SIC 5945

HOBBY, TOY, AND GAME SHOPS

This industry consists of establishments primarily engaged in the retail sale of toys, games, and hobby and craft kits and supplies. Establishments primarily engaged in selling artists' supplies or collectors' items, such as coins, stamps, and autographs, are classified in SIC 5999: Miscellaneous Retail Stores, Not Elsewhere Classified.

NAICS Code(s)

451120 (Hobby, Toy, and Game Shops)

Industry Snapshot

In 2001, the U.S. Census Bureau reported 10,783 establishments primarily engaged in the wholesale distribution of games, toys, hobby goods and supplies, dolls, craft kits, children's vehicles, fireworks, and playing cards. On June 1, 2001, the International Council of Toy Conferences announced that toy sales worldwide reached $69.5 billion for 2000. According to the Toy Industries Association (TIA), total U.S. toy sales for 2002 were $25 billion. TIA also noted that was a 1.7 percent increase over 2001 toy sales. Stores ranged from independent shops to national chains, which sold toys and hobby supplies exclusively. Other types of stores carrying toys as part of their retail offerings include discounters, department stores, warehouse clubs, home supply stores, catalog houses, and drug stores.

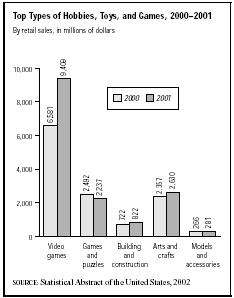

Hobby, toy, and game shops represent the largest market with 8,288 establishments. Together, they shared more than 26 percent of the market. Arts and crafts supplies numbered 8,107, comprising more than 26 percent of the market. Toys and games had 4,936 retail stores and accounted for about 16 percent of the marketplace. Hobbies followed with 2,000; hobby and craft supplies had 1,872; models, toy and hobby had 1,645; dolls and accessories shared 1,442; ceramics supplies had 1,324; children's toys and games had 754; games including chess, backgammon, and other durable games had 462; and kite stores had 188.

Organization and Structure

Manufacturers of toys and games sell their products either to wholesalers, or directly to retailers, although some manufacturers sell to both retailers and wholesalers. Retailers with multiple outlets require efficient delivery systems from their manufacturers. Toy manufacturers with outdated systems have thus found it difficult to convince large retailers to carry their products.

In the hobby and craft industry, manufacturers sell products through independent sales representatives or through their own salespeople. Wholesalers and distributors often play the role of middleman. Pre-packaged craft kits are increasingly sold in non-traditional outlets. Independent craft and toy retailers now compete with nationwide chains of specialty stores as well as with large discount stores carrying craft products. HIA estimated that nearly 20,000 stores could be considered toy and hobby outlets if sewing and other craft-related fields were included.

By the mid-1990s, the top five retailers were Toys "R" Us, Inc., Kay-Bee Toy and Hobby Shops, Inc., Wal-Mart Stores, Inc., Kmart Corporation, and Target Stores Inc. In 1999, these stores accounted for 52 percent of toy sales in the United States. Many industry observers, however, believe that specialty toy stores can still thrive in this marketplace. Those emphasizing convenience, top-notch service, and quality products are most likely to succeed.

Background and Development

With the opening of the first Toys "R" Us in the 1950s, retailing of toys in the United States changed forever. The vast retail chain began as a bicycle shop, was transformed into a juvenile furniture store, and finally became a toy store. Additional Toys "R" Us stores were soon opened; these outlets emphasized deep discounts and wide selections.

Another key factor in the growth of the retail sale of toys was the increase in the use of television advertising. In the late 1950s and early 1960s, television promotions reached into many homes where toy purchasing decisions were made.

In the 1970s many parents expressed concern about toy safety. Several consumer groups began to lobby on behalf of toy safety, as well as in search of manufacturers and retailers who would support limitations on television advertising. The National Advertising Division of the Council of Better Business Bureaus was established in 1974. It included the Children's Advertising Review Unit (CARU), which promoted responsible children's advertising.

Many toy manufacturers helped toy stores sell items by licensing products that were perceived as popular, or "hot toys." One emerging trend was the production of licensed promotional items by the retailers themselves, though this practice was limited to larger retailers who could make the investment of time, money, and space in their stores.

The late 1970s and early 1980s also saw the introduction of electronic games and toys. While retailers were enthusiastic about the tendency of buyers to purchase these items year-round, they suffered from a glut of products left on their shelves. These unsold items became so costly for some retailers that losses forced them to close in the late 1980s. This led to the consolidations that occurred in the 1990s.

In the competitive toy store industry, the latest technological advances have always been sought. Scientific progress has for many years been mirrored in toy development and sales. Independent retailers of toys, mindful of maintaining good relationships with their manufacturers, try to get early shipments of these new toys.

Video games changed the face of toy stores in the 1970s and 1980s. That craze was followed in the 1990s by excitement in toy stores over advanced software, such as computer games that incorporate CD-ROM technology.

Electronic Learning Aids, or ELAs, accounted for large sales increases in many toy stores in the early 1990s. Unlike video games, the electronic toys appeal to parents as well as children. They are age-specific and can be used even by very young children. Some ELAs require no more technology than batteries. Some, however, require purchase or rental of CD players, televisions, or VCRs. Milt Schulman wrote in Playthings that industry executives expect to see interactive technology increase its presence in toy stores. "These new, interactive toys will challenge retailers to take innovative merchandising approaches that help explain what these advanced toys are capable of doing."

New technology also helped toy retailers keep track of their inventories and increased sales. Even smaller toy retailers were moving from manual inventory tracking to computerized systems that hinged on the point-of-sale computer register.

The Internet has also helped bolster the retail toy industry. While sites offering books, movies, and music grew by 17 percent in 1998, toy sites grew by 86 percent. This trend served as a signpost for a bright immediate future for the industry. Amazon.com, Inc, an online shopping company that generated sales of $1.6 billion in 1998, entered the toy-retailing market in the late 1990s and was expected to have a large impact on the industry. According to the U.S. Census Bureau, consumers spent $2.9 billion online for toys in 2000. That increased to $3.2 billion in 2001, and to $3.7 billion for 2002. Overall, there were a total of 22.3 million consumers who purchased toys online in 2002.

Toy Retailers. Manufacturers' shipments of toys, not including video games, increased from $11.4 billion in 1992 to $14.4 billion in 1996, and reached $29.9 billion in 1999. Retail sales rose from $17 billion to $24 billion in the same period. The retail industry as a whole is looking healthier following a difficult recession in the late 1980s and early 1990s. This recovery, coupled with the continued popularity of discount chains such as Wal-Mart, Kmart, and Target, had strong effects on the toy store industry. Some of the toys sold at small independent stores were available at a lower cost on the discounters' shelves because of the inventory advantages such large chains enjoy. Meanwhile, catalog houses, which have made inroads in a number of areas of retailing, have yet to establish themselves as a significant force in the toy retail sector. Toy and hobby catalog purchases still account for only a small share of the total toy market.

Retailers also examined the effect of the increasing numbers of mothers in the workforce, as well as the increasing buying power of the children themselves. Children not only influence their parents in the choice of school items and toys, but, outfitted with greater amounts of disposable income than ever before, also comprise a significant target market by themselves.

Another measurable asset to the toy industry was the sale of video games. David Miller, president of TMA, noted that the success of video games showed that a steep price was not a barrier to the profitable sale of any particular toy. Much of the burden of selling these toys fell on the retailers, whose marketing efforts showed parents and other buyers that the play value of these items was high enough to justify the price. These video games did not fit neatly into retail stores and their existing toy categories. A combination of home entertainment and toy, the video game needed its own space on the retail floor; those retailers who realized this found tremendous profits in video games.

Hobby and Craft Retailers. Retail sales of hobby and craft items increased in the early 1990s as well. In the crafts sector in 1996, general crafts made up 31 percent of purchases ($2.95 billion), while florals and naturals made up 16 percent ($1.53 billion). Frames accounted for 9 percent ($.91 billion), needlecrafts made up 6 percent ($.59 billion), and art materials accounted for 10 percent ($.96). The remainder of sales was in the area of sewing and notions ($2.73 billion). Michaels Stores were the leaders and generated $3,091 million in sales for 2004.

Statistics in the early 1990s showed that consumers preferred to buy their model kits from hobby and toy stores rather than discount stores because of the service they received from the former. Moreover, hobby retailers cite low prices as another factor in their ability to withstand the competition from discounters and catalog sales.

Jockeying With Toy Manufacturers. The Kmart Corporation made an unusual request of toy manufacturers in the summer of 1993—to sell toys on consignment. This meant that the toys would be considered inventory of the manufacturer until their arrival at Kmart stores. Kmart did not want to pay for toys until they went to stores even if they sat in distribution centers for long periods of time. The practical result of this request would be that a poorly selling toy would be the responsibility of the manufacturer. Some large toy manufacturers have refused to comply with Kmart's request, mindful that other retailers were watching Kmart's bid with interest. Other manufacturers, though, have less leverage and are heavily dependent on Kmart to get their products into the marketplace.

This bid came as Kmart, Toys "R" Us, and Wal-Mart, the three largest toy retailers in the United States, sought to convince manufacturers to assume a greater risk in the toy business. The retailers urged a system wherein toys would be replaced immediately by the manufacturers as stocks were depleted. Manufacturers, concerned about the potential for excess inventory such a system would create, have balked at this as well.

In 1998, the Toy Manufacturers of America (TMA)—a trade organization founded in 1916—noted that, due to holiday shopping, approximately two-thirds of toy industry sales occurred in the fourth quarter. Christmas 1999 found shoppers pursuing such products as "Pokemon" and "Star Wars" action figures.

In response to the increasing dominance of large toy chains, specialty toy store owners formed the American Specialty Toy Retailers Association (ASTRA) in 1992. ASTRA created a forum for store owners to exchange ideas, and attempted to create a unified voice that would enable the industry to promote the sale of educational and high-quality toys. Specialty stores were estimated to have about five percent of a $14 billion market in the 1990s.

Industry Leaders

Industry leaders in 2001 included Wal-Mart, which had a 28.4 percent share of the market; Toys "R" Us, which had a 22.79 percent share of the market; KB Toys 6.76 percent; K Mart, 6.75 percent; Target 6.74 percent; Game Shop 3.79 percent; Electronic Boutique 2.93 percent; Best Buy 2.53 percent; Circuit City 1.18 percent; Mattel 1.14 percent; FAO 1.12 percent; Meijer 1.11 percent; and other toy wholesalers represented 15.10 percent. Other significant toy retailers included Ames and J.C. Penney with just over one percent market share each.

Wal-Mart Stores, Inc., the leading retailer in the world, operates approximately 3,600 Wal-Marts and Sam's Clubs throughout North America, South America, Asia, and Europe. Primarily through wide-scale expansion, the company was able to increase its share of the toy market to become the leading retailer in the industry in 2003.

Toys "R" Us, the world's largest toy retailer, had sales of $28 million in fiscal year 2003. It operated discount toy stores in the United States, the United Kingdom, Canada, France, Japan, Spain, and other countries. Kay-Bee Toy Stores, the second-largest toy retailer in America—Kmart, Wal-Mart, and Target are general merchandise discount retailers—operates more than 1,300 toy stores. A division of Consolidated Stores, the company placed most of its stores in shopping malls. Besides these chains, there are an estimated 3,000 specialty toy stores in the United States. Toys "R" Us CEO, John Eyler was fighting back against the price discounters Wal—Mart, and Target Corp. The company was in the progress of reorganizing and preparing for the 2004 holiday season. In an interview, Eyler revealed,"We have developed pricing strategies, lowered out expense structure, and done a number of things that allow us to reinvest in lower prices." Among other toy retailers that felt the strain from the mass merchandisers were Kay-Bee Toys, FAQ Schwarz, Inc., Zany Brainy, and the Right Start who all filed for Chapter 11 bankruptcy protection following by the 2003 holiday season.

Workforce

An estimated 137,147 people were employed in the U.S. toy industry in 2001. Almost 49 percent of the workforce in this industry were salespersons. The rest of the workforce was split among various other jobs such as cashier, stock clerks, executives, and shipping and receiving clerks. Every field within this industry was expected to grow going into the next century, some by as much as 40 percent, and some by only seven percent. In 2003, the workforce climbed to 159,930 and average number of employees per store numbered five.

America and the World

The United States has the largest market for toys in the world. Other successful toy markets include Japan, Germany, France, and the United Kingdom, and global toy sales amounted to $67.8 billion in 1998. Domestic toy manufacturers in 1998 were riding a crest of increased exports that began in the mid-1980s, with exports totaling $1.0 billion. Imports have risen just as steadily, bringing that total to $14.3 billion. Many American toy stores have tried to capitalize on the changing face of the world. Toys "R" Us was one of the first U.S. retail stores to open in Japan. In the early 1990s the company projected that sales there could reach $1.5 billion by the year 2000. It planned to open ten stores each year beginning in 1993. When Toys "R" Us began to expand into Australia, it met with heavy competition from Australia's own retailer, Coles Myer. In the mid-1990s, Coles Myer planned to open large stores called World 4 Kids (W4K) that would go head to head with Toys "R" Us in each market.

A growing concern for consumers is the conditions under which toys, and other personal products, were produced. William J. Holstein, in a U.S. News and World Report article entitled "Santa's Sweatshop," points out that many of the most popular toys are made in sweatshops around the world by overworked, and in many cases, underpaid workers, toiling in unhealthy conditions. The toys mentioned ranged from F.A.O. Schwarz's Bernie St. Bernard to Mattel's Barbie, to a range of Disney products. Holstein also points out that a "Made in America" label is no longer a guarantee of non-sweatshop production, particularly in the garment industry.

Further Reading

D&B Sales & Marketing Solutions, May 2004. Available from http://www.zapdata.com

Grant, Lorrie."KB Toys Files for Chapter 11 after Cutthroat Holiday Season." USA Today, 15 January 2004. Available from http://www.keepmedia.com/pubs/USATODAY/2004/01/15/372064 .

Hoover's Company Capsule, 20 March 2000. Available from http://www.hoovers.com .

Lazich, Robert S., " Market Share Reporter. Farmington Hills, MI: Gale Group, 2004.

Michaels Stores, May 2004. Available http://www.michaels.com .

Toy Industry Association. "2002 vs 2001 State of the Industry," 2002. Available from http://www.toy-tia.org .

Toy Manufacturers of America, 10 February 2000. Available from http://www.toy-tma.com .

Toy Manufacturers Association."2000 Toy Industry Fact Book: The Year in Review," 20 April 2000. Available from http://www.toy-tma.com .

——. "Industry Statistics," 20 April 2000. Available from http://www.toy-tma.com .

"Toys R Us Ready for a Price Fight." Reuters, 19 May 2004. Available from http://www.money.cnn/2004/15/19/news/fortune500/toysrus.reut .

U.S. Census Bureau. Statistical Abstract of the United States, 2002. Available from http://www.census.gov/prod/www.statistical—abstract—03.html .

——. Statistics of U.S. Businesses 2001. Available from http://www.census.gov/epcd/susb/2001/US421420.HTM .

Comment about this article, ask questions, or add new information about this topic: