provide personal one-on-one attention to customers after hours when needed. Customers can buy sweaters, dress slacks, dress shirts, coats, jogging suits, jean outfits, childrens' items, catalog items, and more. The store hours will be 7 days a week. Store hours will be from 10 A.M. to 10 P.M., Monday through Saturday, and 11:00 A.M. to 8:00 P.M. on Sundays.

We will have two full-time employees. The wages for these employees will be $6.00 hour. We will not be offering benefits for the first couple of years. Employees will do the cleaning of the building.

The inventory will be purchased through several vendors that include: BRG Sportswear, Inc., White Sail, USA 66, Wonder, Inc., ABX, and Mark Zap Clothing, Inc. We estimate our inventory to turn over 8 times a year. Starting inventory will be $19,000 with the markup of up to 100 percent.

The following are our operation policies and will be posted throughout the store:

- 30-day layaway with 50 percent down, nonrefundable

- 30-day exchange policy, no cash refunds (this will be written on our receipts)

- $25 fee for check returns

- 2 items at a time in the dressing room

- Accepting credit cards, Visa, Mastercharge, Discover, and American Express

The owners have enlisted the professional services of Mitchell's Accounting and Investment Services to handle Boston Rags's business functions and needs. The following will be conducted by Mitchell's accounting firm:

- Weekly payroll

- Compliance with all Connecticut Sales Tax requirements

- Generate Profit and Loss Statements as required

- Consultation on an as-needed basis

- Generate all 941 requirements as required by Federal, State, and Local Taxes

- Generate all W-2s as required

- Filing all required personal tax returns will be at the current cost rates for Schedule C's and other business returns

This accounting firm will be phased out as we learn how to use the appropriate accounting software to manage our own books.

Ms. Arbor has combined managerial experience of 12 years and has also taken business management classes at Smith Community College and Hartford Business Institute. She is therefore technically qualified to handle the products the store will offer. Boston Rags will be aided in development by Ventures store out of Boston, Massachusetts, and Wonderkins Store out of New York, New York. Ventures and Wonderkins sell similar products to Boston Rags. The owners of Ventures are also close friends of Ms. Arbor. Boston Rags will also utilize the SBA Business Information Center for additional resources and business training.

The owners have referred to an attorney but will not retain an attorney until a later date. The attorney will be used for recommendations in respect to future incorporation as a Limited Liability Corporation. The attorney will also handle any future permit or certificate needs.

PRODUCTS

Urban wear has increased in popularity as the number of new musical hip-hop artists' popularity has increased over the past several years. Boston Rags will sell products similar to one hip-hop artist, Mark Zap, who has a store in New York. Like Mark's store, Boston Rags's line of clothing of more than 32 pieces, include denim, leather, twill and linen bottoms, linen and silk shirts, silk/cashmere sweater vests, T-shirts, and hats.

Boston Rags, like Mark Zap's, decided to carry a line of clothing that is a "more simple" but still gives off "a chameleon type of feel" in which "it can fit into any type of setting—not too bright or loud." According to Mark Zap this type of urban wear has projected sales in the range of $15 million to $18 million depending on store size. New growth developments in the urban wear industry have made obtaining the clothing much more simple and easy. This clothing can also be sold at festivals and fashion shows.

Inventory

Boston Rags's inventory tracking system will tell Boston Rags's management what merchandise is in stock, what is on order, when it will arrive, and what was sold. With such a system Boston Rags can plan purchases more intelligently and quickly recognize the fast moving items we need to reorder and the slow moving items we should markdown or specially promote.

We will control inventory right at the cash register with our point-of-sale (POS) software and equipment. Our POS software records each sale when it happens, so inventory records are always up-to-date. We will get more information about the sale than we would gather with a manual system. By running reports based on this information, we will be able to make better decisions.

Our POS equipment includes electronic cash drawers, bar-code scanners, credit card readers, and receipt printers. Our POS software package includes integrated accounting modules, including general ledger, accounts receivable, accounts payable, purchasing, and inventory control systems. In essence, our POS system is an all-in-one way to keep track of our business cash flow. The reporting capabilities of our POS programs include sales, costs, and profits by salesperson or by category for the day, month, and year-to-date.

We will count our inventory once every two weeks (the count cycle). Processing paperwork and placing orders with our vendors will take two weeks (the order cycle). The order will take two weeks to get to us (delivery cycle). Therefore, we will need six weeks worth of inventory from the first day of the count cycle to stay in operation until our merchandise arrives. We will have on hand a six-week supply of inventory and turn it over 8 times a year. According to Retail in Detail by Ronald L. Bond, "estimating sales for a new retail store is very difficult, and loaded with uncertainties." Bond suggests the retailer start with a range from $75 to $200 per square foot per year. We will use the very conservative figure of $75 per square foot per year, similar to Ventures in Boston, Massachusetts.

For inventory valuation we will use the Last In, First Out (LIFO) method. We will sell the most recently purchased inventory first. This method will also help us pay less in taxes.

Our inventory control system will tell us when to buy replacement inventory, what to buy, what not to buy, and how much to buy.

Suppliers will be independent craftspeople, import sources, distributors, and manufacturers. We have established a list of possible suppliers and requested quotes, prices, available discounts, and delivery terms. We have also asked them for customer references. We will also try and establish accounts with these suppliers prior to opening our store.

MARKET ANALYSIS SUMMARY

Consumer expenditures for retail sales rose to $1,139,457 in Hartford, Connecticut, and to $5,842,488 in Hartford County in 1999.

The continuous formation of new musical groups that wear urban clothing helps fuel our business, as does our free music CD store giveaways.

Market Segmentation

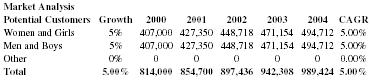

According to the Hartford Chamber of Commerce, there are approximately 150,000 males and 165,000 females in Hartford County, totaling 315,000 people. Of those 315,000 people, 186,000 are between the ages of 18 and 54 years of age. Seventy-six percent of the 315, 000 people have a household income of more than $15,000. Boston Rags's target market is men and women between the ages of 18 and 54 with a household income of $15,000 or more.

| Market Analysis | |||||||

| Potential Customers | Growth | 2000 | 2001 | 2002 | 2003 | 2004 | CAGR |

| Women and Girls | 5% | 407,000 | 427,350 | 448,718 | 471,154 | 494,712 | 5.00% |

| Men and Boys | 5% | 407,000 | 427,350 | 448,718 | 471,154 | 494,712 | 5.00% |

| Other | 0% | 0 | 0 | 0 | 0 | 0 | 0.00% |

| Total | 5.00% | 814,000 | 854,700 | 897,436 | 942,308 | 989,424 | 5.00% |

Target Market and Program Strategies

Near the business thoroughfare is a new residential subdivision under development, where houses are priced at $100,000 and above. Also in the area is the campus of Central Connecticut State University, and downtown Hartford, all which serve Boston Rags's potential customers. Boston Rags's customers are employed men and women, between the ages of 18 to 54 years old with a household medium income of $32,000 and above.

We will use flyers and other literature to act as our representative. Here are some of our marketing programs and strategies:

Designing good ad copy to reach our customers.

- Choose the proper publication

- Have a goal for our advertisement

- Involve the audience

- Inform the buyer

- Headline and illustrations grab attention

- Give them something

- Always be specific

- Make our offer a good one

- Be creative in our media choices—such as unusual avenues like—fax newsletters, mall kiosks, fax-on-demand, publicity stunts, online marketing, anything unusual to reach our target market

- Small classified ads

- Track our results

- Keep all our customers/prospects in a database and stay in touch with them regularly

- Gradually increase the size of our ad and tract the results

- Advertise regularly and consistently

- Evaluate our efforts

Customer loyalty is much more important to Boston Rags than customer satisfaction. We will serve our customers so well they will brag about Boston Rags to others. This will keep them loyal, and also provide a continual flow of customers. We will maintain our customers' happiness by using our Self-Evaluation Program.

Self-Evaluation Program asks the following questions:

- Are Boston Rags's products the best they can be?

- Is the appearance of our cashiers, managers, business surroundings, and appearance of our store professional?

- Can we clearly describe our business in 25 words or less? Can our customers describe our business in 25 words or less?

- Do our customers know about all of our products and services?

- Do we have a well-developed marketing plan that we follow on a consistent basis?

- What if our marketing plans work? Will we be able to handle the increased volume of sales without harming our customers or the quality of our work product?

- Do we treat others with honesty and respect at all times?

Advertising and Promotional Strategy

Boston Rags will try out our promotion on a small portion of our target audience before we roll out the promotion to the rest of the target market. Our tests will include variation on our basic offer, on the text or composition of our message, and on our presentation. The benefits from testing will provide to us early feedback on the response rates and margins used in our break-even calculations for that particular promotion. Testing will also help us roll out successful ideas and omit the not-so-successful ones.

With our promotions we will compare results, analyze, track responses, and measure profitability to insure our promotions are profitable.

Our advertising budget will be equal to 2 or 3 percent of our projected gross sales which averages out to be $5,627 or $457 a month after initial start-up. The budget will be based on the cost method which theorizes that an advertiser can't afford to spend more than he or she has. We will increase this amount for our grand opening.

We have taken the following steps to insure our dollars will be wisely spent on advertising.

- Established our target market by asking ourselves who our customers are and therefore whom we want to reach with our advertising.

- Setting a rough budget for broadcast advertising.

- Contacted sales managers at TV and radio stations in our area and arrange to have a salesperson visit us.

- Talked to other business people in our area about their experiences with broadcast advertising.

- Asked about the "audience delivery" of the available spots.

- Inquired about the production of our commercial.

We then compared various proposals and looked at the cost per thousands and negotiated the most attractive deal based on which outlet offers the most cost-effective way of reaching our audience. We will also buy time well in advance to lower the cost.

Our direct mail campaign will begin by getting our name on as many mailing lists as possible. We will then take note of our reaction to each piece of mail we receive and save the ones that communicate most effectively, noticing the colors, key words, and types of inserts that can be adapted to our own mailer. To get the readers involved we will include stickers that say Yes or No to be pasted on the order form. We will continue to build our direct mailing program with the resources from the Direct Marketing Association (DMA).

We plan to target our advertising to focus as narrowly as possible to the media that will reach our customers. Our customers' location, age, income, interests, and other information will be used to guide us to the right media.

Our printed ads will attract attention through a truly arresting headline and visual element. It will appeal to the reader's self-interest or announce news. It will communicate our company's unique advantage and it will prove our advantage over our competitor. Finally, it will motivate readers to take action. Our printed ads will not be a "hard sell" but it will be an all-out attempt to attract, communicate with, and motivate the reader. All of our ads will answer the customer's number one question: "What is in it for me?"

Our radio and television ads will deliver our message to more customers than any other type of ad campaign. We have a clear understanding of our market so the money spent on broadcast advertising isn't wasted.

For television ads, we will stick to 30-second spots which are standard in the industry. We understand that generally rates vary widely during the first quarter of the year, and sometimes during the third quarter or late in the fourth quarter, which are traditionally slow seasons for many businesses. We will try to avoid paying full rates during the rest of the year or during popular shows or prime time. We will also stretch our dollar by bartering our products for air time.

Our other methods of marketing will include direct mail, encompassing a wide variety of marketing materials, including brochures, catalogs, postcards, newsletters, and sales letters.

Point-of-Purchase (POP) advertising appears in various forms inside our retail store. It is designed to influence the buying behavior of our customers. POP advertising may take many forms in our store, each bearing a sales message. Here are a few examples:

- Counter cards and displays

- Window displays

- Floor stands and cutouts

- Animated displays run by electricity

- Pennants, banners, plaques, streamers

Industry Analysis and Trends

According to the 1994 U.S. Industrial Outlook stores selling mostly nondurables accounted for nearly 64 percent total retail sales, with 1993 revenues topping 1.3 trillion, up 5.7 percent over 1992. Sales of durable goods totaled 757 billion in current dollars, up more than seven percent from 1992 and accounted for 36 percent of the total.

According to The Guide to Retail Business Planning retail operations in the United States generated $2.34 trillion in sales from more than 1.5 million establishments in 1995. From 1994 to 1995 the sector as a whole grew at a rate of approximately 5 percent and represents the second-largest industry in our economy after the service industry.

Retailing has experienced more changes during the past decade than it did in the preceding generations. Although one can argue that retailing is still a domain of small businesses (that is, approximately 75 percent of all retail stores have annual sales of less than $1 million), in recent years slightly more than 80 percent of all sales were generated by stores with sales above $1 million. In addition, the growth of discount retailers has increased at a rate, some experts claim, three times that of the industry. This is due primarily to companies like Wal-Mart (which has been credited with creating one out of every 16 new jobs in the United States in 1994) and to an increase in wholesale membership clubs, such as Toys "R" Us and Circuit City.

Retail customers of the 1990s are significantly different from retail customers of a decade ago, and retail strategies need to be reassessed in view of the changing demographics and new buying patterns.

Competition and Buying Patterns

Boston Rags is located on a strip that includes a variety of businesses, but none of which create any competition. Traffic is moderate to heavy, especially near the lunch and dinner hours. The closest competing urban wear store is at least 20 miles away, located in the Hartford Valley Mall. There are no other urban wear stores in the direct vicinity of Boston Rags's location.

According to the Arbitron, Spring 2000, U.S. Dept. of Labor, Bureau of Labor Statistics, Consumer Expenditure Survey, 1998, Hartford County and surrounding areas spend in the following patterns:

Women's and Girls' Clothing

- $449.4 Thousand each Month

- $103.7 Thousand each Week

- $14.8 Thousand each Day

- $1,477 each Hour (ten-hour business day)

Men's and Boys' Clothing

- $323.4 Thousand each Month

- $74.6 Thousand each Week

- $10.6 Thousand each Day

- $1063 each Hour (ten-hour business day)

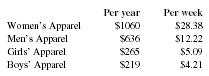

The Consumer Spending Patterns Report states that the average amount spent on clothing per household is:

| Per year | Per week | |

| Women's Apparel | $1060 | $28.38 |

| Men's Apparel | $636 | $12.22 |

| Girls' Apparel | $265 | $5.09 |

| Boys' Apparel | $219 | $4.21 |

STRATEGY & IMPLEMENTATION SUMMARY

Boston Rags uses a strategy of total market service. Our promise is in our location and the products we sell, the people we attract, and the atmosphere we create.

We will create an atmosphere that lures the "Hardcore" urban clothing fans.

Ultimately, we aren't selling either clothing or accessories. We are selling the look. We want to be part of the activity, part of the memory, part of the tradition of dressing in the latest fashions.

Strategic Assumptions:

- Every person is a potential customer and all potential markets experience growth.

- Marketing to one segment of the population will lead to an expansion in overall market growth.

Competitive Edge

Our location is a very important competitive edge. We are there, right at the point of entering or exiting downtown Hartford. The nearest competitor is at least 20 miles away.

The other competitive edge we have developed is the atmosphere and reputation. Boston Rags will bring a part of the Boston, Massachusetts, urban clothing experience to Hartford, Connecticut. That is why we are developing our fashion shows, musical guest appearances, etc. This advantage is important to us because our prices are slightly higher than other urban wear store locations in Connecticut. We will also offer more personal attention to our customers than the larger mall retail stores. We have direct connections to one of the top urban wear retailers in Boston, Massachusetts, called Ventures.

Sales Strategy

It is the intent to start the business selling the clothing people need to create a unique image of themselves. This includes various prints, colors, and styles. To increase sales and promote Boston Rags's store, special events will be held that please people, stimulate interest, pursue leisure, involve social participation, and occur within a specific, prescribed time frame. Some of our special events will include:

- Anniversaries

- Bazaars

- Celebrations

- Ceremonies

- Concerts

- Conferences

- Contests

- Conventions

- Exhibits

- Fashion Shows

- Festivals

- Grand Openings

- Open Houses

- Premieres

- Sports Shows

- Testimonials

- Trade Shows

Special events give Boston Rags powerful vehicles to promote our image, products, merchandise, services, and to generate goodwill to the public.

Boston Rags will use these special events to attract customers, sell products, earn profits, make markets aware of new developments, and make communities aware of their policies, goals, and purposes.

We will not be offering credit to our customers. We will accept checks with the assistance of a check verification company. This check verification company offers check verification and check guarantees. So, if a check has been approved by this company and it turns out to be bad, the company will reimburse us for the value of the check, eliminating our risk of getting paid.

We will accept all major credit cards. Accepting credit cards will increase the probability, speed, and size of our customers' sales. It will give us the chance to increase sales by enabling customers to make impulse buys. It will improve our cash flow because we will receive the money within a few days. It also guarantees we will be paid. All potential sales will be attended to in a timely fashion and long-term salesperson/customer relationships will be a major goal of Boston Rags.

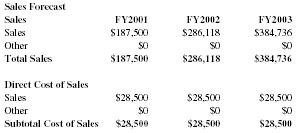

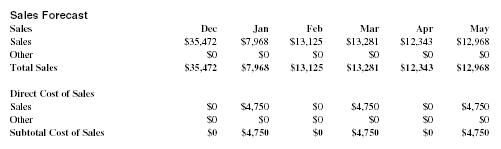

Sales Forecast

The peaks for this type of retail business are the months of August through December where sales rise as high as $34,472 for the month of December. The valleys for this type of business are January, June, and July where sales are down as far as $7,968 for the month of January. The remaining months have an average sales of about $13,000.

During the valley periods we will concentrate on a saturation of special events and sales. We will also do holiday specials.

Projected sales based on square footage ranges from $75 to $200. We used the more conservative rate of $75. The store is 2,500 square feet, multiplied by $75 to give us a Gross Sales of $187,500 the first year and maintaining that average through the second year. There will be some cycling, but it will take some experience to ascertain it. Summer months will probably be lower than winter. Computations are base on a 100 percent markup.

| Sales Forecast | |||

| Sales | FY2001 | FY2002 | FY2003 |

| Sales | $187,500 | $286,118 | $384,736 |

| Other | $0 | $0 | $0 |

| Total Sales | $187,500 | $286,118 | $384,736 |

| Direct Cost of Sales | |||

| Sales | $28,500 | $28,500 | $28,500 |

| Other | $0 | $0 | $0 |

| Subtotal Cost of Sales | $28,500 | $28,500 | $28,500 |

Strategic Alliances

Ms. Seymour and Ms. Arbor have begun to build strategic alliances to assist them with buisiness and inventory issues. Those alliances are:

- SBA Business Information Center

- Community Capital Development Corporation

- Hartford Area Investment Fund

- BRG Sportswear, Inc.

- White Sail

- USA 66

- Wonder, Inc.

- ABX

- Mark Zap Clothing, Inc.

Risks

Retailers of nondurable merchandise face a dual challenge of a slow-growing market and changes in demographics and consumer buying habits that have spawned structural changes within the industry. Boston Rags will adjust our competitive strategies to these new realities and take advantage of new marketing techniques as electronic retailing, catalog marketing, a smaller store, and improved customer service. By completing these tasks we can succeed in improving our market position in the changing retailing era of the 1990s and beyond.

The owners are injecting $18,299 of the $53,743 capital needed to start the business. Therefore, 34 percent of the risk is with the owners' money. In the event of business failure it is estimated that the owners' assets and current income would produce the $35,444 needed to repay the loan.

MANAGEMENT SUMMARY

Ms. Arbor has over seven years of experience in retail sales and over five years of managerial experience. She has held positions of responsibility which required meeting company objectives. She receives a sufficient salary from her current job to support her during the incubation period of her business. She will oversee the store on a daily basis. She, along with co-owner Ms. Seymour, will hire two staff persons to work full-time in the store. One person will be responsible for operating the cash register and loss prevention. The other person will be responsible for customer service and inventory control. Ms. Seymour will oversee day-today operations along with Ms. Arbor.

Both owners believe very strongly that relationships should be forthright, work should be structured with enough room for creativity, and pay should commensurate with the amount and quality of work completed. No person is better than another, except in ability, knowledge, and experience.

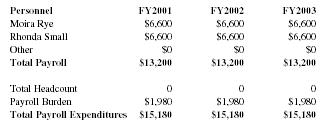

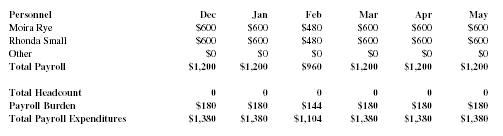

Personnel Plan

Boston Rags understands the impact hiring and managing our store's staff will have on our business success. Therefore, we have taken the time to make sure all those overseeing the store and those working directly in the store have the qualifications needed to help build our professional image.

It is the intent for the owners to be the key manpower in starting this business. They will be assisted by two full-time employees during certain hours. Employee resources include the local University and Career Alliance. Employee's age is not a factor unless they are under 18, they then would need a worker's permit.

The following two employees will be hired:

The Sales Clerk/Loss Prevention Manager will be Moira Rye. Moira has seven years of retail management experience in the area of cashier and loss prevention.

The Customer Service/Inventory Control Manager will be Rhonda Small. Rhonda has nine years of experience in the area of customer service and inventory control.

Both of these employees have an exceptionally high level of retail experience and professionalism needed to deliver excellent customer service for our customers and management of our store.

| Personnel | FY2001 | FY2002 | FY2003 |

| Moira Rye | $6,600 | $6,600 | $6,600 |

| Rhonda Small | $6,600 | $6,600 | $6,600 |

| Other | $0 | $0 | $0 |

| Total Payroll | $13,200 | $13,200 | $13,200 |

| Total Headcount | 0 | 0 | 0 |

| Payroll Burden | $1,980 | $1,980 | $1,980 |

| Total Payroll Expenditures | $15,180 | $15,180 | $15,180 |

FINANCIAL PLAN

Our financial plan anticipates the following:

- Growth will be moderate, cash flows steady

- Marketing will remain below 15 percent of sales

- The company will invest residual profits into financial markets and not company expansion (unless absolutely necessary)

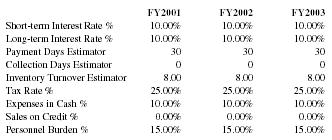

Important Assumptions

Our financial plan depends on important assumptions, most of which are shown in the following table as annual assumptions.

Some of the more important underlying assumptions are:

- We assume a strong economy, without major recession

- We assume, of course, that there are no unforeseen changes in the use of clothing which will make the need for clothing obsolete

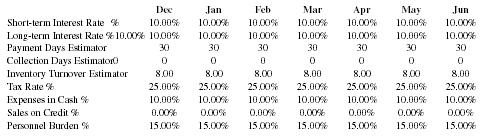

General Assumptions

| FY2001 | FY2002 | FY2003 | |

| Short-term Interest Rate % | 10.00% | 10.00% | 10.00% |

| Long-term Interest Rate % | 10.00% | 10.00% | 10.00% |

| Payment Days Estimator | 30 | 30 | 30 |

| Collection Days Estimator | 0 | 0 | 0 |

| Inventory Turnover Estimator | 8.00 | 8.00 | 8.00 |

| Tax Rate % | 25.00% | 25.00% | 25.00% |

| Expenses in Cash % | 10.00% | 10.00% | 10.00% |

| Sales on Credit % | 0.00% | 0.00% | 0.00% |

| Personnel Burden % | 15.00% | 15.00% | 15.00% |

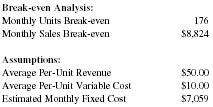

Break-even Analysis

A break-even analysis table has been completed on the basis of average costs/prices. With fixed costs of $7,059, $50 in an average sale, and $10 in average variable costs, we need $8,824 per month to break even.

| Break-even Analysis: | |

| Monthly Units Break-even | 176 |

| Monthly Sales Break-even | $8,824 |

| Assumptions: | |

| Average Per-Unit Revenue | $50.00 |

| Average Per-Unit Variable Cost | $10.00 |

| Estimated Monthly Fixed Cost | $7,059 |

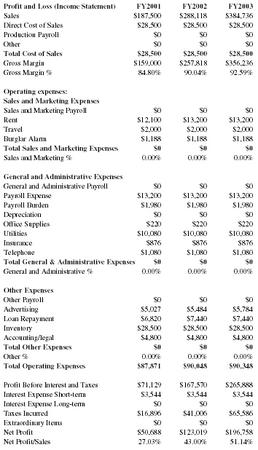

Projected Profit and Loss

Boston Rags will have a profit-to-sales ratio of just over 27 percent. Normally, a start-up concern will operate with negative profits through the first two years. We will avoid that kind of operating loss by knowing our competitors and our target markets.

| Profit and Loss (Income Statement) | FY2001 | FY2002 | FY2003 |

| Sales | $187,500 | $288,118 | $384,736 |

| Direct Cost of Sales | $28,500 | $28,500 | $28,500 |

| Production Payroll | $0 | $0 | $0 |

| Other | $0 | $0 | $0 |

| Total Cost of Sales | $28,500 | $28,500 | $28,500 |

| Gross Margin | $159,000 | $257,818 | $356,236 |

| Gross Margin % | 84.80% | 90.04% | 92.59% |

| Operating expenses: | |||

| Sales and Marketing Expenses | |||

| Sales and Marketing Payroll | $0 | $0 | $0 |

| Rent | $12,100 | $13,200 | $13,200 |

| Travel | $2,000 | $2,000 | $2,000 |

| Burglar Alarm | $1,188 | $1,188 | $1,188 |

| Total Sales and Marketing Expenses | $0 | $0 | $0 |

| Sales and Marketing % | 0.00% | 0.00% | 0.00% |

| General and Administrative Expenses | |||

| General and Administrative Payroll | $0 | $0 | $0 |

| Payroll Expense | $13,200 | $13,200 | $13,200 |

| Payroll Burden | $1,980 | $1,980 | $1,980 |

| Depreciation | $0 | $0 | $0 |

| Office Supplies | $220 | $220 | $220 |

| Utilities | $10,080 | $10,080 | $10,080 |

| Insurance | $876 | $876 | $876 |

| Telephone | $1,080 | $1,080 | $1,080 |

| Total General & Administrative Expenses | $0 | $0 | $0 |

| General and Administrative % | 0.00% | 0.00% | 0.00% |

| Other Expenses | |||

| Other Payroll | $0 | $0 | $0 |

| Advertising | $5,027 | $5,484 | $5,784 |

| Loan Repayment | $6,820 | $7,440 | $7,440 |

| Inventory | $28,500 | $28,500 | $28,500 |

| Accounting/legal | $4,800 | $4,800 | $4,800 |

| Total Other Expenses | $0 | $0 | $0 |

| Other % | 0.00% | 0.00% | 0.00% |

| Total Operating Expenses | $87,871 | $90,048 | $90,348 |

| Profit Before Interest and Taxes | $71,129 | $167,570 | $265,888 |

| Interest Expense Short-term | $3,544 | $3,544 | $3,544 |

| Interest Expense Long-term | $0 | $0 | $0 |

| Taxes Incurred | $16,896 | $41,006 | $65,586 |

| Extraordinary Items | $0 | $0 | $0 |

| Net Profit | $50,688 | $123,019 | $196,758 |

| Net Profit/Sales | 27.03% | 43.00% | 51.14% |

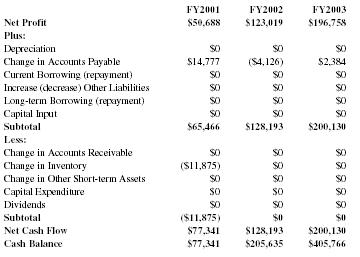

Projected Cash Flow

We are positioning ourselves in the market as a medium risk concern with steady cash flows. Accounts payable is paid at the end of each month while sales are in cash and credit cards, giving Boston Rags an excellent cash structure. Intelligent marketing will secure a cash balance of $ 77,443 by 2001.

| FY2001 | FY2002 | FY2003 | |

| Net Profit | $50,688 | $123,019 | $196,758 |

| Plus: | |||

| Depreciation | $0 | $0 | $0 |

| Change in Accounts Payable | $14,777 | ($4,126) | $2,384 |

| Current Borrowing (repayment) | $0 | $0 | $0 |

| Increase (decrease) Other Liabilities | $0 | $0 | $0 |

| Long-term Borrowing (repayment) | $0 | $0 | $0 |

| Capital Input | $0 | $0 | $0 |

| Subtotal | $65,466 | $128,193 | $200,130 |

| Less: | |||

| Change in Accounts Receivable | $0 | $0 | $0 |

| Change in Inventory | ($11,875) | $0 | $0 |

| Change in Other Short-term Assets | $0 | $0 | $0 |

| Capital Expenditure | $0 | $0 | $0 |

| Dividends | $0 | $0 | $0 |

| Subtotal | ($11,875) | $0 | $0 |

| Net Cash Flow | $77,341 | $128,193 | $200,130 |

| Cash Balance | $77,341 | $205,635 | $405,766 |

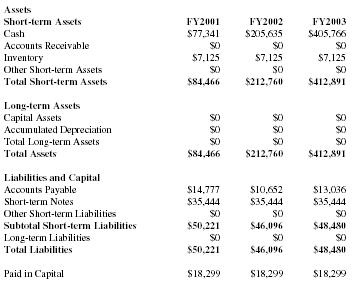

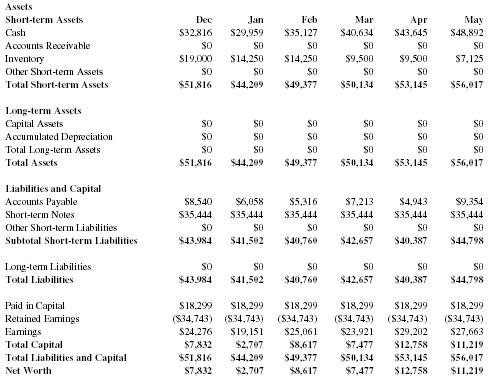

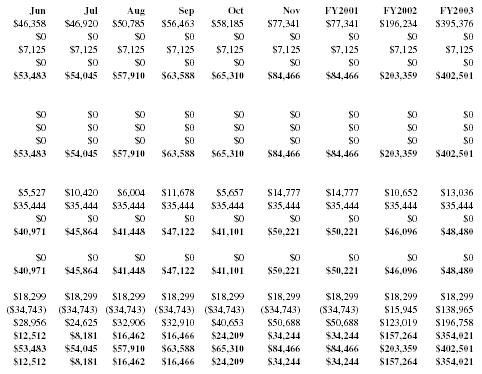

Projected Balance Sheet

All of our tables will be updated monthly to reflect past performance and future assumptions. Future assumptions will not be based on past performance but rather on economic cycle activity, regional industry strength, and future cash flow possibilities. We expect solid growth in net worth beyond the year 2002.

| Assets | |||

| Short-term Assets | FY2001 | FY2002 | FY2003 |

| Cash | $77,341 | $205,635 | $405,766 |

| Accounts Receivable | $0 | $0 | $0 |

| Inventory | $7,125 | $7,125 | $7,125 |

| Other Short-term Assets | $0 | $0 | $0 |

| Total Short-term Assets | $84,466 | $212,760 | $412,891 |

| Long-term Assets | |||

| Capital Assets | $0 | $0 | $0 |

| Accumulated Depreciation | $0 | $0 | $0 |

| Total Long-term Assets | $0 | $0 | $0 |

| Total Assets | $84,466 | $212,760 | $412,891 |

| Liabilities and Capital | |||

| Accounts Payable | $14,777 | $10,652 | $13,036 |

| Short-term Notes | $35,444 | $35,444 | $35,444 |

| Other Short-term Liabilities | $0 | $0 | $0 |

| Subtotal Short-term Liabilities | $50,221 | $46,096 | $48,480 |

| Long-term Liabilities | $0 | $0 | $0 |

| Total Liabilities | $50,221 | $46,096 | $48,480 |

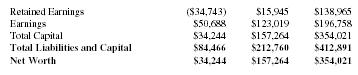

| Paid in Capital | $18,299 | $18,299 | $18,299 |

| Retained Earnings | ($34,743) | $15,945 | $138,965 |

| Earnings | $50,688 | $123,019 | $196,758 |

| Total Capital | $34,244 | $157,264 | $354,021 |

| Total Liabilities and Capital | $84,466 | $212,760 | $412,891 |

| Net Worth | $34,244 | $157,264 | $354,021 |

Business Ratios

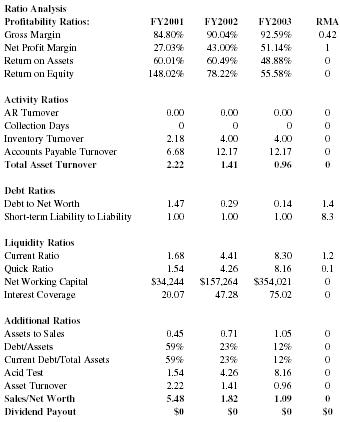

The following table shows the projected ratios. We expect to maintain healthy ratios for profitability, risk and return.

| Ratio Analysis | ||||

| Profitability Ratios: | FY2001 | FY2002 | FY2003 | RMA |

| Gross Margin | 84.80% | 90.04% | 92.59% | 0.42 |

| Net Profit Margin | 27.03% | 43.00% | 51.14% | 1 |

| Return on Assets | 60.01% | 60.49% | 48.88% | 0 |

| Return on Equity | 148.02% | 78.22% | 55.58% | 0 |

| Activity Ratios | ||||

| AR Turnover | 0.00 | 0.00 | 0.00 | 0 |

| Collection Days | 0 | 0 | 0 | 0 |

| Inventory Turnover | 2.18 | 4.00 | 4.00 | 0 |

| Accounts Payable Turnover | 6.68 | 12.17 | 12.17 | 0 |

| Total Asset Turnover | 2.22 | 1.41 | 0.96 | 0 |

| Debt Ratios | ||||

| Debt to Net Worth | 1.47 | 0.29 | 0.14 | 1.4 |

| Short-term Liability to Liability | 1.00 | 1.00 | 1.00 | 8.3 |

| Liquidity Ratios | ||||

| Current Ratio | 1.68 | 4.41 | 8.30 | 1.2 |

| Quick Ratio | 1.54 | 4.26 | 8.16 | 0.1 |

| Net Working Capital | $34,244 | $157,264 | $354,021 | 0 |

| Interest Coverage | 20.07 | 47.28 | 75.02 | 0 |

| Additional Ratios | ||||

| Assets to Sales | 0.45 | 0.71 | 1.05 | 0 |

| Debt/Assets | 59% | 23% | 12% | 0 |

| Current Debt/Total Assets | 59% | 23% | 12% | 0 |

| Acid Test | 1.54 | 4.26 | 8.16 | 0 |

| Asset Turnover | 2.22 | 1.41 | 0.96 | 0 |

| Sales/Net Worth | 5.48 | 1.82 | 1.09 | 0 |

| Dividend Payout | $0 | $0 | $0 | $0 |

APPENDIX

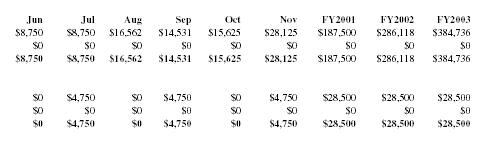

| Sales Forecast | ||||||

| Sales | Dec | Jan | Feb | Mar | Apr | May |

| Sales | $35,472 | $7,968 | $13,125 | $13,281 | $12,343 | $12,968 |

| Other | $0 | $0 | $0 | $0 | $0 | $0 |

| Total Sales | $35,472 | $7,968 | $13,125 | $13,281 | $12,343 | $12,968 |

| Direct Cost of Sales | ||||||

| Sales | $0 | $4,750 | $0 | $4,750 | $0 | $4,750 |

| Other | $0 | $0 | $0 | $0 | $0 | $0 |

| Subtotal Cost of Sales | $0 | $4,750 | $0 | $4,750 | $0 | $4,750 |

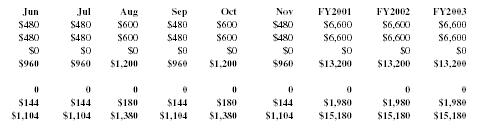

Personnel Plan

| Personnel | Dec | Jan | Feb | Mar | Apr | May | |

| Moira Rye | $600 | $600 | $480 | $600 | $600 | $600 | |

| Rhonda Small | $600 | $600 | $480 | $600 | $600 | $600 | |

| Other | $0 | $0 | $0 | $0 | $0 | $0 | |

| Total Payroll | $1,200 | $1,200 | $960 | $1,200 | $1,200 | $1,200 | |

| Total Headcount | 0 | 0 | 0 | 0 | 0 | 0 | |

| Payroll Burden | $180 | $180 | $144 | $180 | $180 | $180 | |

| Total Payroll Expenditures | $1,380 | $1,380 | $1,104 | $1,380 | $1,380 | $1,380 |

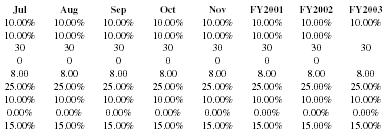

General Assumptions

| Dec | Jan | Feb | Mar | Apr | May | Jun | |

| Short-term Interest Rate % | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% |

| Long-term Interest Rate %10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% |

| Payment Days Estimator | 30 | 30 | 30 | 30 | 30 | 30 | 30 |

| Collection Days Estimator0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| Inventory Turnover Estimator | 8.00 | 8.00 | 8.00 | 8.00 | 8.00 | 8.00 | 8.00 |

| Tax Rate % | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% |

| Expenses in Cash % | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% |

| Sales on Credit % | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% |

| Personnel Burden % | 15.00% | 15.00% | 15.00% | 15.00% | 15.00% | 15.00% | 15.00% |

| Jun | Jul | Aug | Sep | Oct | Nov | FY2001 | FY2002 | FY2003 |

| $8,750 | $8,750 | $16,562 | $14,531 | $15,625 | $28,125 | $187,500 | $286,118 | $384,736 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $8,750 | $8,750 | $16,562 | $14,531 | $15,625 | $28,125 | $187,500 | $286,118 | $384,736 |

| $0 | $4,750 | $0 | $4,750 | $0 | $4,750 | $28,500 | $28,500 | $28,500 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $0 | $4,750 | $0 | $4,750 | $0 | $4,750 | $28,500 | $28,500 | $28,500 |

| Jun | Jul | Aug | Sep | Oct | Nov | FY2001 | FY2002 | FY2003 |

| $480 | $480 | $600 | $480 | $600 | $480 | $6,600 | $6,600 | $6,600 |

| $480 | $480 | $600 | $480 | $600 | $480 | $6,600 | $6,600 | $6,600 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $960 | $960 | $1,200 | $960 | $1,200 | $960 | $13,200 | $13,200 | $13,200 |

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| $144 | $144 | $180 | $144 | $180 | $144 | $1,980 | $1,980 | $1,980 |

| $1,104 | $1,104 | $1,380 | $1,104 | $1,380 | $1,104 | $15,180 | $15,180 | $15,180 |

| Jul | Aug | Sep | Oct | Nov | FY2001 | FY2002 | FY2003 | |

| 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | |

| 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | ||

| 30 | 30 | 30 | 30 | 30 | 30 | 30 | 30 | |

| 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||

| 8.00 | 8.00 | 8.00 | 8.00 | 8.00 | 8.00 | 8.00 | 8.00 | |

| 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | 25.00% | |

| 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | 10.00% | |

| 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | |

| 15.00% | 15.00% | 15.00% | 15.00% | 15.00% | 15.00% | 15.00% | 15.00% |

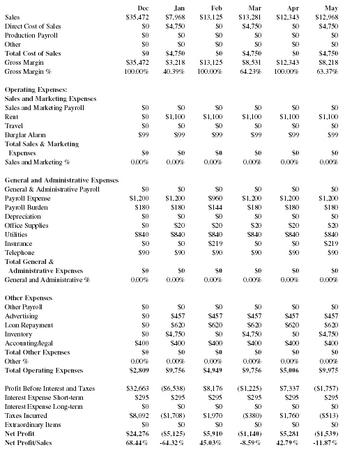

Profit and Loss (Income Statement)

| Dec | Jan | Feb | Mar | Apr | May | |

| Sales | $35,472 | $7,968 | $13,125 | $13,281 | $12,343 | $12,968 |

| Direct Cost of Sales | $0 | $4,750 | $0 | $4,750 | $0 | $4,750 |

| Production Payroll | $0 | $0 | $0 | $0 | $0 | $0 |

| Other | $0 | $0 | $0 | $0 | $0 | $0 |

| Total Cost of Sales | $0 | $4,750 | $0 | $4,750 | $0 | $4,750 |

| Gross Margin | $35,472 | $3,218 | $13,125 | $8,531 | $12,343 | $8,218 |

| Gross Margin % | 100.00% | 40.39% | 100.00% | 64.23% | 100.00% | 63.37% |

| Operating Expenses: | ||||||

| Sales and Marketing Expenses | ||||||

| Sales and Marketing Payroll | $0 | $0 | $0 | $0 | $0 | $0 |

| Rent | $0 | $1,100 | $1,100 | $1,100 | $1,100 | $1,100 |

| Travel | $0 | $0 | $0 | $0 | $0 | $0 |

| Burglar Alarm | $99 | $99 | $99 | $99 | $99 | $99 |

| Total Sales & Marketing Expenses | $0 | $0 | $0 | $0 | $0 | $0 |

| Sales and Marketing % | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% |

| General and Administrative Expenses | ||||||

| General & Administrative Payroll | $0 | $0 | $0 | $0 | $0 | $0 |

| Payroll Expense | $1,200 | $1,200 | $960 | $1,200 | $1,200 | $1,200 |

| Payroll Burden | $180 | $180 | $144 | $180 | $180 | $180 |

| Depreciation | $0 | $0 | $0 | $0 | $0 | $0 |

| Office Supplies | $0 | $20 | $20 | $20 | $20 | $20 |

| Utilities | $840 | $840 | $840 | $840 | $840 | $840 |

| Insurance | $0 | $0 | $219 | $0 | $0 | $219 |

| Telephone | $90 | $90 | $90 | $90 | $90 | $90 |

| Total General & Administrative Expenses | $0 | $0 | $0 | $0 | $0 | $0 |

| General and Administrative % | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% |

| Other Expenses | ||||||

| Other Payroll | $0 | $0 | $0 | $0 | $0 | $0 |

| Advertising | $0 | $457 | $457 | $457 | $457 | $457 |

| Loan Repayment | $0 | $620 | $620 | $620 | $620 | $620 |

| Inventory | $0 | $4,750 | $0 | $4,750 | $0 | $4,750 |

| Accounting/legal | $400 | $400 | $400 | $400 | $400 | $400 |

| Total Other Expenses | $0 | $0 | $0 | $0 | $0 | $0 |

| Other % | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% |

| Total Operating Expenses | $2,809 | $9,756 | $4,949 | $9,756 | $5,006 | $9,975 |

| Profit Before Interest and Taxes | $32,663 | ($6,538) | $8,176 | ($1,225) | $7,337 | ($1,757) |

| Interest Expense Short-term | $295 | $295 | $295 | $295 | $295 | $295 |

| Interest Expense Long-term | $0 | $0 | $0 | $0 | $0 | $0 |

| Taxes Incurred | $8,092 | ($1,708) | $1,970 | ($380) | $1,760 | ($513) |

| Extraordinary Items | $0 | $0 | $0 | $0 | $0 | $0 |

| Net Profit | $24,276 | ($5,125) | $5,910 | ($1,140) | $5,281 | ($1,539) |

| Net Profit/Sales | 68.44% | -64.32% | 45.03% | -8.59% | 42.79% | -11.87% |

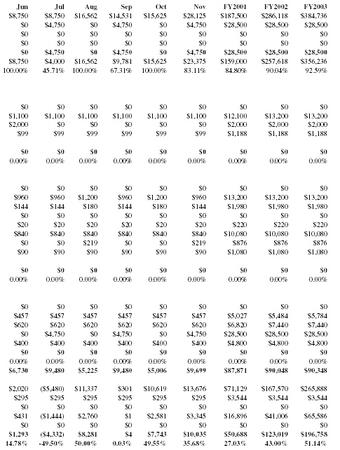

| Jun | Jul | Aug | Sep | Oct | Nov | FY2001 | FY2002 | FY2003 |

| $8,750 | $8,750 | $16,562 | $14,531 | $15,625 | $28,125 | $187,500 | $286,118 | $384,736 |

| $0 | $4,750 | $0 | $4,750 | $0 | $4,750 | $28,500 | $28,500 | $28,500 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $0 | $4,750 | $0 | $4,750 | $0 | $4,750 | $28,500 | $28,500 | $28,500 |

| $8,750 | $4,000 | $16,562 | $9,781 | $15,625 | $23,375 | $159,000 | $257,618 | $356,236 |

| 100.00% | 45.71% | 100.00% | 67.31% | 100.00% | 83.11% | 84.80% | 90.04% | 92.59% |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $1,100 | $1,100 | $1,100 | $1,100 | $1,100 | $1,100 | $12,100 | $13,200 | $13,200 |

| $2,000 | $0 | $0 | $0 | $0 | $0 | $2,000 | $2,000 | $2,000 |

| $99 | $99 | $99 | $99 | $99 | $99 | $1,188 | $1,188 | $1,188 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $960 | $960 | $1,200 | $960 | $1,200 | $960 | $13,200 | $13,200 | $13,200 |

| $144 | $144 | $180 | $144 | $180 | $144 | $1,980 | $1,980 | $1,980 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $20 | $20 | $20 | $20 | $20 | $20 | $220 | $220 | $220 |

| $840 | $840 | $840 | $840 | $840 | $840 | $10,080 | $10,080 | $10,080 |

| $0 | $0 | $219 | $0 | $0 | $219 | $876 | $876 | $876 |

| $90 | $90 | $90 | $90 | $90 | $90 | $1,080 | $1,080 | $1,080 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $457 | $457 | $457 | $457 | $457 | $457 | $5,027 | $5,484 | $5,784 |

| $620 | $620 | $620 | $620 | $620 | $620 | $6,820 | $7,440 | $7,440 |

| $0 | $4,750 | $0 | $4,750 | $0 | $4,750 | $28,500 | $28,500 | $28,500 |

| $400 | $400 | $400 | $400 | $400 | $400 | $4,800 | $4,800 | $4,800 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% | 0.00% |

| $6,730 | $9,480 | $5,225 | $9,480 | $5,006 | $9,699 | $87,871 | $90,048 | $90,348 |

| $2,020 | ($5,480) | $11,337 | $301 | $10,619 | $13,676 | $71,129 | $167,570 | $265,888 |

| $295 | $295 | $295 | $295 | $295 | $295 | $3,544 | $3,544 | $3,544 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $431 | ($1,444) | $2,760 | $1 | $2,581 | $3,345 | $16,896 | $41,006 | $65,586 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $1,293 | ($4,332) | $8,281 | $4 | $7,743 | $10,035 | $50,688 | $123,019 | $196,758 |

| 14.78% | -49.50% | 50.00% | 0.03% | 49.55% | 35.68% | 27.03% | 43.00% | 51.14% |

Projected Cash Flow

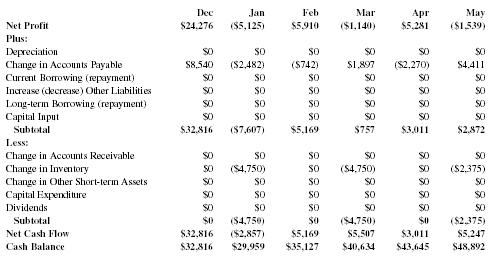

| Dec | Jan | Feb | Mar | Apr | May | |

| Net Profit | $24,276 | ($5,125) | $5,910 | ($1,140) | $5,281 | ($1,539) |

| Plus: | ||||||

| Depreciation | $0 | $0 | $0 | $0 | $0 | $0 |

| Change in Accounts Payable | $8,540 | ($2,482) | ($742) | $1,897 | ($2,270) | $4,411 |

| Current Borrowing (repayment) | $0 | $0 | $0 | $0 | $0 | $0 |

| Increase (decrease) Other Liabilities | $0 | $0 | $0 | $0 | $0 | $0 |

| Long-term Borrowing (repayment) | $0 | $0 | $0 | $0 | $0 | $0 |

| Capital Input | $0 | $0 | $0 | $0 | $0 | $0 |

| Subtotal | $32,816 | ($7,607) | $5,169 | $757 | $3,011 | $2,872 |

| Less: | ||||||

| Change in Accounts Receivable | $0 | $0 | $0 | $0 | $0 | $0 |

| Change in Inventory | $0 | ($4,750) | $0 | ($4,750) | $0 | ($2,375) |

| Change in Other Short-term Assets | $0 | $0 | $0 | $0 | $0 | $0 |

| Capital Expenditure | $0 | $0 | $0 | $0 | $0 | $0 |

| Dividends | $0 | $0 | $0 | $0 | $0 | $0 |

| Subtotal | $0 | ($4,750) | $0 | ($4,750) | $0 | ($2,375) |

| Net Cash Flow | $32,816 | ($2,857) | $5,169 | $5,507 | $3,011 | $5,247 |

| Cash Balance | $32,816 | $29,959 | $35,127 | $40,634 | $43,645 | $48,892 |

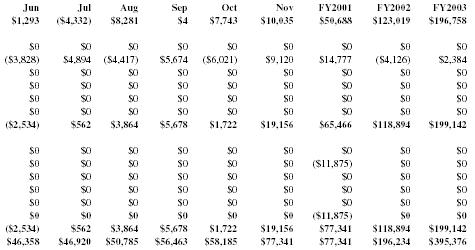

| Jun | Jul | Aug | Sep | Oct | Nov | FY2001 | FY2002 | FY2003 |

| $1,293 | ($4,332) | $8,281 | $4 | $7,743 | $10,035 | $50,688 | $123,019 | $196,758 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| ($3,828) | $4,894 | ($4,417) | $5,674 | ($6,021) | $9,120 | $14,777 | ($4,126) | $2,384 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| ($2,534) | $562 | $3,864 | $5,678 | $1,722 | $19,156 | $65,466 | $118,894 | $199,142 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $0 | $0 | $0 | $0 | $0 | $0 | ($11,875) | $0 | $0 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $0 | $0 | $0 | $0 | $0 | $0 | ($11,875) | $0 | $0 |

| ($2,534) | $562 | $3,864 | $5,678 | $1,722 | $19,156 | $77,341 | $118,894 | $199,142 |

| $46,358 | $46,920 | $50,785 | $56,463 | $58,185 | $77,341 | $77,341 | $196,234 | $395,376 |

Projected Balance Sheet

| Assets | ||||||

| Short-term Assets | Dec | Jan | Feb | Mar | Apr | May |

| Cash | $32,816 | $29,959 | $35,127 | $40,634 | $43,645 | $48,892 |

| Accounts Receivable | $0 | $0 | $0 | $0 | $0 | $0 |

| Inventory | $19,000 | $14,250 | $14,250 | $9,500 | $9,500 | $7,125 |

| Other Short-term Assets | $0 | $0 | $0 | $0 | $0 | $0 |

| Total Short-term Assets | $51,816 | $44,209 | $49,377 | $50,134 | $53,145 | $56,017 |

| Long-term Assets | ||||||

| Capital Assets | $0 | $0 | $0 | $0 | $0 | $0 |

| Accumulated Depreciation | $0 | $0 | $0 | $0 | $0 | $0 |

| Total Long-term Assets | $0 | $0 | $0 | $0 | $0 | $0 |

| Total Assets | $51,816 | $44,209 | $49,377 | $50,134 | $53,145 | $56,017 |

| Liabilities and Capital | ||||||

| Accounts Payable | $8,540 | $6,058 | $5,316 | $7,213 | $4,943 | $9,354 |

| Short-term Notes | $35,444 | $35,444 | $35,444 | $35,444 | $35,444 | $35,444 |

| Other Short-term Liabilities | $0 | $0 | $0 | $0 | $0 | $0 |

| Subtotal Short-term Liabilities | $43,984 | $41,502 | $40,760 | $42,657 | $40,387 | $44,798 |

| Long-term Liabilities | $0 | $0 | $0 | $0 | $0 | $0 |

| Total Liabilities | $43,984 | $41,502 | $40,760 | $42,657 | $40,387 | $44,798 |

| Paid in Capital | $18,299 | $18,299 | $18,299 | $18,299 | $18,299 | $18,299 |

| Retained Earnings | ($34,743) | ($34,743) | ($34,743) | ($34,743) | ($34,743) | ($34,743) |

| Earnings | $24,276 | $19,151 | $25,061 | $23,921 | $29,202 | $27,663 |

| Total Capital | $7,832 | $2,707 | $8,617 | $7,477 | $12,758 | $11,219 |

| Total Liabilities and Capital | $51,816 | $44,209 | $49,377 | $50,134 | $53,145 | $56,017 |

| Net Worth | $7,832 | $2,707 | $8,617 | $7,477 | $12,758 | $11,219 |

| Jun | Jul | Aug | Sep | Oct | Nov | FY2001 | FY2002 | FY2003 |

| $46,358 | $46,920 | $50,785 | $56,463 | $58,185 | $77,341 | $77,341 | $196,234 | $395,376 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $7,125 | $7,125 | $7,125 | $7,125 | $7,125 | $7,125 | $7,125 | $7,125 | $7,125 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $53,483 | $54,045 | $57,910 | $63,588 | $65,310 | $84,466 | $84,466 | $203,359 | $402,501 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $53,483 | $54,045 | $57,910 | $63,588 | $65,310 | $84,466 | $84,466 | $203,359 | $402,501 |

| $5,527 | $10,420 | $6,004 | $11,678 | $5,657 | $14,777 | $14,777 | $10,652 | $13,036 |

| $35,444 | $35,444 | $35,444 | $35,444 | $35,444 | $35,444 | $35,444 | $35,444 | $35,444 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $40,971 | $45,864 | $41,448 | $47,122 | $41,101 | $50,221 | $50,221 | $46,096 | $48,480 |

| $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 | $0 |

| $40,971 | $45,864 | $41,448 | $47,122 | $41,101 | $50,221 | $50,221 | $46,096 | $48,480 |

| $18,299 | $18,299 | $18,299 | $18,299 | $18,299 | $18,299 | $18,299 | $18,299 | $18,299 |

| ($34,743) | ($34,743) | ($34,743) | ($34,743) | ($34,743) | ($34,743) | ($34,743) | $15,945 | $138,965 |

| $28,956 | $24,625 | $32,906 | $32,910 | $40,653 | $50,688 | $50,688 | $123,019 | $196,758 |

| $12,512 | $8,181 | $16,462 | $16,466 | $24,209 | $34,244 | $34,244 | $157,264 | $354,021 |

| $53,483 | $54,045 | $57,910 | $63,588 | $65,310 | $84,466 | $84,466 | $203,359 | $402,501 |

| $12,512 | $8,181 | $16,462 | $16,466 | $24,209 | $34,244 | $34,244 | $157,264 | $354,021 |

A retail clothing store must buy product to fill shelves from brands and distributors for one year, sometimes six months. So whatever you project to gross in Year One, you must have at least half of the product cost, of the first projected month, available as cash on hand.

Designing, buying fixtures, branding, construction and POS integration are immense start-up costs requiring cash on hand.

Then 3-6 months wages, rent deposit according to lease agreement also need to be available.

Retail profit margins vary from 1% - 10% according to economy and style of operation. (Owner-operator obviously more profitable). $187500 at 10% profit, and you are seriously broke. Literally under them poverty line. End-game anybody?

65%, are you crazy? Product cost is 45-60% (according to trade tariffs and tax), MSRP often doubles up that dollar figure.

A store that size will not be able to reach the minimum orders required by the major distributors offering margins, based on financial, gross output, initial traffic and relational market restraints. Especially, if as a distributor, you do not know if the buyer will pay their bills.

Travel expenses to attend trade shows and buying trips to meet with vendors, and purchase product for upcoming seasons. is an expense often left-put of business plans. Be sure to include extra wages to be able to operate the store sufficiently.

This business plan should honestly have minimum $250 000 cash on hand, loans or untied cash, to start-up. Then pray to God that you don't lose your shirt.

Also, two items in the room, but you are selling the look not the items? How do you expect to add-on wardrobe? TO properly wardrobe a customer, minimum of 3 items will be in the room at all times.

And the $/sq.ft. ... $75 sales a foot? Per year? At least per season please! Why do you need a store that big? It will look empty with the amount of product you bought. And 44cents a square foot for commercial retail space, per month! That is a dumb number. Seriously. You do not want to be at a location with rent that cheap, and that number is unheard of in the industry for the size you want. Keep the store under 1000sq/ft, it will more than suffice.

The spreadsheets are well-formatted, but the dollars and logistics of this business plan are garbage. Do not use this as a source! Go talk to someone in the industry!