BALANCE SHEET

In accounting, a balance sheet is a type of financial statement that provides a synopsis of a business entity's financial position at a specific time, including a company's economic resources (assets), economic obligations (liabilities), and the value of a company after its liabilities are subtracted from its assets (owners' equity). The term "balance sheet" refers to the way assets always equal (or balance) liabilities plus owners' equity. Also known as a statement of financial position or a statement of financial condition, the balance sheet usually presents financial information in one of the following formats:

- Assets = Liabilities + Owners' equity

- Assets - Liabilities = Owners' equity

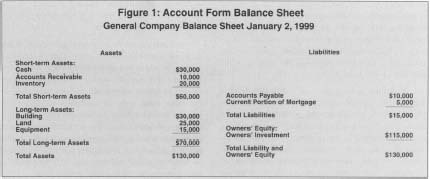

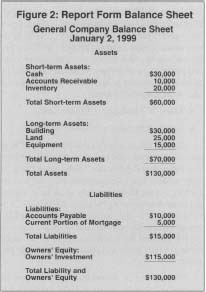

Balance sheets come in two forms: report form and account form, which contain the same information but present it differently. In the report form, the balance sheet lists asset accounts first, and lists the liability and stockholders' equity accounts in sequential order directly below the assets (see Figure 2). In the account form, the balance sheet is organized in a horizontal manner, with the asset accounts listed on the left side and the liabilities and owners' or stockholders' equity accounts listed on the right side (see Figure 1).

The heading of the balance sheet contains the name of the business, the name of the statement (i.e.,

General Company Balance Sheet January 2,1999

CONTENT OF THE STATEMENT

The balance sheet discloses major classes and amounts of a company's assets as well as major classes and amounts of its financial structure, including liabilities and equity. Major classifications used in the statement include:

-

Assets—anything owned by a company that has monetary value,

including economic resources that have current and probable future

value:

Figure 2: Report Form Balance Sheet

Figure 2: Report Form Balance Sheet

General Company Balance Sheet January 2,1999- Current assets (cash, marketable securities, accounts receivable or debt owed to a company, inventory, and prepaid expenses)

- Investments

- Fixed assets (property, plant, and equipment)

- Intangible assets (patents, copyrights, goodwill)

- Deferred charges or other assets

-

Liabilities—current and probable future debts owed by a company

against its assets, including the obligations of a business to transfer

assets or provide services to other parties in the future as a result of

past transactions or events:

- Current liabilities (accounts payable, notes payable, wages payable, and taxes payable)

- Long-term liabilities (bonds payable, pensions, and lease obligations)

- Other liabilities

-

Owners' equity—the resources invested in a company by the

owner. Owners' equity is equal to the assets after deducting the

liabilities:

- Capital stock

- Other paid-in capital in excess of par or stated value

- Retained earnings (dividends)

The essential characteristics of an asset include: (1) it is owned, not leased, by a company, and (2) it has present or future value and a capacity to contribute directly or indirectly to future net cash inflows, either by itself or in combination with other assets.

The essential characteristics of a liability include: (1) it embodies a present duty or responsibility to one or more parties to repay a debt, and (2) the duty or responsibility obligates a particular company, leaving it little or no discretion to avoid paying the debt. Since companies find it convenient and often necessary to purchase materials and supplies on credit, all companies have liabilities. When companies purchase goods on credit, they incur the liability known as an account payable. On the other hand, when companies borrow money, they incur the liability known as a note payable.

Current assets are cash and other assets that are expected to be converted into cash, sold, or consumed either in the year or in the operating cycle of the business, whichever is longer. Current liabilities are the obligations that are reasonably expected to be liquidated either through the use of current assets or the creation of other current liabilities.

Assets are classified in the balance sheet from most liquid to least liquid. Liabilities are classified in the order of maturity. Owners' equity items are classified according to source and in their decreasing order of permanence.

Balance sheets are usually presented in comparative form. Comparative financial statements include the current year's statement and statements of one or more of the preceding accounting periods. For example, companies often provide five- or ten-year balance sheets, which make them useful for evaluating and analyzing trends and relationships.

Notes added to the balance sheet provide additional information not included in the accounts on the financial statements as well as explanations of figures presented in the balance sheet. Moreover, additional information can be disclosed by means of supporting schedules or parenthetical notation.

RECOGNITION AND MEASUREMENT

For an item to be recognized in a balance sheet, the item and information about it must: (1) meet the definition of an element of accounting (the broad classes of items comprising the balance sheet), (2) be measurable (valuation), (3) be relevant, and (4) be reliable.

Assets and liabilities are measured or reported on the balance sheet by different attributes (for example, historical cost, current replacement cost, current market value, net realizable value, and present value of future cash flows), depending upon the nature of the item and the relevance and reliability of the attribute measured. The valuation method primarily used in balance sheets currently is historical cost because it is measurable and provides information that has a relatively high degree of reliability. Historical cost is the price paid for an asset when it was acquired. While this method does not factor in inflation, it provides a convenient, objective way of determining an asset's value because any accountant can verify the cost paid for an asset and because companies generally acquire fixed assets such as property and buildings for business use, not for selling.

Other valuation methods include the current cost, current market value, net realizable value, and present value approaches. Current cost is the amount of cash or cash equivalent required to obtain the same asset at the balance sheet date. Current market value or exit value is the amount of cash that may be obtained at the balance sheet date by selling the asset in an orderly liquidation. Net realizable value is the amount of cash that can be obtained as a result of future sale of an asset. Present value is the expected exit value discounted to the balance sheet date.

CONSOLIDATED BALANCE SHEET

Consolidated financial statements represent the combined financial position of both parent and subsidiary companies. A consolidated balance sheet is presumed to present more meaningful information than separate financial statements of the affiliated companies and must be used in substantially all cases in which a parent company directly or indirectly controls the majority voting stock (over 50 percent) of a subsidiary. Consolidated financial statements should not be prepared in those cases in which the parent's control of the subsidiary is temporary or where there is significant doubt concerning the parent's ability to control the subsidiary. Furthermore, the consolidated balance sheet does not include revenues and expenses resulting from intercompany transactions, i.e., transactions between parent and subsidiary companies.

USES AND LIMITATIONS

The balance sheet assists external users of financial statements in assessing a company's liquidity, financial flexibility, and operating capabilities, as well as in evaluating the earnings performance for the period. Liquidity describes the amount of time that is expected to elapse until an asset is realized or otherwise converted into cash or until a liability has to be paid. Financial flexibility is the ability of an enterprise to take effective action to alter the amounts and timing of cash flows so it can respond to unexpected needs and opportunities. Operating and performance capabilities refer to the capability and effectiveness of a company related to its major or ongoing revenue producing activities.

Many bankers and miscellaneous users of balance sheets consider having total current assets that are roughly twice as much as its total current liabilities a sign of a company's creditworthiness. Consequently, they use balance sheets to determine the ratio of a company's total current assets to its total current liabilities, or the current ratio. Creditors compute the current ratio by dividing the total current assets by the total current liabilities, yielding a measurement of a company's ability to repay debt. The amount of current assets over current liabilities is a company's working capital. Banks also rely on balance sheets to determine a company's liquidity—the amount of cash and assets easily convertible to cash, such as a company's accounts receivable.

The balance sheet has major limitations, however. The balance sheet does not necessarily reflect the fair market value of assets because accountants typically apply the historical cost principle in valuing and reporting assets and liabilities. The balance sheet omits many items that have financial significance. Furthermore, professional judgment and estimates are often used in the preparation of balance sheets, possibly impairing the usefulness of the statements. Finally, since balance sheets contain only financial information, they do not list such important information as the intensity of a company's competition and the experience and skill of a company's management personnel, which affect a company's financial performance.

SEE ALSO : Auditing ; Income and Revenue ; Income Statement ; Liabilities

[ Charles Woelfel ,

updated by Karl Hell ]

FURTHER READING:

Eskew, Robert K., and Daniel L. Jensen. Financial Accounting. 5th ed. New York: McGraw-Hill, 1999.

Financial Accounting Standards Board. Statements of Financial Accounting Concepts. Homewood, IL: Irwin, 1987.

Meigs, Robert F., et al. Accounting: The Basis for Business Decisions. 11th ed. Boston: Irwin/McGraw-Hill, 1999.

Why dr. A/c is in left side and cr. A/c in right side?