U.S. TREASURY NOTES

U.S. Treasury notes (T-notes) are debts with intermediate maturities of one to ten years issued by the U.S. Department of the Treasury. The Treasury issues T-notes in minimum denominations of $1,000. T-notes (and bonds) are issued in book entry form, which requires the Treasury to establish an account for the owner.

Treasury notes are sold at auction with both competitive and noncompetitive bids accepted. Noncompetitive bids are handled identically to Treasury bills auctions and are limited to a maximum of $5 million from a single bidder. Noncompetitive bids can now be made over the Internet, by phone, or by paper forms.

Unlike bill auctions where a rate of discount is indicated, bidders in T-note auctions indicate a yield to maturity. Now, T-notes, like all Treasury securities, are sold at a single price auction. The practice of awarding winning bids at multiple prices has been discontinued. Each successful competitive and noncompetitive bidder is now awarded securities at the price equivalent to the highest accepted rate or yield (i.e., lowest price) of accepted competitive tenders. Given the yield from an auction, accepted at auction, the Treasury sets the stated interest rate on new notes at the nearest 1/8 percentage point that produces an average auction price slightly below par.

T-notes are issued on a rotational basis throughout the year as follows: two-year maturities are issued monthly; five- and ten-year notes are issued quarterly during the second month of the calendar quarter. Because of the recent large budget surplus, the Treasury has announced it will be reducing the size of five- and ten-year Treasury note auctions and possibly reducing the frequency of the two-year note auctions.

Unlike U.S. Treasury bills (T-bills) which have no coupon or stated rate of interest, Treasury notes (and bonds) do carry stated rates as determined at the time of sale; they also pay interest semiannually. While T-bills will always sell at a discount, the market prices of T-notes will change in the same way as corporate bonds. Therefore, T-notes will sell at a discount or premium depending upon whether market interest rates move above, or below, the note's stated rate. Currently, all outstanding Treasury notes are noncallable.

There is also an extremely active market in T-note futures contracts. The Chicago Board of Trade began trading in Treasury note futures in June 1979. The basic trading unit is $100,000 of face value. T-note futures have become one of the most popular forms of interest rate futures. They are widely used to hedge against adverse interest rate movements.

PROS AND CONS OF T-NOTE INVESTING

Treasury notes, like other U.S. Treasury debt, have several advantages. The interest received is subject to federal income taxes, but exempt from state and local income taxes. Like other debt securities, the longer the maturity of a T-note, the greater its interest rate risk. T-notes also enjoy an extremely active secondary market, similar to other Treasury issues. Security firms and commercial depositories offer a wide variety of notes in amounts and maturities to accommodate a broad range of investors. Government securities dealers are charged with maintaining the liquidity of this market.

Since T-notes are available in the secondary market in a wide variety of maturities, an investor can select a maturity (and yield) corresponding to the investor's requirements. Given the shape of the yield curve, the existence of T-notes frequently offers investors the opportunity to take advantage of intermediate term yields, which are just a few basis points lower than long-term rates. In the fall of 1998, however, intermediate term T-notes were actually yielding less than shorter term T-bills. Thus, the investor cannot, in today's volatile money markets, make any assumption regarding the yields of T-notes relative to shorter or longer maturities.

T-note rates are often used as bellwether indicators for rates on home mortgages. Traditionally, changes in the ten-year maturity T-note rates were the best indicators of changes in mortgage rates. Recently, however, with the dramatic increase in the pace of mortgage refinancing, yields on shorter-term T-notes, usually with around three- to five-year maturities, are thought to be better indicators.

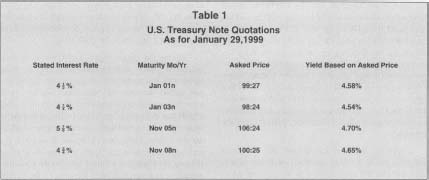

TREASURY NOTE QUOTATIONS

T-note prices are reported daily in the Wall Street Journal, together with their yields to maturity. Since they are listed with Treasury bonds, most quotation sources use the letter n after the instrument's year of maturity to designate a note. T-notes trade in 32nds of a dollar. Hence, a price quotation of 98:16 (note the use of the colon to designate 32nds) equals $985.00. Table I presents the prices and yields of selected T-notes based on January 29, 1999 trades. Quotations used by traders often include a "+" which raises the price to the next 64th (e.g., 98:12+ = 98 25/64).

The yields to maturity are computed like any other debt instrument, being equal to that interest rate, which compares the present value of the remaining interest payments and the face amount of the note to the current price of the T-note.

STRIPS

To accommodate a huge market demand for risk-free zero coupon bonds, the Treasury initiated Separate Trading of Registered Interest and Principal of Securities Notes (STRIPS). Financial institutions and

U.S. Treasury Note Quotations

As for January 29,1999

| Stated Interest Rate | Maturity Mo/Yr | Asked Price | Yield Based on Asked Price |

| 4 ½% | Jan 01 n | 99:27 | 4.58% |

| 4 ¼% | JanO3n | 98:24 | 4.54% |

| 5 ⅞% | Nov05n | 106:24 | 4.70% |

| 4 ¾% | Nov08n | 100:25 | 4.65% |

government securities brokers and dealers may request that the Treasury book the interest and principal separately to facilitate the timely payment of a wide variety of zero bond rates and maturities. Quotations for STRIPS appear with those for other Treasury instruments in the Wall Street Journal. Instruments that are stripped principal of T-notes are indicated by "np"; stripped interest is indicated by "ci." Strips are subject to the taxation features of original issue discount instruments.

FOREIGN-TARGETED NOTES

In October 1984 the Treasury instituted securities designed especially for foreign institutions and foreign branches of U.S. banks who certify that, on the day of issuance, they will place these notes only with non-U.S. citizens. After a 45-day period, foreign investors may exchange these notes for comparable domestic issues, or sell them to U.S. citizens. The Treasury sets the interest rate according to the results of the auction of the companion domestic issue and provides book-entry form during the 45-day waiting period. Afterwards, the Treasury makes registered notes available.

SEE ALSO : U.S. Treasury Bills

[ Ronald M. Horwitz ]

FURTHER READING:

Board of Governors of the Federal Reserve. The Federal Reserve System: Purposes and Functions. 7th ed. Washington DC: Board of Governors of the Federal Reserve, 1984.

——. 1989 Historical Chart Book. Washington DC: Board of Governors of the Federal Reserve, 1990.

Kahn, Milton. The Complete Guide to Buying U.S. Treasury Bills, Notes, and Bonds from the Federal Government. Denver: Klondike Publishing, 1995.

Kleege, Steven. "Does Treasury Know How to Make a Buck." Business Week, 17 October 1994.

Ricchiuto, Steve R. The Rate Reference Guide to the U.S. Treasury Market. Probus Publishing, 1990.

Ricchiuto, Steve R., and Barclays de Zoete Wedd. The Rate Reference Guide to the U.S. Treasury Market. 2nd ed. Chicago: Irwin Professional Publishing, 1996.

Rosen, Jan M. "U.S. Easing the Route to Buying Treasuries." New York Times, 9 August 1998.

U.S. Department of the Treasury. Bureau of Public Debt. "T-Bills, Notes, and Bonds." Washington: Bureau of Public Debt, U.S. Department of the Treasury, 12 August 1998. Available from www.treasurydirect.gov .

Comment about this article, ask questions, or add new information about this topic: